So, I virtually never read articles anymore with sensational titles (actually, I seldom read any 'articles' anymore). However, I can't help but read a headline when it somehow sneaks onto my screen.

This title caught my attention this morning:

Friday, March 31, 2017

Wednesday, March 29, 2017

This Week's Video: The Weight of the Evidence

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Tuesday, March 28, 2017

Quote(s) of the day: Wisdom of a great speculator....

As I preach here incessantly, to be successful at investing one must develop a sense for the macro, and diligently dull the senses that might otherwise be piqued by the sensationalizing media.

Dixon G. Watts, the 19th Century speculator (one of history's best and most respected), was a man of great wisdom:

Dixon G. Watts, the 19th Century speculator (one of history's best and most respected), was a man of great wisdom:

It is better to act on general than special information (it is not so misleading), viz., the state of the country, the condition of the crops, manufacturers, etc. Statistics are valuable, but they must be kept subordinate to a comprehensive view of the whole situation.

A man must think for himself, must follow his own convictions. George MacDonald says: “A man cannot have another man’s ideas any more than he can another man’s soul or another man’s body.” Self-trust is the foundation of successful effort.

That equipoise, that nice adjustment of the faculties one to the other, which is called good judgment, is an essential to the speculator.

Monday, March 27, 2017

Move along...

Dow's down 165 as I type. All the headlines blame Congress's failure to replace the Affordable Care Act. The market dipping for that particular reason is curious, given this S&P 500 chart that begins the day the ACA was enacted: click any chart to enlarge...

Friday, March 24, 2017

This Week's Message: Good traders and good investors have more in common than you think...

In Tuesday's video we took a look at that day's pummeling of the sectors we favor: click any chart to enlarge

Ugh! All things cyclical took a bath, while the defensive stocks (the stocks you buy when nobody's buying cars and computers) fared just fine.

So, clearly, the market was signaling that all's not as it may appear. Right? Well, yeah, you'd have to conclude that if the stocks of companies that benefit from a growing economy, higher interest rates, a little inflation, etc., are getting creamed, we maybe have issues. Now, of course one day's action does not a trend make. However, when we're talking a 3% hit to the sector, financials, that stands to perhaps benefit the most from higher rates, etc., we simply can't ignore it. Or can we?

Ugh! All things cyclical took a bath, while the defensive stocks (the stocks you buy when nobody's buying cars and computers) fared just fine.

So, clearly, the market was signaling that all's not as it may appear. Right? Well, yeah, you'd have to conclude that if the stocks of companies that benefit from a growing economy, higher interest rates, a little inflation, etc., are getting creamed, we maybe have issues. Now, of course one day's action does not a trend make. However, when we're talking a 3% hit to the sector, financials, that stands to perhaps benefit the most from higher rates, etc., we simply can't ignore it. Or can we?

Tuesday, March 21, 2017

This Week's Video Commentary: How meaningful -- for you and me -- was today's selloff?

Once playing, click the icon in the lower right corner for full screen. Focus occurs after a few seconds:

Quote(s) of the Day: A thing in motion...

As is forever the case, the financial media isn't wanting these days for characters who would have us believe that they can foretell the stock market's future. Which, of course -- as markets are people -- requires that they possess some magical insight into the coming collective decisions of the world's consumers, investors, traders, politicians, etc.. Ironically, the proof that they unequivocally lack such skill is the simple fact that they claim to have such skill. That is, such skill, kept to oneself, would make one far and away the richest self who's ever lived. And, yes, while ego by itself is no doubt at play, make no mistake, these would-be seers desire to be rich.

Saturday, March 18, 2017

History likes what we've seen so far...

The following from Bespoke Investment Group speaks to the setup we've been discussing here on the blog:

Knowing yourself can be tough...

Of all of the painstaking research and analysis we do here at PWA, there's an area of interest that holds huge sway over our approach to individual client portfolio management. An "area" that we believe has major implications in terms of the prospects for favorable long-term results on a client-specific basis. Call it risk tolerance, or perhaps behavioral finance, if you like; I think of it in terms of client predilections, preconceptions and degrees of impressionability.

Friday, March 17, 2017

Quote of the Day -- AND -- The Budget Cut/Border Tax Contradiction...

Here's Don Boudreaux responding to a reader who can't see through the understandably-presumed negative effects of a government budget cut on certain groups to the positive effects on others:

If you believe that society is harmed when government taxes one group to subsidize another, how in the world can you believe that society benefits when government forces higher goods prices (via a border tax) on all groups to subsidize a few ginormous politically-powerful corporations?

When budgets are cut, it’s easy to see the likes of government employees who lose jobs, farmers who get smaller subsidy checks, arts exhibitions that must now survive exclusively on private contributions, and poor people whose welfare payments fall. But the analysis and conversation nearly always stop there. If cutting funding for some government-funded activity is found to cause some hardship (and which such activity isn’t so found?), cutting government funding of that activity is typically deemed cruel and wrong. But what is too-seldom asked is: As compared to what? What will those who now keep more of their incomes spend this money on? In what ways will the money now left in the private sector be invested? What new products, businesses, and economic opportunities might be created now that the state no longer seizes these resources from those who create or earn them? And how will system-wide incentives change when government reduces taxes and spending?I know for certain that no small number of my readers sympathize, passionately, with Don. I also strongly suspect that no small number of that no small number will fail to apply the very same logic to a proposal that would levy an across-the-board tax on foreign imports.

If you believe that society is harmed when government taxes one group to subsidize another, how in the world can you believe that society benefits when government forces higher goods prices (via a border tax) on all groups to subsidize a few ginormous politically-powerful corporations?

This Week's Message: The Fed Funds Rate Reaction

On Wednesday, on cue, the Fed raised its benchmark interest rate a quarter-point. However, the members effectively signaled in their commentary -- and Yellen in her press conference -- that while things are improving, they're doing so at a pace that does not warrant what would be deemed aggressive monetary tightening.

Perfect! That allows bonds to rally, gold to rally, developed foreign markets to rally, emerging markets to rally, staples to rally, cyclicals to rally, utilities to rally and REITs to rally. Man Oh Man!

Perfect! That allows bonds to rally, gold to rally, developed foreign markets to rally, emerging markets to rally, staples to rally, cyclicals to rally, utilities to rally and REITs to rally. Man Oh Man!

Wednesday, March 15, 2017

This Week's Video Commentary

Once playing, click the icon in the lower right corner for full screen. Focus occurs after a few seconds:

Tuesday, March 14, 2017

The Market Does What It Wants...

As I type, it's virtually 100% certain that the Fed is going to bump up its benchmark interest rate tomorrow. This morning the NFIB Small Business Optimism Index for February was released. Here's from Bloomberg:

So then, with upbeat economic prospects and naturally higher interest rates, you should bet the farm today that the interest rate-sensitive sectors are selling off and the cyclicals are soaring. Right? Well, nope...

At this moment, bonds are up half a percent (in price, meaning yields are lower), utilities are break even and gold's up 2 bucks.

As for the stuff that's supposed to rise with a good economy and higher interest rates, financials, industrials, energy, materials and technology are down .80%, .93%, 1.44% and .50% respectively. Go figure!

Jesse Livermore, whose story is arguably one of Wall Street-history's most fascinating, and instructive -- he literally made millions in the early 1900s when he followed his own rules, and blew up time and time again when he didn't -- spoke to the wisdom that ultimately told of his own undoing:

My best guess is -- given the present setup -- that a little (or a lot) selling into the news may prove healthy in the weeks/months following it.

...the index remaining above 105 for three consecutive months indicates the continuation of a very high level of optimism for small business owners.Also this morning we saw the release of the February Producer Price Index. Bloomberg again:

Year-on-year, overall producer prices are up 2.2 percent for the hottest rate in nearly 5 years.Today's releases jibe perfectly with the balance of indicators that suggest the economic outlook is bright, and with the to-be-expected attendant (albeit moderate ["the hottest" in a remarkably low-inflation five years]) inflation pressure, the Fed has a very green light to push the needle on interest rates.

So then, with upbeat economic prospects and naturally higher interest rates, you should bet the farm today that the interest rate-sensitive sectors are selling off and the cyclicals are soaring. Right? Well, nope...

At this moment, bonds are up half a percent (in price, meaning yields are lower), utilities are break even and gold's up 2 bucks.

As for the stuff that's supposed to rise with a good economy and higher interest rates, financials, industrials, energy, materials and technology are down .80%, .93%, 1.44% and .50% respectively. Go figure!

Jesse Livermore, whose story is arguably one of Wall Street-history's most fascinating, and instructive -- he literally made millions in the early 1900s when he followed his own rules, and blew up time and time again when he didn't -- spoke to the wisdom that ultimately told of his own undoing:

The reason is that a man may see straight and clearly and yet become impatient or doubtful when the market takes its time about doing as he figured it must do. That is why so many men in Wall Street, who are not at all in the sucker class, not even in the third grade, nevertheless lose money. The market does not beat them. They beat themselves, because though they have brains they cannot sit tight.While we can't know that this go-round the stuff that makes sense -- given the perceived conditions we find ourselves in -- will ultimately be the stuff of reality, one thing's for sure, in the near-term the market will do whatever it wants, for whatever its reasons.

My best guess is -- given the present setup -- that a little (or a lot) selling into the news may prove healthy in the weeks/months following it.

Sunday, March 12, 2017

Quotes of the Day: Border Tax Winners and Losers

Like virtually any other government proposal, Congress's "Border Adjustment Tax", in terms of its ultimate impact on U.S. individuals and institutions, is, at best, difficult for discerning folks to frame. I have to qualify with "discerning" because of course there are those who immediately presume that taxing foreign imports is good because "they do it us", "it'll inspire us to buy American", "it'll create jobs" and so on. Of course if all that were true, it would be reality, as opposed to what it's mostly been for eons -- campaign-stump rhetoric. In reality, there's much more negative potential and, therefore, political risk than meets the eye.

Without delving into currency fluctuations, retaliation from foreign trading partners, crony capitalism, etc., one way to handicap who the winners and losers of the taxing of imports by 20% would be is to simply look at the players who are for and against it.

Keep in mind, the U.S. -- with two-thirds of its GDP owing to consumer spending -- is a resoundingly consumer-driven economy.

Here's what Americans for Affordable Products (a coalition of 120 retailers [make their money via the consumer], which includes the likes of Best Buy, Dollar General, Macy's, Rite Aid and Walmart) think of the proposal:

Without delving into currency fluctuations, retaliation from foreign trading partners, crony capitalism, etc., one way to handicap who the winners and losers of the taxing of imports by 20% would be is to simply look at the players who are for and against it.

Keep in mind, the U.S. -- with two-thirds of its GDP owing to consumer spending -- is a resoundingly consumer-driven economy.

Here's what Americans for Affordable Products (a coalition of 120 retailers [make their money via the consumer], which includes the likes of Best Buy, Dollar General, Macy's, Rite Aid and Walmart) think of the proposal:

We oppose any border adjustment tax (BAT) because it will increase the cost of clothing, food, medicine, gas, and other essential items that Americans rely on," the group says on its website. "Consumers shouldn’t bear the burden of this new tax while some corporations get a tax break.And here's from a Knowledge at Wharton interview with Wharton's own Ann Harrison and Penn Law's Michael Knoll:

... big exporters, including technology companies and large industrial companies like General Electric could have nil or even negative tax liability, he said. Indeed the chief executives from 16 companies, including GE, Oracle and Pfizer, sent a letter to congressional leaders this week in support of the GOP tax plan.

Careful what you ask for...

P.s., I feel the need to qualify the "winners" column: The advocating by the GEs, etc., is, in my view, simply the result of CEO myopia (fixation on near-term quarterly earnings results). The ultimate ramifications of hammering the U.S. consumer to maybe balance Washington's this or that has to ultimately bode poorly for the would-be-winner as well.

P.s., I feel the need to qualify the "winners" column: The advocating by the GEs, etc., is, in my view, simply the result of CEO myopia (fixation on near-term quarterly earnings results). The ultimate ramifications of hammering the U.S. consumer to maybe balance Washington's this or that has to ultimately bode poorly for the would-be-winner as well.

Saturday, March 11, 2017

Quote of the day: How not to book a 50% gain...

A relatively new client -- one with whom we've yet to experience a true down market -- asked me yesterday how we'd handle things when the market experiences its next big selloff. I love such questions, for two reasons. One: they affirm for me that my client understands the nature of things; i.e., that stocks will forever experience draw downs and bear markets. And two: they give me the opportunity to outline the ills of market timing for long-term investors.

I explained that we'd maintain our equity/fixed income mix which we previously determined -- and confirmed yesterday -- was, for him, an emotionally-palatable position. We then discussed how we meld fundamental and technical analyses to determine what we believe to be the most prudent sector and regional equity mix. As the cycle evolves and the data offer their signals (dictating whether our tilt/bias is toward cyclical vs defensive sectors), our sector allocation evolves as well.

Again, the notion that the long-term investor can or should attempt to play the price swings is a dangerous notion indeed -- as I illustrated with this chart in last week's video: click to enlarge...

And as Chris Ciovacco stated in his weekly presentation:

I explained that we'd maintain our equity/fixed income mix which we previously determined -- and confirmed yesterday -- was, for him, an emotionally-palatable position. We then discussed how we meld fundamental and technical analyses to determine what we believe to be the most prudent sector and regional equity mix. As the cycle evolves and the data offer their signals (dictating whether our tilt/bias is toward cyclical vs defensive sectors), our sector allocation evolves as well.

Again, the notion that the long-term investor can or should attempt to play the price swings is a dangerous notion indeed -- as I illustrated with this chart in last week's video: click to enlarge...

And as Chris Ciovacco stated in his weekly presentation:

It is not possible to ever book a 50% to 80% gain if we over-trade and overmanage during a strong bullish trend...

Friday, March 10, 2017

The Week's Message: Only heed those with skin in the game...

Reagan budget director David Stockman has a knack for getting himself in the headlines. Seriously, take a look at his latest work (this is just me Googling for a few minutes):

Wednesday, March 8, 2017

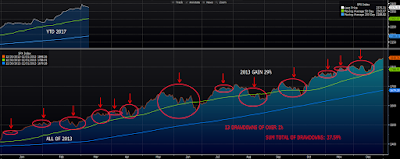

Market Commentary: So far, a lot like 2013 (video)

This week's video is short and simple. Ironically, I've always found the basic stuff to be the stuff most critical to long-term investment success. Be sure to watch this one.

After clicking the play button click the icon in the lower right corner for full screen. Focus will occur a few seconds later.

After clicking the play button click the icon in the lower right corner for full screen. Focus will occur a few seconds later.

Quote of the Day: Death Wishes -- or -- Deficit Spending

As I've expressed herein a thousand times and in a multitude of ways, markets are people. Famed trader, Richard Dennis, who, in his heyday was far more interested in David Hume than he was the details of any employment report, while expressing where his interests lied, spoke to the force that inspires markets and moves investors/traders to all manner of self-destructing behavior:

I think it's far more important to know what Freud thinks about death wishes than what Milton Friedman thinks about deficit spending.

Monday, March 6, 2017

There's Certainly Uncertainty Around the Impact of Higher Interest Rates

The Federal Open Market Committee meets next week, and futures pricing says a rate hike is a virtual certainty: click charts to enlarge...

What's is clearly uncertain on Wall Street is the impact higher rates will have on the economy. The chart below shows us that futures speculators are heavily short treasury bonds (betting rates are going up and bond prices are, thus, going down) -- and that asset managers who trade futures are, on the other hand, heavily long (suggesting rate hikes will be considered virtually out of the blocks as constraining, and leading to lower yields and, thus, higher bond prices):

While markets can forever surprise us, my best guess is that the speculators are ultimately on the right side of this particular trade. The economic data generally supports their position, and, while showing a slightly stabler picture of late, on balance, the technicals are in their favor as well:

What's is clearly uncertain on Wall Street is the impact higher rates will have on the economy. The chart below shows us that futures speculators are heavily short treasury bonds (betting rates are going up and bond prices are, thus, going down) -- and that asset managers who trade futures are, on the other hand, heavily long (suggesting rate hikes will be considered virtually out of the blocks as constraining, and leading to lower yields and, thus, higher bond prices):

While markets can forever surprise us, my best guess is that the speculators are ultimately on the right side of this particular trade. The economic data generally supports their position, and, while showing a slightly stabler picture of late, on balance, the technicals are in their favor as well:

Sunday, March 5, 2017

Beware the Junior-High-Genius! -- And -- Pain is Essential

"If Washington rolls back financial regulations, could we see a replay of 2008?" That (words to that effect) was a question posed to me during a meeting last week. My immediate response was

"no. Not, that is, with the current players in the banking system. Not that shenanigans of the sort -- regardless of the prevailing regulatory regime -- aren't indeed likely to repeat, it's just that I suspect the likes of 2008 (a financial sector meltdown spawned by careless securitization of mortgages, and layers of speculation on those securities) will have to come at the hands of future geniuses who now attend junior high school, and who are, thus, oblivious to the happenings of 9 years ago" (words to that effect). I then proceeded to ramble on about the history of bailouts and my belief that had the powers-that-be not rescued the politically-powered bankers/investors of old from their folly, Wall Street's (I generalize) confidence that it could privatize its gains (it keeps em) and socialize its losses (taxpayers forced to come to its rescue) would never have been ingrained in its psyche.

"no. Not, that is, with the current players in the banking system. Not that shenanigans of the sort -- regardless of the prevailing regulatory regime -- aren't indeed likely to repeat, it's just that I suspect the likes of 2008 (a financial sector meltdown spawned by careless securitization of mortgages, and layers of speculation on those securities) will have to come at the hands of future geniuses who now attend junior high school, and who are, thus, oblivious to the happenings of 9 years ago" (words to that effect). I then proceeded to ramble on about the history of bailouts and my belief that had the powers-that-be not rescued the politically-powered bankers/investors of old from their folly, Wall Street's (I generalize) confidence that it could privatize its gains (it keeps em) and socialize its losses (taxpayers forced to come to its rescue) would never have been ingrained in its psyche.

Saturday, March 4, 2017

This Week's Message: I'm not feeling late- '90s euphoria right about now -- And -- The Prudence in Political Agnosticism...

It's interesting, I keep hearing "experts" suggest that investors are way too giddy about the stock market these days. But, honestly, that's not my observation. While, sure, folks have to be feeling good about the present state of affairs, I'm certainly not sensing giddiness in our clients as we conduct our semi-annual reviews. Again, not that they're not liking their results these days, but nobody's threatening to mortgage the farm and throw it all at the stock market. I'm definitely not feeling the late-'90s right about now.

Friday, March 3, 2017

My Friend Dick

There's a school of thought that says if you want to be successful in business, discover what it is that truly sets you apart from the competition; the one thing that you can do better than virtually anyone else. I have this friend who embodied that concept. This gentleman, either through thoughtful self-analysis or instinct (I suspect the latter), discovered at an early stage that he indeed possessed a one thing that made him unique in his business. And this gentleman, my dear friend Dick Wetnight, exploited his one thing to the fullest -- while he outsourced virtually all of the minutia and the mundane to others. I've often referred to him as a master delegator; a mastery that I've come to understand is absolutely essential to success in business.

Wednesday, March 1, 2017

Market Commentary: What does breadth say about the current trend?

Click the icon in the lower right corner for full screen. Wait a few seconds for focus:

Quote of the Day

Big rally today! As I type the Dow's up 330. Per last week's message, some on Wall Street, as well as main street, are wondering when the inevitable fall will come.

Yep, for sure, there'll be a fall. In fact, there'll be many this year -- I'm certain. That said, as I continue to chart for you, there's also the current trend, and, per Jesse Livermore below, that's what smart investors focus on:

Yep, for sure, there'll be a fall. In fact, there'll be many this year -- I'm certain. That said, as I continue to chart for you, there's also the current trend, and, per Jesse Livermore below, that's what smart investors focus on:

The big money is not in the individual fluctuations, but in the big movements. That is, not in reading the tape, but in sizing up the entire market and its trend.

Subscribe to:

Comments (Atom)