''As events evolved, we recognized that, despite our suspicions, it was very difficult to definitively identify a bubble until after the fact -- that is, when its bursting confirmed its existence.''Well, frankly, that’s a notion I wholeheartedly reject.

In fact, fast forward 16 years, and, ironically, Mr. Greenspan himself agrees that bubbles can indeed be foreseen.

Easily, in fact, based on his conviction in 2018 that bubbles had formed in both the stock and the bond markets:

“"There are two bubbles: We have a stock market bubble, and we have a bond market bubble," the former Federal Reserve chairman told Bloomberg TV.Yes, as regular readers know all too well, I agree with Mr. Greenspan (the 2018 version, that is) that bubbles can be foreseen (the timing of their bursting is of course another matter), and that the bond (debt) bubble is presently “the critical issue.”

The trouble in the bond market "will eventually be the critical issue," Greenspan said, adding that "for the short term it's not too bad."”

Although, we didn’t begin adjusting portfolios to that reality until our macro index turned red late-summer 2019. At that point odds favored recession over expansion going forward, and our view was that the next recession would pierce the debt bubble and bring on a worse-than-2008 experience.

Here’s yours truly on Halloween Day 2019 in This Week's Message: Absolutely, There is A Bubble:

“...all of that stimulus coming out of the bursting of the mortgage bubble was so effective at inflating asset prices (just like it was coming out of the dotcom bubble), while wedding them (asset prices) to interest rates, that the Fed has boxed itself into the proverbial corner.Hence, here we are, living a surreality that could only occur at the end of a debt supercycle, amid epic asset price bubbles, and while panicky policymakers who -- in their willful abandonment of capitalism -- are desperate to keep asset markets and failed companies afloat.

And, worse yet -- and this is the fundamental problem -- it created yet another debt bomb that probably can't be diffused; meaning, it more than likely has to detonate, intentionally or otherwise, before we can even begin to get back to something remotely resembling normalcy in the debt markets.

And of course the Fed fears, legitimately!, that that detonation will surely come at the hands of (or be blamed on) voting members who don't pull every possible lever to delay it till the proverbial cows come home. But what will those proverbial cows be able to do??”

I.e., policymakers have zero interest in seeing debt markets back “to something remotely resembling normalcy.” Or, let’s say, in allowing the necessary painful process to unfold...

We are sorely missing Milton Friedman these days! emphasis mine...

"The economic miracle that has been the United States was not produced by socialized enterprises, by government-union-industry cartels or by centralized economic planning. It was produced by private enterprises in a profit-and-loss system. And losses were at least as important in weeding out failures as profits in fostering successes. Let government succor failures, and we shall be headed for stagnation and decline.”As I ponder the possibility that -- now that the Fed has utterly breached the dictate of the Federal Reserve Act and is, via a work around with the treasury, intervening into the securities (other than treasuries and govt-backed mortgages) market -- perhaps this time may indeed be different (i.e., no 50+% hit to the stock market, and no true debt market clearing), it’s clear to me that, in that scenario, “stagnation and decline” become serious risks over the long-term…

We’d in many ways be adopting the Japanese model, which emerged in response to the bursting of Japan’s own 1980s debt-fueled asset bubble.

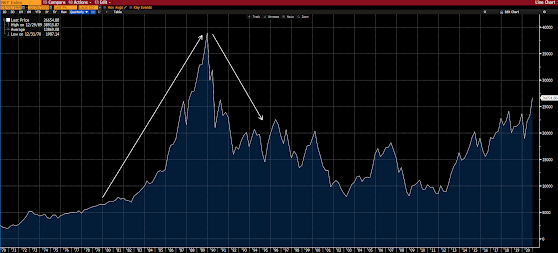

Here’s it is reflected in the Japanese equity market (1970 to current):

To get a feel for how Japan dealt with the fallout, here’s from a February 2003 IMF paper titled Japan’s Lost Decade:

“On the corporate side, rates of return remain low, not least because of the slow progress in reducing the still significant excesses of capital, debt, and employment from the bubble years. Concerns about the impact of restructuring on unemployment may constrain the speed of adjustment…”In other words, intense pain-aversion inspired Japan’s policymakers to do whatever it took (bailouts, credit creation, huge fiscal deficit, etc.) to essentially keep their debt market from clearing (excesses from being purged). Note that the above-referenced paper was written 13 years after the bubble began to burst!

And, yes, that can-kicking indeed managed to keep a 1930’s-style depression at bay.

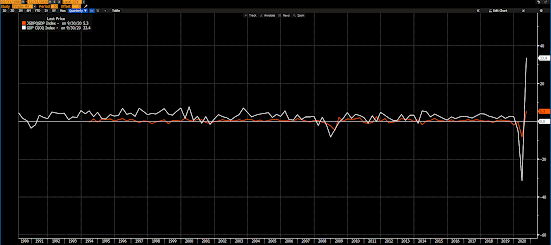

Japan’s unemployment rate (orange) vs the U.S.’s (white) from 1990 to present:

Successfully averting depression notwithstanding, Japan’s policymakers -- having no stomach for the pain that would result from failed enterprises meeting their market fates -- have left their economy constrained by "zombie" companies.

Short and sweet, from a 2017 Bloomberg article on productivity issues in Japan’s manufacturing space:

"“Some Japanese companies keep unprofitable businesses alive to maintain employment,” says Yasuhiro Kiuchi, senior researcher at the Japan Productivity Center in Tokyo."

Unprofitable businesses that require constant capital infusions to stay afloat (zombies) are drags on an economy, as they consume resources that could've otherwise been used in productive endeavors.

You'll recall how Japan was once the word's innovation leader, well, Bloomberg's Innovation Index now has them in 12th place.As for the U.S., not so good, we're 9th. We were #1 in 2013. Hmm....

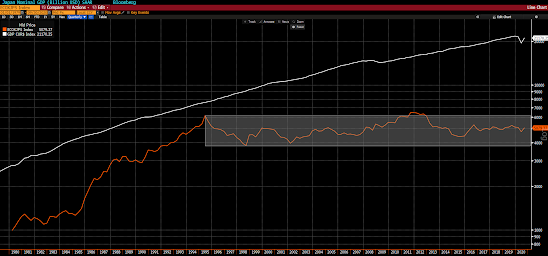

Note how Japan’s GDP growth rate (orange) has essentially hugged the zero line all these years (until recently [although that’s bouncing off of the Covid low]): (U.S. GDP in white)

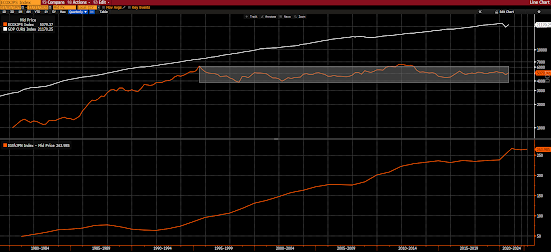

Here’s a look at Japan’s GDP (orange) in nominal terms. Note the utter stagnation these past 25 years. (US nominal GDP in white):

And note the incredible rise in Japan’s government debt (bottom panel) -- now 264% of GDP -- while the economy has done essentially nothing:

I.e., Pain-aversion (and, thus, stagnation) comes with a very high price tag!

Yes, Professor Friedman was spot on:

“Let government succor failures, and we shall be headed for stagnation...”There’s much more we could dissect with regard to Japan’s post-80s economy -- ~zero interest rates in perpetuity, central bank balance sheet, lousy demographics, waning productivity, etc. -- but suffice to say that virtually all of it, even to some degree lousy demographics (read immigration policies, and the correlation between wage growth/standard of living and population growth), results from government’s unwillingness to allow markets to clean up the messes government creates.

And, lastly, before we tackle today’s debt bubble, while the above may sound dire, understanding what policymakers will have to bring to bear in their attempts to avert a worse-than-2008 financial market scenario brings clarity (read opportunity) to the portfolio management process…

As a picture can speak a thousand words -- and since we’ve been relentlessly pounding on this topic for well over the past year -- I’ll be succinct with the rest, and enlist the aid of a few charts to once again make our point.

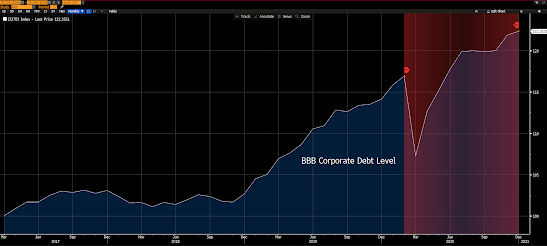

Here’s that BBB-rated (one notch above junk) U.S. corporate debt chart that I featured multiple times late last year, updated:

Remarkable!

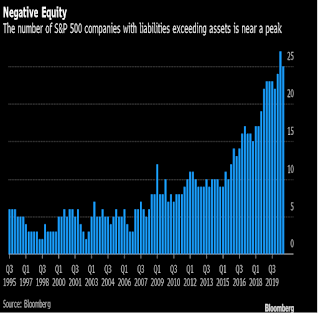

And how about U.S. companies (within the S&P 500) with literally upside down balance sheets:

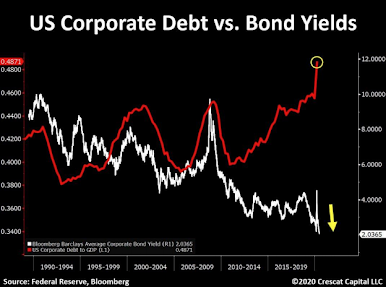

And to really drive home the surrealness of the day, note the head-scratching divergence between the growth in corporate debt and its cost:

Like I said above:

“...a surreality that could only occur at the end of a debt supercycle, amid epic asset price bubbles, and while panicky policymakers who -- in the willful abandonment of capitalism -- are desperate to keep asset markets and failed companies afloat.”So, cutting to the chase, here’s from our October 9 blog post:

“...I would not have expected -- because it was illegal at the time (well, technically still is) -- that the Fed would be able to buy corporate bonds, junk-rated ones no less, and, thus, leave people with legitimate reason to believe that there's absolutely no place they ultimately won't go to keep markets from clearing (Federal Reserve Act constraints be damned!) -- which given the debt mess we came into this recession with (before I could even spell coronavirus) would ultimately be destined to exacerbate the worst recession since the Great Depression.

Well, we indeed have the latter, but, thus far, we haven't remotely experienced the clearing necessary to allow markets to emerge in any semblance of decent shape.

So why might I have previously proclaimed that the next recession would be the worst since the Great Depression? Well, among other things, charts like the following two:

My black arrows point to how after the past several recessions (grey shaded areas) total corporate debt cleared only to a point that left more on the books than the bottom of the one prior. My red arrows point to how interest rates peaked at a lower spot than they did at the peak of each prior expansion. My red circles point to how interest rates rested at zero when debt peaked during the 2008 worst recession since the Great Depression, which is where they essentially sit currently, while debt, alas, ramps ever higher:

And here's the proverbial icing on the cake.

My red circles are where debt peaked during the Great Depression and where interest rates were at the time; where it peaked in 2008 and where interest rates were at the time; and, alas, where interest rates currently sit -- the level where debt will peak this time is yet to be determined:

”

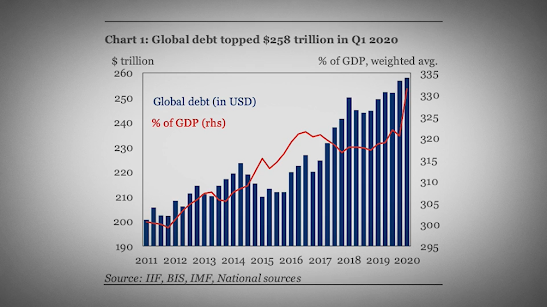

Of course this is not just a U.S. phenomenon.

Bottom line folks, great financial crises tend to come at the end of great private-sector debt cycles. A history that the powers-that-be are all too aware of. Hence their willingness to risk (accept/strive for) long-term stagnation to avoid the short(er)-term painful consequences of, frankly, conditions of their own making.

Whether or not they’ll “succeed” of course remains to be seen. Which is a risk we absolutely must hedge against as we otherwise work to exploit the opportunities inherent in an environment where policymakers will remain hellbent on, among other things, keeping interest rates, as well as the dollar, pinned to the floor…

In parts four and five we’ll explore some of those opportunities, as well as the risks, presented by today’s equity, commodity and currency markets' setups...

No comments:

Post a Comment