In Part Five I explained the relationship -- negative correlation -- between commodities prices and the U.S. dollar.

Thursday, December 31, 2020

Morning Note: Capitalist-minded readers may enjoy this one...

Well, it's the last trading day of 2020 -- quite the year! We'll bid it a fond farewell in the upcoming close to our lengthy year-end letter.

Wednesday, December 30, 2020

PWA 2020 Year-End Letter Part Six: Sectors

In this part six of our year-end letter I'll present an overview of how we see the U.S. equity market setup on a sector by sector basis.

Morning Note: "The Higher The Markets Go The......"

Bloomberg's headline credits vaccine optimism and a weak dollar for this morning's rally in stocks.

In that the former, while great news!, was a given, I'll take the latter as the primary reason equities are up to start the session.

Tuesday, December 29, 2020

PWA 2020 Year-End Letter, Part Five: Commodities and the Dollar

While we've beaten the proverbial dead horse, well, to death, when it comes to the utter canyon that separates stock market fundamentals from stock prices these days, there's one asset class -- which currently directly occupies 22% of our core mix, and, indirectly, via resource-driven stocks, another 9% -- where the fundamentals are intact, and, in fact, present quite the attractive setup.

Quote of the Day: Funny thing about stocks...

From the upcoming Part Five (on commodities) of our year-end letter:

Morning Note: Hmm...

Fear that the senate may not go with $2,000 per person stimulus checks seems to have stocks struggling to find their legs this morning. Given its broad popularity, it'll be interesting to see if senate Republicans can muster, or maintain, the political will to stand in its way.

Monday, December 28, 2020

Quick Afternoon Update

Typically, holiday trading isn't worth reporting on, so take this one with a grain of salt.

But since I went there this morning, and things have notably changed as the session's worn on, I thought I'd give you a quick update.

Morning Note: We have serious 'fundamental' concerns, however...

You'd expect that a trillion dollars of fresh government spending would have the Dow up triple digits. And you'd also expect that such support for markets would have money screaming in, in a real FOMO (fear of missing out) sort of way.

Sunday, December 27, 2020

PWA 2020 Year-End Letter, Part Four: The Good, the Bad, and the Ugly -- And -- Lessons of Nature

For stock prices...

The Good:

Like no other time in history, stock markets have the support of policymakers.

Years of business cycle manipulation, resulting in persistently low interest rates, have established stocks as the perceived only game in town to capture yield and to beat inflation.

Saturday, December 26, 2020

PWA 2020 Year-End Letter, Part Three: Bubbles, Zombification, The Fed and the Future

In 2002, amid the bursting of the 90’s tech bubble, then Fed Chairman Alan Greenspan proclaimed that bubbles are difficult to identify until, alas, after the fact:

In fact, fast forward 16 years, and, ironically, Mr. Greenspan himself agrees that bubbles can indeed be foreseen.

Easily, in fact, based on his conviction in 2018 that bubbles had formed in both the stock and the bond markets:

Although, we didn’t begin adjusting portfolios to that reality until our macro index turned red late-summer 2019. At that point odds favored recession over expansion going forward, and our view was that the next recession would pierce the debt bubble and bring on a worse-than-2008 experience.

Here’s yours truly on Halloween Day 2019 in This Week's Message: Absolutely, There is A Bubble:

I.e., policymakers have zero interest in seeing debt markets back “to something remotely resembling normalcy.” Or, let’s say, in allowing the necessary painful process to unfold...

We are sorely missing Milton Friedman these days! emphasis mine...

We’d in many ways be adopting the Japanese model, which emerged in response to the bursting of Japan’s own 1980s debt-fueled asset bubble.

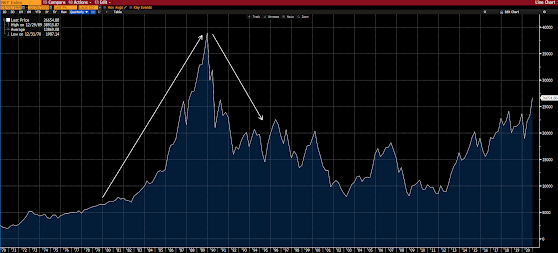

Here’s it is reflected in the Japanese equity market (1970 to current):

To get a feel for how Japan dealt with the fallout, here’s from a February 2003 IMF paper titled Japan’s Lost Decade:

And, yes, that can-kicking indeed managed to keep a 1930’s-style depression at bay.

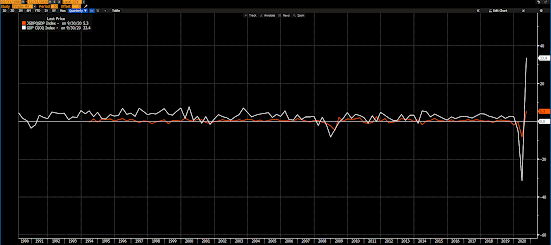

Japan’s unemployment rate (orange) vs the U.S.’s (white) from 1990 to present:

Successfully averting depression notwithstanding, Japan’s policymakers -- having no stomach for the pain that would result from failed enterprises meeting their market fates -- have left their economy constrained by "zombie" companies.

Short and sweet, from a 2017 Bloomberg article on productivity issues in Japan’s manufacturing space:

As for the U.S., not so good, we're 9th. We were #1 in 2013. Hmm....

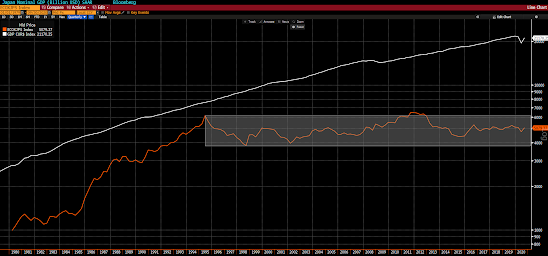

Note how Japan’s GDP growth rate (orange) has essentially hugged the zero line all these years (until recently [although that’s bouncing off of the Covid low]): (U.S. GDP in white)

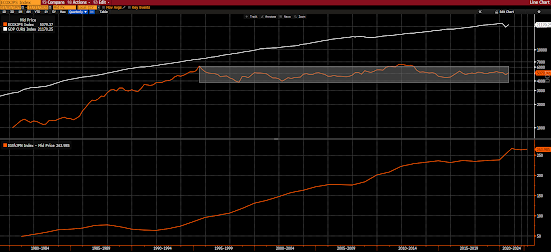

Here’s a look at Japan’s GDP (orange) in nominal terms. Note the utter stagnation these past 25 years. (US nominal GDP in white):

And note the incredible rise in Japan’s government debt (bottom panel) -- now 264% of GDP -- while the economy has done essentially nothing:

I.e., Pain-aversion (and, thus, stagnation) comes with a very high price tag!

Yes, Professor Friedman was spot on:

And, lastly, before we tackle today’s debt bubble, while the above may sound dire, understanding what policymakers will have to bring to bear in their attempts to avert a worse-than-2008 financial market scenario brings clarity (read opportunity) to the portfolio management process…

As a picture can speak a thousand words -- and since we’ve been relentlessly pounding on this topic for well over the past year -- I’ll be succinct with the rest, and enlist the aid of a few charts to once again make our point.

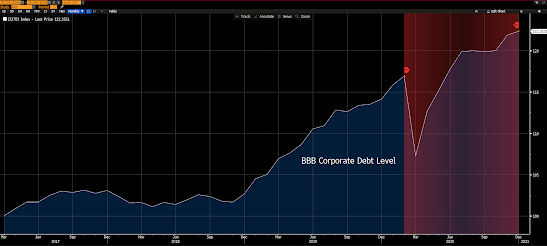

Here’s that BBB-rated (one notch above junk) U.S. corporate debt chart that I featured multiple times late last year, updated:

Remarkable!

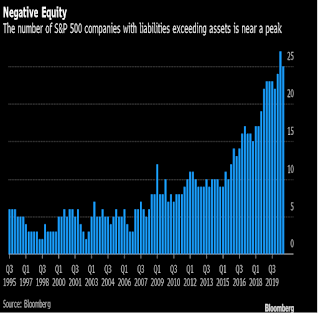

And how about U.S. companies (within the S&P 500) with literally upside down balance sheets:

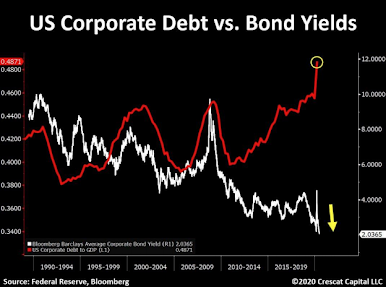

And to really drive home the surrealness of the day, note the head-scratching divergence between the growth in corporate debt and its cost:

Like I said above:

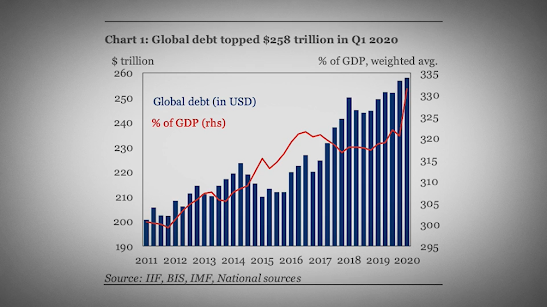

Of course this is not just a U.S. phenomenon.

Bottom line folks, great financial crises tend to come at the end of great private-sector debt cycles. A history that the powers-that-be are all too aware of. Hence their willingness to risk (accept/strive for) long-term stagnation to avoid the short(er)-term painful consequences of, frankly, conditions of their own making.

Whether or not they’ll “succeed” of course remains to be seen. Which is a risk we absolutely must hedge against as we otherwise work to exploit the opportunities inherent in an environment where policymakers will remain hellbent on, among other things, keeping interest rates, as well as the dollar, pinned to the floor…

In parts four and five we’ll explore some of those opportunities, as well as the risks, presented by today’s equity, commodity and currency markets' setups...

''As events evolved, we recognized that, despite our suspicions, it was very difficult to definitively identify a bubble until after the fact -- that is, when its bursting confirmed its existence.''Well, frankly, that’s a notion I wholeheartedly reject.

In fact, fast forward 16 years, and, ironically, Mr. Greenspan himself agrees that bubbles can indeed be foreseen.

Easily, in fact, based on his conviction in 2018 that bubbles had formed in both the stock and the bond markets:

“"There are two bubbles: We have a stock market bubble, and we have a bond market bubble," the former Federal Reserve chairman told Bloomberg TV.Yes, as regular readers know all too well, I agree with Mr. Greenspan (the 2018 version, that is) that bubbles can be foreseen (the timing of their bursting is of course another matter), and that the bond (debt) bubble is presently “the critical issue.”

The trouble in the bond market "will eventually be the critical issue," Greenspan said, adding that "for the short term it's not too bad."”

Although, we didn’t begin adjusting portfolios to that reality until our macro index turned red late-summer 2019. At that point odds favored recession over expansion going forward, and our view was that the next recession would pierce the debt bubble and bring on a worse-than-2008 experience.

Here’s yours truly on Halloween Day 2019 in This Week's Message: Absolutely, There is A Bubble:

“...all of that stimulus coming out of the bursting of the mortgage bubble was so effective at inflating asset prices (just like it was coming out of the dotcom bubble), while wedding them (asset prices) to interest rates, that the Fed has boxed itself into the proverbial corner.Hence, here we are, living a surreality that could only occur at the end of a debt supercycle, amid epic asset price bubbles, and while panicky policymakers who -- in their willful abandonment of capitalism -- are desperate to keep asset markets and failed companies afloat.

And, worse yet -- and this is the fundamental problem -- it created yet another debt bomb that probably can't be diffused; meaning, it more than likely has to detonate, intentionally or otherwise, before we can even begin to get back to something remotely resembling normalcy in the debt markets.

And of course the Fed fears, legitimately!, that that detonation will surely come at the hands of (or be blamed on) voting members who don't pull every possible lever to delay it till the proverbial cows come home. But what will those proverbial cows be able to do??”

I.e., policymakers have zero interest in seeing debt markets back “to something remotely resembling normalcy.” Or, let’s say, in allowing the necessary painful process to unfold...

We are sorely missing Milton Friedman these days! emphasis mine...

"The economic miracle that has been the United States was not produced by socialized enterprises, by government-union-industry cartels or by centralized economic planning. It was produced by private enterprises in a profit-and-loss system. And losses were at least as important in weeding out failures as profits in fostering successes. Let government succor failures, and we shall be headed for stagnation and decline.”As I ponder the possibility that -- now that the Fed has utterly breached the dictate of the Federal Reserve Act and is, via a work around with the treasury, intervening into the securities (other than treasuries and govt-backed mortgages) market -- perhaps this time may indeed be different (i.e., no 50+% hit to the stock market, and no true debt market clearing), it’s clear to me that, in that scenario, “stagnation and decline” become serious risks over the long-term…

We’d in many ways be adopting the Japanese model, which emerged in response to the bursting of Japan’s own 1980s debt-fueled asset bubble.

Here’s it is reflected in the Japanese equity market (1970 to current):

To get a feel for how Japan dealt with the fallout, here’s from a February 2003 IMF paper titled Japan’s Lost Decade:

“On the corporate side, rates of return remain low, not least because of the slow progress in reducing the still significant excesses of capital, debt, and employment from the bubble years. Concerns about the impact of restructuring on unemployment may constrain the speed of adjustment…”In other words, intense pain-aversion inspired Japan’s policymakers to do whatever it took (bailouts, credit creation, huge fiscal deficit, etc.) to essentially keep their debt market from clearing (excesses from being purged). Note that the above-referenced paper was written 13 years after the bubble began to burst!

And, yes, that can-kicking indeed managed to keep a 1930’s-style depression at bay.

Japan’s unemployment rate (orange) vs the U.S.’s (white) from 1990 to present:

Successfully averting depression notwithstanding, Japan’s policymakers -- having no stomach for the pain that would result from failed enterprises meeting their market fates -- have left their economy constrained by "zombie" companies.

Short and sweet, from a 2017 Bloomberg article on productivity issues in Japan’s manufacturing space:

"“Some Japanese companies keep unprofitable businesses alive to maintain employment,” says Yasuhiro Kiuchi, senior researcher at the Japan Productivity Center in Tokyo."

Unprofitable businesses that require constant capital infusions to stay afloat (zombies) are drags on an economy, as they consume resources that could've otherwise been used in productive endeavors.

You'll recall how Japan was once the word's innovation leader, well, Bloomberg's Innovation Index now has them in 12th place.As for the U.S., not so good, we're 9th. We were #1 in 2013. Hmm....

Note how Japan’s GDP growth rate (orange) has essentially hugged the zero line all these years (until recently [although that’s bouncing off of the Covid low]): (U.S. GDP in white)

Here’s a look at Japan’s GDP (orange) in nominal terms. Note the utter stagnation these past 25 years. (US nominal GDP in white):

And note the incredible rise in Japan’s government debt (bottom panel) -- now 264% of GDP -- while the economy has done essentially nothing:

I.e., Pain-aversion (and, thus, stagnation) comes with a very high price tag!

Yes, Professor Friedman was spot on:

“Let government succor failures, and we shall be headed for stagnation...”There’s much more we could dissect with regard to Japan’s post-80s economy -- ~zero interest rates in perpetuity, central bank balance sheet, lousy demographics, waning productivity, etc. -- but suffice to say that virtually all of it, even to some degree lousy demographics (read immigration policies, and the correlation between wage growth/standard of living and population growth), results from government’s unwillingness to allow markets to clean up the messes government creates.

And, lastly, before we tackle today’s debt bubble, while the above may sound dire, understanding what policymakers will have to bring to bear in their attempts to avert a worse-than-2008 financial market scenario brings clarity (read opportunity) to the portfolio management process…

As a picture can speak a thousand words -- and since we’ve been relentlessly pounding on this topic for well over the past year -- I’ll be succinct with the rest, and enlist the aid of a few charts to once again make our point.

Here’s that BBB-rated (one notch above junk) U.S. corporate debt chart that I featured multiple times late last year, updated:

Remarkable!

And how about U.S. companies (within the S&P 500) with literally upside down balance sheets:

And to really drive home the surrealness of the day, note the head-scratching divergence between the growth in corporate debt and its cost:

Like I said above:

“...a surreality that could only occur at the end of a debt supercycle, amid epic asset price bubbles, and while panicky policymakers who -- in the willful abandonment of capitalism -- are desperate to keep asset markets and failed companies afloat.”So, cutting to the chase, here’s from our October 9 blog post:

“...I would not have expected -- because it was illegal at the time (well, technically still is) -- that the Fed would be able to buy corporate bonds, junk-rated ones no less, and, thus, leave people with legitimate reason to believe that there's absolutely no place they ultimately won't go to keep markets from clearing (Federal Reserve Act constraints be damned!) -- which given the debt mess we came into this recession with (before I could even spell coronavirus) would ultimately be destined to exacerbate the worst recession since the Great Depression.

Well, we indeed have the latter, but, thus far, we haven't remotely experienced the clearing necessary to allow markets to emerge in any semblance of decent shape.

So why might I have previously proclaimed that the next recession would be the worst since the Great Depression? Well, among other things, charts like the following two:

My black arrows point to how after the past several recessions (grey shaded areas) total corporate debt cleared only to a point that left more on the books than the bottom of the one prior. My red arrows point to how interest rates peaked at a lower spot than they did at the peak of each prior expansion. My red circles point to how interest rates rested at zero when debt peaked during the 2008 worst recession since the Great Depression, which is where they essentially sit currently, while debt, alas, ramps ever higher:

And here's the proverbial icing on the cake.

My red circles are where debt peaked during the Great Depression and where interest rates were at the time; where it peaked in 2008 and where interest rates were at the time; and, alas, where interest rates currently sit -- the level where debt will peak this time is yet to be determined:

”

Of course this is not just a U.S. phenomenon.

Bottom line folks, great financial crises tend to come at the end of great private-sector debt cycles. A history that the powers-that-be are all too aware of. Hence their willingness to risk (accept/strive for) long-term stagnation to avoid the short(er)-term painful consequences of, frankly, conditions of their own making.

Whether or not they’ll “succeed” of course remains to be seen. Which is a risk we absolutely must hedge against as we otherwise work to exploit the opportunities inherent in an environment where policymakers will remain hellbent on, among other things, keeping interest rates, as well as the dollar, pinned to the floor…

In parts four and five we’ll explore some of those opportunities, as well as the risks, presented by today’s equity, commodity and currency markets' setups...

Thursday, December 24, 2020

Morning Note: "Profit Takes Care of Itself if"

With markets closing early today and equities (and our core portfolio) basically flat as I type (although the Russell 2000's down half a percent), I'll keep this morning's note short and sweet.

Wednesday, December 23, 2020

Morning Note: The Dollar is Key -- AND -- The Speculative Mood

Dow futures -- responding to the President's push back against the stimulus bill -- were at one point down ~200 points overnight.

This morning, however, is seeing the opposite, with the Dow up triple digits as I type.

The headline says the market's bouncing back despite the threat to the stimulus bill. While that's of course true by definition, it leaves out the likely catalyst for this morning's rally.

And, no, it's not the fact that weekly jobless claims -- still north of 800k -- came in lower than expected.

I'm thinking we can credit much of this morning's optimism to weakness in the dollar (strength in the euro and the pound) in response to news that a Brexit trade deal is close at hand.

Here's from Monday's morning note:

"Recall also in last week's video that, while I'm generally bearish on the dollar longer-term, the technicals have been pointing to a bottom, and I thus warned of a bounce that would "play havoc with stocks." We'll see if today isn't the beginning of something. Although a Brexit trade deal would I suspect quell the dollar's upside, at least momentarily."

Well, we've seen a bit of a bounce since last Tuesday's video, and it did play a bit of havoc with stocks.

White = the US Dollar Index, Blue = the Dow (note the near perfect negative correlation), through yesterday:

And here's adding on this morning:

Yes! The dollar will be key going forward...

Asian equities rallied overnight, with all but 2 of the 16 markets we track closing higher.

Same for Europe this morning, with all but 3 of the 19 bourses we track presently in the green.

U.S. major averages (save for the Nasdaq Comp) are nicely green as well: Dow up 179 points (0.59%), SP500 up 0.39%, Nasdaq down 0.04%, Russell 2000 up 0.44%.

The VIX (SP500 implied volatility) is down 5.57%. VXN (Nasdaq vol) is down 2.97%.

Oil futures are up 1.98%, gold's up 0.79%, silver's up 1.63%, copper futures are up 0.84% and the ag complex is up 0.83%.

The 10-year treasury's down (yield's up) and per the above the dollar's taking a hit this morning, down 0.37%.

In that our core mix expresses our longer-term weak-dollar thesis, our core portfolio, up 0.79%, is besting the overall stock market so far this morning.

Leading the way is energy, banks, silver, financials and base metals. Our only decliners on the morning are tech and Verizon.

We indeed see opportunities to exploit in a world where the central bank has managed its way into the proverbial corner; the narrowness of the path out (money printing, interest rate and dollar suppression) gives us unusual clarity (amid what are certain to be unusually volatile times) in terms of where probabilities lie sector by sector.

That said, sentiment, valuations, IPO fever, etc., (not to mention a corporate credit bubble) scream bubbly conditions that demand that we hedge in a manner that would mitigate the damage from a major market blowup.

I.e., the mood is speculative, to put it mildly:

"It is another feature of the speculative mood that, as time passes, the tendency to look beyond the simple fact of increasing values to the reasons on which it depends greatly diminishes. And there is no reason why anyone should do so as long as the supply of people who buy with the expectation of selling at a profit continues to be augmented at a sufficiently rapid rate to keep prices rising."

--Galbraith, John Kenneth. The Great Crash 1929Have a nice day!

Marty

Tuesday, December 22, 2020

PWA 2020 Year-End Letter Part Two: The "Momentum" We're Concerned With

Of all the things I might attest to, the notion that there’s much more to investing than passively riding the market wave would be one in which I'd have high conviction.

Quote of the Day: "A Bird in the Bush Is Worth Two in the Hand"

Financial reporter Michael Santoli speaks to the bubbly nature of today's stock market:

Morning Note: "Pork", That Wonderful Time of the Year, and Beware the Contagion of the Crowd

Imagine being handed a 5,600-page proposal and told you have to vote on its passing in just a few hours.

Well, welcome to Washington.

No, speed reading is not a requisite to public office. And, no, those who voted on the stimulus bill did not remotely know all that it contains.

Monday, December 21, 2020

Morning Note: The Bull/Bear Boat

With, as we've been reporting, standing room only on the bull side of the boat, and only crickets over on the bear side, it would make sense that a good news ("stimulus" coming [big in the U.S. and Japan])/bad news (more contagious COVID strain hitting Europe, plus Brexit trade talks still in turmoil) morning setup would see the market yielding to the downside.

Friday, December 18, 2020

PWA 2020 Year-End Letter, Part One: The Eagle, The Ice, and The Basketball

2020, a year to forget, but one we never will, is coming to a close…

Being that folks come here for insight into markets and economies, we’ll only touch on politics and pandemics in the context of markets and economies.

This year’s final message will come to you in several parts. Part One will focus on how we here at PWA metaphorically view the investing process.

Being that folks come here for insight into markets and economies, we’ll only touch on politics and pandemics in the context of markets and economies.

This year’s final message will come to you in several parts. Part One will focus on how we here at PWA metaphorically view the investing process.

Macro Update: Will This "End Well" For the Stock Market?

Since this is your weekly "macro" update, I should probably mention jobless claims, which, at 885k last week would typically provoke visions of utterly desperate equity markets. But, as you've noticed, equity markets are presently not interested in anything fundamental...

Morning Note: Fundamental Knowledge vs Perception

Tesla's inclusion in the S&P 500 on Monday will stir up a flurry of volume -- and potentially volatility -- near the market close today.

The utter enormity of the shuffling within the equity and derivatives markets that's about to occur... well... let's just say that the timing -- heading into a low-volume/liquidity time of year, and on a day when options and futures contracts on indexes, and on stocks themselves expire (so-called "quadruple witching") -- for making the biggest add to the S&P 500 Index ever was perhaps not all that well thought out...

Thursday, December 17, 2020

Quote of the Day: Surreal...

"The interest in participating in a bubble in something that precious few understand is truly disturbing. Then again, these are the same markets that saw investors buy Hertz after it declared bankruptcy, and the same markets gobbling up a century bond from Peru at 170 basis points over Treasuries. Dare I say, a world of negative bond yields in places like Italy, Spain, Portugal and now Greece."

Morning Note: Fantasy...

For reasons we'll explore in our year-end letter(s) (it'll come in several parts), the Federal Reserve has, over many years, manipulated itself -- well, the economy and the markets -- into a corner that leaves it (in the minds of its governors) left with no choice but to continue to inflate asset bubbles and, well, pray...

Wednesday, December 16, 2020

This Week's Message: Our Latest Messaging...

Since I'll be devoting much of my writing time over the next several days to our year-end letter, this week's main message will be some highlights of our recent messaging:

Morning Note: Coaxed

Asian stocks followed yesterday's U.S. rally into the night, with 14 of the 16 markets we track closing higher.

Europe's leaning green this morning, with 13 of the 19 bourses we track trading higher as I type.

U.S. major averages (save for the Russell) are barely off to start the day: Dow down 22 points (0.07%), SP500 down 0.01%, Nasdaq down 0.12%, Russell 2000 down 0.52%.

Tuesday, December 15, 2020

'Technical' Market Update (video)

Note: While I point to the setup for a technical bounce in the dollar, potentially playing havoc (if not provoked by) the stock market, I'm first looking at the potential for a leg lower off of Euro, and pound, strength in the event of a signed trade deal with the UK in the coming days.

Shortly thereafter is where I expect the short-term bullish technical setup for the dollar to play out...

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Morning Note: Why Patience Right Here?

While we've made some notable sector shifts over the past few months (with more on the horizon) -- gaining a more cyclical, and international, tilt to the overall mix -- we've yet to reduce our target fixed income exposure.

And for those of you who've recently either added capital to your existing portfolios, or are new clients to the firm, you've noticed that we're taking our time getting you to 100% of your personal target to our core portfolio.

Monday, December 14, 2020

Quotes of the Day: Bedeviling thinking pattern...

While establishing the format for our lengthy year-end client letter, I've decided to kick things off with 3 analogies I've offered up over the past 3 years to help folks understand what inspires and drives our disciplined approach to markets.

As I searched for blogposts that featured the ones I'm after, I stumbled across the following from a past "Quote of the Day."

"A Growing Insolvency Crisis"

As I suggested in this morning's note, markets these days are moved by a most myopic force.

By definition, that suggests that they may not be properly discounting longer-term reality.

And while, as we've stressed herein, there are clear opportunities to exploit in this world of top-down market manipulation, there are huge risks that prudent, thoughtful investors simply must hedge -- as we've been preaching since well before the pandemic hit...Morning Note: Acute Myopia

The EU and the UK hard deadline to ink a trade deal, well, wasn't so hard after all. Yesterday's news that they'll go the extra mile has global stocks in celebration mode this morning -- although the breadth among U.S. sectors is suspect (financials, industrials, materials and energy are actually down as I type).

Also helping equities (well, save for the key sectors mentioned above) this morning is optimism over U.S. budget talks, and more hints that global central banks will stay in the mood to print as far as the eye can see. Of course the latest vaccine news is notably bullish as well...

Friday, December 11, 2020

Macro Update: Back in the Red...

As our macro index has been climbing its way out of virtually unfathomable depths of late, I suspect you've noticed an air of skepticism in my commentaries.

That largely stems from my awareness of the sheer enormity of support the powers-that-be have brought to bear in their efforts to avoid what seemed destined to be a deep, protracted recession and historic bear market in asset prices.Morning Note: How Bubbles Form

Asian stocks traded mostly higher overnight, with 12 of the 16 markets we track closing in the green.

European equities, with a possible no-trade-deal Brexit on traders minds, is trading mostly lower so far this morning, with 14 of the 19 bourses we follow in the red.

U.S. major averages are (save for the Russell) leaning lower to start the day: Dow down 44 points (0.15%), SP500 down 0.33%, Nasdaq down 0.47%, Russell 2000 up 0.17%.

Thursday, December 10, 2020

Morning Note: "Awesome Stories" and The Dangers of Artificial Sweeteners

Asian equities leaned red overnight, with 9 of the 16 markets we track closing lower.

Europe's following suit so far this morning, with 15 of the 19 bourses we track down as I type.

U.S. major averages are mixed to start the day: Dow down 46 points (0.15%), SP500 down 0.07%, Nasdaq up 0.12%, Russell 2000 down 0.03%.

Wednesday, December 9, 2020

This Week's Message: Beating the Proverbial Dead Horse...

Well, as I begin to pen this week's main message I'm wondering how many ways I can spin my commentary around a setup that has stocks trading far removed from fundamental reality -- although our technical assessment has improved markedly.

I mean, from how many different angles can I continue to beat the proverbial dead horse?

Morning Note: Easy Peasy?

Asian equities continue their ascent; 11 of the 16 markets we track closed in the green overnight.

Europe's up as well so far this morning, with 14 of the 19 bourses we track trading higher.

U.S. Major averages are mixed, as I type: Dow down 62 points (0.20%), SP500 down 0.15%, Nasdaq down 0.16%, Russell 2000 up 0.29%.

Tuesday, December 8, 2020

Morning Note: Consumer Caution...

Asia once again leaned green overnight, with 9 of the 16 markets we track closing higher.

Europe, riding rising sentiment and vaccine prospects, while ignoring rising risk of a no-trade-deal Brexit come 12/31 (I'll be surprised if there's ultimately no deal), is mostly higher -- 13 of the 19 bourses we follow are in the green -- so far this morning.

US major averages, save for the Nasdaq Comp, continue to -- albeit slowly this morning -- climb a wall of extreme (dangerously extreme) optimism: Dow up 57 points (0.19%), S&P 500 up 0.11%, Nasdaq down 0.08%, Russell 2000 up 0.53%.

Monday, December 7, 2020

Morning Note: All Else Equal...

Asian equities traded mostly higher overnight, with 10 of the 16 markets we track closing in the green.

Europe's mixed as Brexit trade negotiations have hit an 11th-hour snag: 10 of the 19 bourses we track trading lower as I type.

U.S. major averages, save for the Nasdaq, are leaning lower: Dow down 160 points (0.53%), S&P 500 down 0.11%, Nasdaq up 0.43%, Russell 2000 down 0.21%.

Sunday, December 6, 2020

Potentially Problematic Complacency, Except in Futures...

Like I said last week, the bull side of the boat is presently a standing room only affair, and -- contrarianly-speaking -- that's not necessarily a good thing...

Friday, December 4, 2020

Macro Update: We May Be Onto Something...

Our proprietary macro index remains, for the second consecutive week, out of the red, although still not in the green either. Its overall score rested at 0 this week.

Morning Note: One Common Theme to Crises

Just the numbers this morning... well, I'll probably throw in a quote... then our weekly macro update later today (tomorrow at the latest).

Thursday, December 3, 2020

Morning Note: The Torment 😎

Asian equities traded mostly higher overnight, with 12 of the 16 markets we track closing in the green.

Europe, well, not so much. 10 of the 19 bourses we follow are in the red so far this morning.

U.S. major averages are solidly in the green early in the session: Dow up 142 points (0.47%), S&P 500 up 0.17%, Nasdaq up 0.35%, Russell 2000 up 0.99%.

Wednesday, December 2, 2020

This Week's Message: What We Know - And - What's Not To Like?

This week's main message will be short and sweet. It'll essentially be me doing a little thinking out loud...

Morning Note: "To consort with the crowd is harmful"

Asian equities traded mostly green overnight, with 10 of the 16 markets we track closing higher.

Tuesday, December 1, 2020

Morning Note: Never Content With "Discoveries Already Made"

Allow me to offer up the opposite to yesterday's metaphor, as asset prices, the world over, are swimming in a sea of green to start the month of December.

Monday, November 30, 2020

The Ultimate Object of the Fed's Affection...

Listening to RealVision managing editor Ed Harrison this evening has me thinking about my recent conversations with clients during our portfolio review sessions.

Morning Note: The Elephant in the Boat

Asset prices, the world over, are swimming in a sea of red as we start the week.

Friday, November 27, 2020

Macro and Sentiment Update: Our Index Is Out of the Red! And Positioning's A Bit Precarious

Well, for the first time since October 2019 our PWA Macro Index is out of the red. Can't quite say "in the green", since it presently scores a 0. But what a rebound off of a -82.69 back in June!

Morning Note: Wall Street's Incentives...

Just a couple of quick notes this morning, first this morning's numbers, then I'll follow with something light after I score our weekly macro and sentiment indexes.

Wednesday, November 25, 2020

Chart of the Day: Are the latest gains "durable"?

In our client review meetings these days I of course expound on much (the good and the bad) of what you've read herein, and when it comes to the historic chasm that separates current stock prices from underlying fundamentals I typically declare that the major averages would need to decline by easily two-thirds (a bit more than the '08 experience) to catch down to present reality.

This Week's Message: This Ain't About Capitalism...

As I've suggested herein of late, it's not a stretch to surmise that the near-term path of least resistance for the stock market is most likely higher (not a prediction mind you!).

Morning Note: "Obvious Things"

Asian stocks were mixed overnight, with 9 of the 16 markets we track closing lower. Same for Europe this morning, with 9 of the 19 bourses we follow currently in red. U.S. major averages, save for the Nasdaq, are giving a little back so far this session; Dow down 176 points (0.58%), S&P 500 down 0.27%, Nasdaq up 0.13%, Russell 2000 down 0.53%.

Tuesday, November 24, 2020

Morning Note: Gold's Woes, and a couple tweaks...

Positive vaccine news, improving global data, political certainty and an incoming US treasury secretary with a penchant for easy money has stocks in rally mode this week.

Monday, November 23, 2020

Morning Note: How To Tell Good From Bad Economists

Optimism pretty much reigns globally this morning, as positive news on Astrazeneca's vaccine added to recent promising reports from Pfizer and Moderna, and the readings from purchasing manager surveys (PMIs) say business, particularly among global manufacturers, is picking up notably, as are costs, per our view on inflation going forward.

Friday, November 20, 2020

Macro Update: A Little Something for Everybody

I've been hinting that many of what we deem to be pertinent data points have been flashing threatening signals of late. However, per this week's analysis, not yet to the point that has us lowering their scores.

In fact, thanks to an uptick in mortgage purchase applications (our only needle-mover this week), our overall score moved yet another notch closer to the green; this week we're at -4.08.

Morning Note: Careful What You Ask For!

U.S. stocks have found sanguinity at the open this morning, after getting rocked a bit overnight by news that the Treasury has no interest in expanding emergency assistance measures and asked the Fed to return all remaining funds to the government. Secretary Mnuchin's comment this morning that folks are misinterpreting the message I suspect helped calm the waters a bit.

Thursday, November 19, 2020

Well, Wow!!

So, a little bit ago I stuck my head in the fridge and saw this can labeled "Starbucks Doubleshot Energy" and, well, the following happened.

Read at your leisure... 😎

Regular readers may have noticed that I've warmed a bit more lately to the notion that there may very well be some upside left in stocks from here (of course, particularly short-term, one never knows). And that's despite the reality that 20 million Americans remain on some form of unemployment assistance, that we're operating amid a corporate debt bubble that is not only the largest in history, but its credit quality in the aggregate is, well, horrendous; some $1.4 trillion of corporate debt literally sits on the balance sheets of insolvent companies yet to implode, and, well, there's more (read this week's main message), but you get the gist.

Morning Note: No Limits

Asian stocks traded mostly higher overnight, with 10 of the 16 markets we track closing in the green. Europe's nearly across-the-board weak this morning, with all but 2 of the bourses we track in the red. U.S. major averages are mixed: Dow down 45 points (-0.15%), S&P 500 flat, +0.02%, Nasdaq up 0.55%, Russell 2000 down 0.21%.

Wednesday, November 18, 2020

Morning Note: Windy Out There!

Asian equities traded mostly positive overnight, with 11 of the 26 markets we track closing in the green. Europe is beginning the day in opposite fashion vs yesterday (all but 2 bourses were down), with all but one of the 19 bourses we track trading nicely higher. U.S. major averages are a bit mixed this morning: Dow up 96 points (0.32%), S&P 500 up 0.14%, Nasdaq down 0.11%, Russell 2000 up 0.39%.

This Week's Message: A New Paradigm: A Synopsis of Our View on Probabilities From Here

It is virtually impossible for general conditions to get back to pre-covid levels, if, for example, general conditions include the balance sheet condition of US institutions.

Tuesday, November 17, 2020

Quote of the Day: "The One Reality"

While our present view of probabilities going forward has us exploiting what we believe to be truly viable opportunities, we recognize the uniqueness, and immense challenge inherent in what's about to unfold. And we do not envy the new investor who is just now entering the fray, with uber-high expectations.

Inflation and Interest Rates May Not 'Quite' Go Hand-in-Hand Next Year...

As I've suggested lately herein, I'm leaning toward the rising inflation camp as we move firmly into 2021. Which is a position at odds with that of a number of economists/macro thinkers whom I have great respect for.

Morning Note: "A key in 2021"

Asian equities fared okay overnight, with 12 of the 16 markets we track closing modestly in the green. Europe, on the other hand, is in a sour mood this morning; all but 2 of the 19 bourses we track are trading lower as I type. U.S. Major averages are taking a breather this morning as well: Dow down 316 points (-1.06%), S&P 500 down 0.77%, Nasdaq down 0.34%, Russell 2000 down 1.47%.

Monday, November 16, 2020

Morning Note: A Unique Display

In last Monday's morning note we put numbers to an impressive rally on the back of news that Pfizer's covid vaccine was looking to be hugely (90%) effective. And here we are, one week later, and reports from Moderna suggest the same for theirs (94% effective!).

Saturday, November 14, 2020

Quotes of the Day: The Stock Market Would Absolutely Love Janet Yellen At the Treasury Helm!

In yesterday's morning note I shared the following from my recent entry to our internal research thread:

Friday, November 13, 2020

Macro Update: Forget About Normalcy...

While 6 of the 49 inputs to our proprietary macro index saw their scores change this week, they essentially balanced each other out: Our overall score remained stuck at -6.12 for the third consecutive week:

Morning Note: I'm Relatively Constructive, However, The Irremediable Looms...

Asian equities traded in mixed fashion overnight, with half of the 16 markets we track closing higher, half lower. Europe, holding up against rising covid numbers and faltering Brexit trade talks, is seeing 12 of its 19 bourses we follow in the green so far this morning. U.S. major averages are holding up against the same in terms of covid, and appear unconcerned over the domestic political backdrop: Dow up 198 (0.68%), S&P 500 up 0.69%, Nasdaq up 0.39%, Russell 2000 up 1.78%.

Thursday, November 12, 2020

Morning Note: "One Major Problem In Investing"

Asian stocks took a breather last night from what's been an impressive rally of late; 12 of the 16 markets we track closed in the red. Europe's giving some back this morning as well, with 14 of the 19 bourses we follow trading lower. U.S. major averages, save for the Nasdaq, are not feeling it either: Dow down 149 points (0.51%), S&P 500 down 0.30%, Nasdaq up 0.27%, Russell 2000 down 0.55%.

Wednesday, November 11, 2020

Morning Note: Bad Breadth

Asian equities on-balance continued their winning streak overnight, with 11 of the 16 markets we track closing in the green. Europe's once again in the green as well, with 17 of the 19 bourses we track trading higher, as I type. U.S. major averages, however, are mixed: Dow down 45 points (0.15%), S&P 500 up 0.46%, Nasdaq up 1.38%, Russell 2000 down 0.72%.

Tuesday, November 10, 2020

Chart of the Day: Leaders Rolling Over

While what's worked (namely the FAAMGs) year-to-date has been rolling over of late, concentration among the S&P 500's largest 5 positions (FAAMG) still sits way above the previous tech-bubble high (top).

Morning Note: Folks Like Company

Asian equities put in another positive performance overnight, with 13 of the 16 markets we track closing higher. Europe's following suit this morning, with 16 of the 19 bourses we follow in the green thus far. U.S. major averages, on the other hand, are all over the place: Dow up 77 points (0.27%), S&P 500 down 0.65%, Nasdaq down 1.93%, Russell 2000 up 0.11%.

Monday, November 9, 2020

This Week's Message: Just a Peek Into The End-Game of the Debt Super-Cycle

I thought the following section of an email conversation with a savvy friend and long-time client on Sunday would be instructive for our readers. It was in response to his feedback regarding a superb essay that I discovered over the weekend and excerpted from -- in response to my friend's emailed question/comment regarding Saturday's blog post -- to emphasize much of what I've been writing about over the past year+.

I'll add parenthetic clarity where I think it's needed. I'll also add emphasis where my comments relate to today's rally.

Speaking of today's rally; while the Dow closed up over 800 points (2.95%), the S&P 500 managed only a 1.17% gain, while the Nasdaq Composite actually closed down 1.53%. Our core allocation closed up 1.21%:

Morning Note: Stay Tuned...

Vaccine optimism has global stocks screaming higher this morning. Pfizer's vaccine, in a large study, reportedly prevented 90% of infections. Cause for celebration (or at least great anticipation), for obviously much more than investment purposes!

Saturday, November 7, 2020

Trapped

The following from Hoisington Capital Management's (home of revered macro thinker Lacy Hunt) latest must-read quarterly newsletter should sound very familiar to clients and regular readers: emphasis mine...

Friday, November 6, 2020

Macro Update: Fuggetabout Tomorrow

Our proprietary macro index (-6.12) broke even on the week; with two inputs improving, two deteriorating:

Morning Note: Swept Up In Moods

The Bureau of Labor Statistics (BLS) October jobs report (released this morning) looks markedly better than this week's ADP report (mentioned in yesterday's morning note). Nonfarm payrolls increased by 638k vs 580k estimated. Permanent jobs losses remain at 3.7 million (among the 20 million still without work), but "remain" is the operative word. I.e., the number came in flat in October after major increases over the previous two months. More on this to come in this week's macro update.

Thursday, November 5, 2020

Morning Note: Don't Be the Dolt

Well, that warm, fuzzy feeling you might be having over this week's rally in stocks maybe should be tempered a tiny bit.

I'm not talking politics, I'm talking economics.

Wednesday, November 4, 2020

Market Commentary (video)

In today's video commentary I illustrate the messy internals in today's equity market rally, reflecting a shift in election expectations, I make the case for commodities and I briefly touch on a handful of our weekly analyses.

IF VIEWING FROM YOUR MOBILE PHONE, CLICK "VIEW WEB VERSION" AT THE BOTTOM OF YOUR SCREEN.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Chart of the Day

In this morning's note I alluded to a rotation that's taken place the past few weeks, from the high-flying techy names to the value "reflation" names. I also suggested that the premise beneath today's reversal of that trend is ultimately faulty.

Morning Note: Whimsical

If you look at the major U.S. stock market indices this morning you'd think all's well on Wall Street. But if you open a few doors and peak inside, well, hmm...

Tuesday, November 3, 2020

Morning Note: A Wiley Sort of Market???

If you're looking for something pithy and provocative on the election this morning, well, you won't find it here. And if you're baffled by this morning's 580-point Dow rally, I hear ya. That said, if all I knew at the moment was that the dollar was down 0.74% (that's big), I'd say, given the present setup, and where the dollar -- and stocks -- have been of late, a big stock market rally today is a no brainer.

Could it be that "the market" is already looking past the election? Perhaps, but a 35 VIX (pricing of volatility in SP500 options) says that traders, despite this week's rally, are hugely on edge. Let's hope it's not a Wile E. Coyote sort of edge, if you know what I mean.

Monday, November 2, 2020

Core Performance Update (video)

See year-to-date results for global equity markets and commodities beneath the video player below.

Morning Note: Entering New Territory

October Purchasing Managers Indices (PMI) were released last evening for much of the world, and, per much of the world scoring above 50, much of the world's economy improved (vs September) last month. That, I suspect, plus -- in the face of covid lockdowns and a contentious U.S. election -- some dip-buying following the worst week since March for global stock markets has stocks in rally mode this morning.

Saturday, October 31, 2020

Core Positioning Update (video)

SPECIFICALLY FOR CLIENTS: Here's our latest positioning update where I illustrate the whys and wherefores of the adjustments we've made since mid-year, including how we're currently handling our cash/fixed income exposure, as well as why we're about to re-establish a modest position in AT&T.

Note: Where I make reference to a sector that has "performed well" this year, I'm speaking on a relative basis (coming off of the March low); 7 of the 11 primary U.S. equity sectors remain notably in the red on the year; as do 41 of the 47 foreign equity indices we formally track.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Friday, October 30, 2020

Macro Update: Pulling Forward

For the second week in a row our macro assessment, via our proprietary index, shows net improvement. The PWA Macro Index gaining 2.14 points, to -6.12:

Missing Out On the Most Important Phase of the Business Cycle!

Taking a break from this morning's macro grind, I thought I'd share this short back and forth between myself and Nick in our firm's chatroom a little while ago:

Morning Note: With the End of Uncertainty

Asian equities, save for Vietnam's, took a bath overnight, with all but 1 of the 16 markets we track closing in the red. Europe, on the other hand, is showing a little strength this morning, with 10 of the 19 bourses we follow trading higher. U.S. major averages look more like Asia did last night so far this morning: Dow down 179 points (-0.67%), S&P 500 down -0.90%, Nasdaq down -1.57%, Russell 2000 down -1.07%.

Thursday, October 29, 2020

Chart of the Day: Tim Cook on Q4, "I dunno"

This (big decline in what folks expend to spend on Christmas this year):

Explains this (Apple offering no calendar Q4 guidance):

Morning Note: Abnormal Reaction -- And -- Man's Search for Meaning

Just in the course of my morning routine of perusing overnight and early morning data and developments, the Dow went from up mid-double digits (surrendering a 300+ rally in futures trading last night) to down 220 points to up 155 as I type. I would tell you to buckle up, but you're not trading this noise, right? Say "right."

Wednesday, October 28, 2020

This Week's Message: The Inevitable Consequence

Hmm.... I find myself struggling a bit to get this week's message going. The plethora of stuff we can cover has me doubly challenged. My aim is to hook you from the get go (as this is directed to you clients, and I want you understanding the whys and the wherefores that instruct our decisions regarding your money). And while hook you I may, my main objective is to get you all the way to the net before releasing you back into the turbulent waters we find ourselves swimming in these days.

So I'll keep brevity in mind as I focus on relevance...

Morning Note: Sell Mode

Lack of a bazooka stimulus plan happening pre-election in the U.S. and covid numbers spiking the world over has global equities in sell mode once again this morning. 11 of the 16 Asian markets we track closed lower overnight. 18 of the 19 European bourses we follow are trading down (big) as I type. U.S. major averages are off notably across the board: Dow down 630 points (-2.30%), S&P 500 down -2.26%, Nasdaq down -2.56%, Russell 2000 down -2.74%.

Tuesday, October 27, 2020

Morning Note: Words To Live By

Asian equities closed mostly lower overnight (but not bad considering yesterday's rout in U.S. markets), with 10 of the 16 markets we track in the red. Europe's definitely having a rough go of it, with 16 of the 19 bourses we follow currently trading lower. U.S. stocks are struggling to find direction this morning: Dow down 110 points (-0.40%), S&P 500 down -0.15%, Nasdaq up 0.37%, Russell 2000 down -0.42%.

Monday, October 26, 2020

Quick note on today's action...

Well, you know me, it's hard to stay silent on a morning when the Dow was at one point down over 900 points, so allow me to blab for a couple of minutes on what I'm thinking.

Morning Note: Too Easy to Forget

Asian equities leaned lower overnight, with 10 of the 16 markets we track closing in the red. Constructive Brexit headlines can't overcome a notable spike in Covid-19 cases across Europe, with all 19 bourses we track currently trading lower. Stalling stimulus talks and higher Covid numbers has the dollar rising and U.S. stocks falling so far this morning: Dow down -652 points (-2.35%), S&P 500 down -1.98%, Nasdaq down -1.51%, Russell 2000 down -2.64%.

Friday, October 23, 2020

Macro Update: The Hand We're Dealt

This week saw a notable improvement in our proprietary macro index; up 4 points to a net overall score of -8.16.

Morning Note: "At the right price, markets function"

Asian equities traded mostly higher overnight, with 11 of the 16 markets we track closing in the green. European markets are liking the news out of their auto sector, plus I suspect optimism around Brexit isn't hurting either, as 16 of the 19 bourses we follow are in the green as I type. U.S. stocks are searching for direction this morning as disappointing earnings reports from chip makers has tech trading a bit lower: Dow up 28 points (0.10%), S&P 500 up 0.13%, Nasdaq down -0.35%, Russell 2000 up 0.17%.

Thursday, October 22, 2020

Morning Note: The "Worst Risk-Reward Profile" (of credit markets)

Asian equities traded in mixed fashion overnight, as 9 of the 16 markets we track closed in the red. Less than rosy economic reports and rapidly rising covid numbers have European stocks down nearly across the board this morning; 16 of the 19 bourses we follow are lower as I type. U.S. major averages remain choppy, as traders await final word on a pre-election "stimulus" package; Dow down 116 points (-0.41%), S&P 500 down -0.40%, Nasdaq down -0.65%, Russell 2000 down 0.19%.

Wednesday, October 21, 2020

This Week's Message: With Clarity Comes Opportunity, But Patience Is Key...

I'm taking this week's main message from an entry to our internal log that I penned last weekend (adapted/edited to be featured herein).

While, in it, I pull no punches, I want to be careful not to leave you with an all-hope-is-lost feeling.

Morning Note: For Every Complex Problem

Asian equities traded mostly higher overnight, with 10 of the 16 markets we track closing in the green. While the pound and the euro are loving the positive Brexit (talks) news this morning, European equities aren't feeling it; 17 of the 19 bourses we follow are trading lower as I type. US major averages (save for the Russell) were initially liking the sound of a 48-hour deadline (call it an extension) to get another trillion or three of much needed "stimulus" (call it "support") approved; at the moment, however, not so much: Dow down -48 points (-0.17%), S&P 500 down -0.09%, Nasdaq down -0.07%, Russell 2000 down -0.87%.

Tuesday, October 20, 2020

Morning Note: Toppy Phenomena

Asian equities traded mostly higher overnight, with 10 of the 16 markets we track closing in the green. Europe's doing well as well, with 13 of the 19 bourses we track up as I type. U.S. major averages are reflecting newfound optimism that a stimulus deal will happen by the end of the day (decent [but not guaranteed] bet I suspect): Dow up 206 points (0.73%), S&P 500 up 0.70%, Nasdaq up 0.42%, Russell 2000 up 0.26%.

Monday, October 19, 2020

Morning Note: The Prelude (well, reminiscent of a past prelude)

Asian stocks traded mostly higher overnight, with 12 of the 16 markets we track closing in the green. Europe, not so much this morning; 11 of the 19 indexes we follow are trading lower as I type. The U.S. major averages, trading on virtually nothing (for the moment) but the prospects for fiscal stimulus, have been all over the place as today's session gets underway. At the moment: Dow down 24 points (-0.06%), S&P 500 down -0.13%, Nasdaq down -0.25%, Russell 2000 up 0.44%.

Sunday, October 18, 2020

Random notes from our research thread...

Being surrounded by what I feel blessed to say is an amazing support team allows me to spend most of my time deep in the weeds of markets and of macro conditions.

Saturday, October 17, 2020

Macro Update: Yep, Unprecedented...

I'll let JPMorgan CEO Jamie Dimon set the stage for this week's macro update:

“The word unprecedented is rarely used properly. This time, it’s being used properly. It’s unprecedented what’s going on around the world, and obviously Covid itself is a main attribute. The economy would be in shambles without the safety net of the CARES Act. In a normal recession unemployment goes up, delinquencies go up, charge-offs go up, home prices go down; none of that’s true here. Savings are up, incomes are up, home prices are up. So you will see the effect of this recession; you’re just not going to see it right away because of all the stimulus.”

Friday, October 16, 2020

Morning Note: Financial Gravity Suspended

Friday is definitely on my top-7 list of favorite days of the week, as it's the day I score our macro index, so I'll be keeping this morning's note short and sweet.

Thursday, October 15, 2020

Morning Note: There's Absolutely A Market For Treasuries

Increasing covid case numbers and lack of agreement on US fiscal stimulus has markets in a risk-off mood round the world. All but two of the 16 Asian equity markets we track closed lower overnight. Europe -- seeing rising covid numbers and proposing new lockdowns -- is red (19 of 19 markets we track) across the board. US major averages are all off this morning as well: Dow down 162 points (-0.57%), S&P 500 down -0.76%, Nasdaq down -1.19%, Russell 2000 down -0.66%.

Wednesday, October 14, 2020

This Week's Message: No Hunch or Hyperbole

The treasury secretary told Bloomberg News this morning that:

"U.S. DEBT MUST BE DEALT WITH OVER NEXT 10 YEARS."

Yep.... hmm... well... uhhhh... yyyyeah... that's good. Because, well, here's how the future of Federal debt is shaping UP:

Morning Note: The Great One's Greatest Discovery

Quick one for you this morning (our main weekly message to follow soon).

Asian equities were mixed overnight; 9 markets we track down, 7 up. While Brexit headlines remain concerning, the pound (unlike yesterday) is suggesting something constructive is in the works (+0.83% this morning). European stocks are leaning green, with 11 of the 19 bourses we follow presently higher on the session. US major averages are mixed: Dow +17 points (0.06%), S&P 500 up 0.09%, Nasdaq up 0.07%, Russell 2000 down -0.26%.

Tuesday, October 13, 2020

Quote of the Day: B, B, & B Battening Down

Well, time will tell if the stock market has it right this go-round, or if indeed we're staring down the latter stages of the third epoch bubble in one-fewer decades (remarkable, if so, but explainable, as I'll attempt to do in tomorrow's weekly message).

Morning Note: Patient

Investor expectations in Europe are tanking (per September survey readings), covid cases in Germany are rallying at their fastest pace since April and UK's Boris Johnson says a no-deal Brexit is essentially no big deal. I.e., the euro and the pound are getting pounded this morning, therefore, the dollar's in rally mode. Therefore, while stocks are feeling it, commodities are definitely taking it in the chin.

Monday, October 12, 2020

Quote of the Day: Goes With Our Charts of the Day: Hmm...

In my earlier "Charts of the Day: Hmm..." post I featured visuals showing the session's rise of NDX (Nasdaq 100 Index) and VXN (tracks implied volatility of NDX) and noted that days like today -- both rallying hard -- were rare.

Coincidentally, Bloomberg's Ye Xie noticed it as well and dug into the weeds a bit to find out just how rare the phenomenon has been, and what it typically spells in terms of near-term risk.

Well, following the other 4 times this (and a few other times that were a little less pronounced) has occurred since 2001, VXN did indeed serve as a legitimate short-term warning signal:

"(Bloomberg) -- It’s deja vu all over again. A surge in tech

stocks Monday was accompanied by higher volatility, offering an

eerie reminder of the August stocks melt-up that laid the

groundwork for September’s correction. In fact, it’s only the

fifth time since 2001 when the NDX rose more than 3% and VXN

increased at least 0.8 points. If we lower the threshold for the

NDX to a 2% gain, it’s still a fairly rare occurrence. And the

historical performance in the next two weeks aren’t really

encouraging."

For us, this is simply short-term stuff and nothing actionable at this point. But it's worth noting that all occurrences either came amid bear markets or, in one instance (2015), a double-digit correction.

Charts of the Day: Hmm...

As I type the Nasdaq 100 Index (read tech) is staging one heck of a rally, up 3.21% on the day thus far (although giving a bit back the past hour or so):

Morning Note: Moved by Hopes

Either because of, in spite of, or oblivious to a concerted effort by China to cheapen its lately-strengthening currency (one could make attendant bull or bear cases for the rest of Asia) Asian equities mostly rallied overnight, with 12 of the 16 markets we track closing in the green. Brexit talks this week are all the talk in Europe, and the action in equities and currencies (despite the warning cries) says the UK won't be busting out without a trade deal (the overwhelming political risk makes that my base case as well); all but 4 of the bourses we follow are trading higher so far this morning. U.S.'s major averages, expecting more stimulus (it'll come, whether it's pre or post election), anticipating special stuff out of Apple's big day tomorrow, and betting that positives will emerge from bank earnings results this week are nicely higher as I type: Dow up 269 points (0.94%), S&P 500 up 1.44%, Nasdaq up 2.13%, Russell 2000 up 0.51%.

Friday, October 9, 2020

Macro Update, More on the Debt Mess, and a Synopsis of Our General Thesis

"The real opportunities in macro, you have to wait for. You don't always have to be doing something.

Having lived a few of these markets before, you have to be very careful because you can lose P&L very quickly by getting too excited."

--Raoul Pal, 10/9/2020 RealVision Daily Briefing

Raoul is RealVision's founder and CEO, and one of today's great macro thinkers. Of course I'm quoting him today because, as clients and regular readers know, his comments echo our present thinking...

Thursday, October 8, 2020

Morning Note: "Social Sciences Always Start From Problems"

The on again stimulus talks are giving legs to this week's rally, in the face of another 840k folks filing first-time unemployment claims (worse than expected), while nearly 11 million stay on the rolls (although that was fewer than expected). Asian equities rallied overnight nearly across the board, with 14 of the 16 markets we track in the green. Europe's nothing to sneeze at either; 15 of the 19 bourses we follow trading higher this morning. U.S. major averages are up across the board as I type: Dow up 88 points (0.31%), S&P 500 up 0.57%, Nasdaq up 0.36%, Russell 2000 up 0.73%.

Wednesday, October 7, 2020

This Week's Message: All One Can Do

I think it's safe to say that history has never concluded a setup like the current without seeing stocks suffer a significant, protracted bear market in the process (the Feb/March experience btw doesn't come close). So the question has to be, how does one manage a portfolio amid historic certainty that before the next true expansion or bull market gets underway stocks will experience major, extended losses?

Morning Note: Beholden to stocks...

Equity markets are attempting to claw back yesterday's losses, as the President claws back yesterday's no-stimulus-till-post-election pledge: A perfect example of how tweet-possessed traders have become, and how strong the belief in the reflexive nature of the stock market; i.e., that rising stock prices engender robust animal spirits (economic action), and vice versa.

Tuesday, October 6, 2020

Morning Note: Financial Progress Is, Alas, Cyclical

Asian stocks for the most part continued their rally into the week, with 12 of the 16 markets we track closing higher overnight. Same for Europe, with 14 of the 19 we follow in the green so far this morning. U.S. major stocks are more or less hanging in there as well: Dow up 116 points (0.41%), S&P 500 up 0.12%, Nasdaq flat -0.01%, Russell 2000 up 0.99%.

Monday, October 5, 2020

Quote of the Day: The Popular Mind

If I had a nickel for every time someone has asked me since the market recaptured, say, the first 50% of the Feb/March selloff how stock prices can so defy economic reality, well, yeah, lots of nickels...

Morning Note: Risk Is Rallying

Optimism over US fiscal stimulus prospects and positive commentary around the President's present condition is overcoming news of re-lockdowns in New York City, Spain, France, UK and the Czech Republic as global markets get underway this week.

Wednesday, September 30, 2020

Quote of the Day: The "Real Second Wave"

Okay, just one more before I go quiet for a few days. This speaks as much as anything as to why we continue to sound a cautious note...

Macro strategist Julien Brigden tweeted this today above a Bloomberg news search titled "job cuts, firings, layoffs."

This Week's Message: Where We Presently Stand

In a recent weekly message we scratched the surface of the presently popular inflation/deflation debate among some of today's brightest macro thinkers. This week we're going to take a deeper dive into that discussion and clue you in to where we presently stand on the issue and how we expect to manage it going forward.

Morning Message: The Carnival

In yesterday's morning note I pointed out what motivates policymakers these days (the market). If you happen to struggle with that, with my cynicism that is, well, struggle away.

It's not that I don't get that a buoyant market leads to confidence and a buoyantly-spending consumer, it's that 36 years of experience and the study of 360+ years of history tells me that such irresponsible pumping of markets and allocation of public resources tends to ultimately lead to extreme financial pain, not only for the unsuspecting investors who get sucked in, but for the folks who truly need the help, as deflating bubbles deflate the desire, if not the means, to consume beyond one's basic necessities, destroying opportunity in the process.

Tuesday, September 29, 2020

Morning Note: Forgive Me My Cynicism

“We definitely need another round of stimulus here, not only for confidence for the American public and workers, but also for the markets,” Michelle Connell, the owner and president of Portia Capital Management, said on Bloomberg Television. “Going into this election, that would definitely help.”

Allow me to tweak that statement just a bit to capture the fundamental belief that guides the powers-that-"stimulate"- in today's top-down, big-government world:

Monday, September 28, 2020

Quotes of the Day: "Rushing Out" Onto That Ice

In Saturday's video commentary I suggested that the last time the ice on the lake (my metaphor for equity markets) was this thin and the temperature this warm the ice ultimately broke.

Morning Note: World in Rally Mode This Morning

Surprisingly good industrial production numbers out of China (I'll suspend the caveats galore this morning), a bit of optimism over Europe's 2021's prospects/hope over Brexit talks this week, and the anticipation of another bazooka fiscal stimulus package in the U.S. -- and/or a bit of that Pavlovian dip-buying -- has world markets rallying this morning.

Sunday, September 27, 2020

God's Greatest Work

Well, faithful readers, I'll be giving you a break next Thursday thru Sunday. No morning notes, no quotes of the day, no macro update, etc., to take in, as I'll be attempting at least to force upon myself a rare few days of disconnectedness.

Typically, when I find myself away from my normal surroundings I remain engaged (connected) until the clock strikes one (pt), but this time the plan is to be fully engaged in what I'll say is -- outside of first my family, then markets and economies -- my one true passion, fly fishing. And it'll have my fullest attention while markets are trading the latter part of next week.

Hence, me re-posting the message below (I'll be joining a dear friend whom I first met in early fall 2008 and introduced to my readers back in 2010, this time on the Missouri River in Helena, Montana).

Only continue if you're in the mood for something non-financial...

Saturday, September 26, 2020

Macro and Market Update (video)

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Friday, September 25, 2020

Morning Note: Seeing That Commodities Dip We Were Hoping For, But Wait...

Asian equities were mixed overnight, 10 markets we track closed up, 6 down. Europe's suffering so far this morning, with only 3 of the 19 markets we track trading higher. U.S. stocks are starting the day in the red as well: Dow down 100 points (-0.37%), S&P 500 down -0.38%, Nasdaq down -0.19%, Russell 2000 down -0.52%.

Thursday, September 24, 2020

Morning Note: Speaking of the Dollar

Asian equities, no surprise, got hammered overnight, with all but 2 of the markets we track closing notably in the red. Europe's sliding as well this morning, with all but 3 of the 19 bourses we follow trading lower. U.S. stocks have been all over the place this morning: As I type: Dow down 40 points (-0.15%), SP500 down -0.16%, Nasdaq down -0.10%, Russell 2000 down a big -1.48%.

Wednesday, September 23, 2020

Morning Note: The Rise of Leverage

Asian equity markets were mixed overnight; 9 down, 7 up. Europe's hanging in there; 13 of the markets we track are higher, 6 are trading lower as I type. The U.S.'s major averages are struggling one hour into today's session: Dow (despite Nike) down 38 points (0.14%), S&P 500 down -0.53%, Nasdaq down -0.85%, Russell 2000 down -1.08%.

This Week's Message: "Awesome Time to Be Alive"

We'll start this week's message off by looking at the data I shared in our internal research call yesterday afternoon. The topic was the day's market internals.

The reason I'm using yesterday's action as my segue to this week's message is because in a number of ways it serves as a nice microcosm of the 2020 equity market to date.

Tuesday, September 22, 2020

Morning Note: Messy

Asian equities continue to struggle this week; 13 of the 16 markets we track closed down notably overnight. European stocks are fairing better this morning with 15 of the 19 bourses we follow presently in the green. U.S. stocks are struggling just a bit to start the day: Dow down 36 points (0.13%), S&P 500 flat, up 0.06%, Nasdaq flat, up 0.03%, Russell 2000 down -0.60%.

Monday, September 21, 2020

Morning Note: Nowhere to Hide (This Morning)...

Yet another jolt to the U.S. political setup, Covid breaking above March's numbers in Europe and a concerning report on major global banks and their alleged relationships with "dangerous players" over the past two decades has world asset markets on edge this morning.

Saturday, September 19, 2020

Charts of the Day: Comfortable Being in the Minority

In yesterday's macro update I mentioned that

"...not everyone agrees with our presently cautious bent. I mean, some folks actually believe now's the time to take the leap and buy the recent dip with both fists."

Well, that's putting it mildly!

Friday, September 18, 2020

Macro Update: Is the Reopening Bounce Fading?? -- And -- Careful Taking That Leap!

Our proprietary macro index gave up 4 points this week; net score -14.00.

Morning Note: "It Ain't Ever Different"

Asian equities, on balance, rallied a bit overnight, with 10 of the 16 markets we track closing in the green. Europe, on the other hand, is struggling so far on the session, with only 3 of the 19 bourses we track presently in the green. U.S. equity averages are essentially flat. Dow down 58 points (-0.21%), S&P 500 down -0.08%, Nasdaq up 0.15%, Russell 2000 up 0.28%.

Thursday, September 17, 2020

Morning Note

Asian equities got hammered overnight, with all but 2 of the markets we track closing in the red. Europe, while well off the session lows, is taking a beating this morning as well; all but 5 of the 19 bourses we follow presently trading lower. U.S. stocks, also presently off the session lows, are red across the board as I type: Dow down 63 points (-0.22%), S&P 500 down 0.85%, Nasdaq down 1.42%, Russell 2000 down 1.31%.

This Week's Message: History's Rhymes

In our effort to keep you informed as to what we're thinking in the here and now we're forever highlighting herein the at-the-moment trends and developments that instruct our entries into, exits out of, and hedges on various asset classes and securities. Underneath it all of course is the broad macro picture, global general conditions, if you will, that command our attention (analyzing, interpreting, testing, hypothesizing) on virtually a 24/7 basis.

Wednesday, September 16, 2020

Morning Note: More on the Disconnect

Asian equities had a mixed session overnight, with 7 of the 16 markets we track closing lower. Same for Europe this morning, 9 of the 19 bourses we follow currently in the red. And "mixed" pretty much characterizes U.S. stocks to start today's session: Dow up 91 points (0.32%), S&P 500 up 0.11%, Nasdaq down -0.19%, Russell 2000 up 0.75%.

Tuesday, September 15, 2020

Quotes of the Day: Beware the "Self-fulfilling Mechanisms"

Just began digging into the latest Bank for International Settlements Quarterly Review (always a must read, but only if you're, like me, a total geek), released yesterday, and can't help but quote from the opening few paragraphs, as they so echo what you've been reading herein the past months:

Morning Note: Untutored Traders Are Not To Be Chastened, Well... Not Just Yet...

Better than expected data out of China inspired a rally in Asia that saw all but 3 of the 16 markets we track closing higher overnight. Europe, riding a sentiment survey that bested all economists' expectations, is following suit so far this morning; 15 of the 19 bourses we follow in the green. And not to be left out this morning are the U.S. equity markets: Dow up 133 points (0.48%), S&P 500 up 0.87%, Nasdaq up 1.51%, Russell 2000 up 0.47%.

Monday, September 14, 2020

Morning Note: A "Fascinating", And Telling, Development, and more....

Optimistic vaccine headlines and a bit of merger mania saw Asian equities rally overnight (12 of the 16 markets we track closed in the green) and has Europe, on balance, in rally mode as well this morning (12 of the 19 bourses we track up on the session thus far). U.S. equities are bouncing back from two weeks of decline rather nicely: Dow up 319 points (1.30%), S&P 500 up 1.52%, Nasdaq up 2.06%, Russell 2000 up 1.27%.

Friday, September 11, 2020

Macro Update: Blushing Socialists -- And -- The Dollar Bears Close Watching!

Macro conditions, as indicated by this week's scoring of our PWA Macro Index, continue, after last week's hiccup, to show net improvement. Although, not nearly to the point that would have us comfortably allocating assets in a manner reflecting strong odds that the next sustainable expansion is underway.

Morning Note: Tough Times Yield Good Things, If.....

Asian equities traded mostly higher overnight, with 12 of the 16 markets we track closing in the green. Europe's limping a bit into the U.S. session this morning, with 9 of the 19 bourses we track trading lower. U.S. stocks are (save for small caps) once again catching an early bid: Dow up 190 points (0.69%), S&P 500 up 0.51%, Nasdaq up 0.16%, Russell 2000 down -0.45%.

The VIX (SP500 implied volatility) is down -7.67%. VXN (Nasdaq vol) is down -4.38%. Now, don't be fooled by those steep declines in the pricing of volatility, 27.48 and 36.35 respectively are very precarious levels for stocks broadly.

Thursday, September 10, 2020

Chart of the Day

Well, that dollar/stock market nastiness I keep harping on is playing itself out in today's session as well:

This Week's Message: Bad News Be Good News

It's just a few minutes before the open on this smokey (I live in California) Thursday morning, and despite weekly jobless claims coming in higher than expected, and the U.S. dollar taking a sound beating this morning, U.S. equity futures just turned from notably red to nicely green. Hmm...

Wednesday, September 9, 2020

Quick note on today's action...

Was thinking about jumping on the blog and offering a quick market update, given this morning's strong rally. Nick just made the task easy.

Morning Note: Natural Rhythms

Asian equities followed the U.S. into the red in the overnight session; 14 of the 16 markets we track closed lower. Europe, on the other hand, is rebounding sharply this morning; 17 of 19 bourses are trading notably green thus far. U.S. markets are, as I type, attempting to break a 3-day string of sharp losses with an impressive rally: Dow up 453 points (1.65%), S&P 500 up 1.86%, Nasdaq up 2.25%, Russell 2000 up 0.34%.

Tuesday, September 8, 2020

Morning Note: The Question of the Day