Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once again, the next cycle will be rich with macro investment opportunities, once we're through whatever's left in the current one.

Now that we've sufficiently (and some) expressed our view that there's more left to play out in the present cycle, we'll finish up this year's year-end message with a look at the next cycle's investment prospects.

"...if we apply some insight regarding cycles, we can increase our bets and place them on more aggressive investments when the odds are in our favor, and we can take money off the table and increase our defensiveness when the odds are against us." --Marks, Howard

What I'll call my broken-record line of the past several months has been:

"While you and I may or may not appreciate the world we'll be living in during the next cycle, it'll be rich with macro investment opportunities, once we're through whatever's left in the current cycle."

So let's break that down:

My implication that there's more to play out before we can declare coast is clear to allocate for the early-cycle phase of what's to come stems from, frankly, 39 years of intimacy with the economy and with global markets.

"The reports of my death are greatly exaggerated."

--The US Dollar

Among the factors that influence the asset mix of a thoughtfully designed global macro portfolio, the manager’s long-term dollar thesis is key.

As for our long-term (the next cycle) macro view, we -- despite our opening quote -- anticipate a weaker trending dollar... Which, as you'll see in Part 5, can make for a global investment setup rich in opportunity.

So why the weak-dollarview?

Well, and make no mistake, it's definitely not because the dollar is in any near-term risk of losing its reserve currency dominance.

Numera Analytics just published their year-end macro strategist commentary... If you've been keeping up with our year-end message to this point -- Part 2 and the recent video update, where we delved into yield curve dynamics, in particular -- the following from the aforementioned commentary will ring very familiar.

I.e., while we're not consensus right here (which, frankly, only emboldens our conviction), per the below, we're not the only ones seeing what we see:

Dear Clients, here's another one to be sure to take in...

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Attention clients, this is an important one to take in, start to finish 😎.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

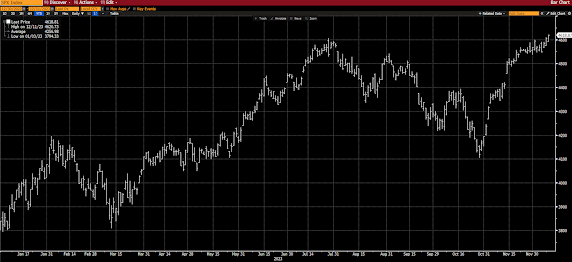

In last year's year-end message we expressed the following go-forward view of equity market conditions:

"As for our present view of conditions, while we don't believe we're out of the icy water just yet -- and, for the moment, we anticipate that'll it'll get even colder before things begin to warm up -- we indeed see bluer skies on the not-too-distant horizon... Although, as you'll read in the remainder of this year-end message, we think the skating will be far better on ponds the vast majority of investors neglected during the previous bull run."

Here's the S&P 500 year-to-date:

While that February/March cold snap was indeed threatening, as we stated in Part 2, the Fed's $400 billion regional bank rescue served to heat things right back up... Then, from May to July, the AI-driven "Magnificent 7" phenomenon (just a handful of stocks doing all the heavy lifting) boosted the headline index virtually straight up to the end of July.

And what about that Q3 double-digit drawdown, was that the cold snap we were looking for? Nope, our concern lies in the fact that the market seems utterly unconcerned with the prospects for recession on the horizon, which, in that event, exposes itself to consequential downside risk... I.e., that cold snap, should it come, will be in response to the reality that the earnings estimates currently baked into stock prices simply cannot hold up amid an economic contraction.

In this year's Part 2 we're updating the data and our narrative (recession risk remains elevated) on the state of the economy, using a format similar to last year's Part 2.

Yes, our recession light was lit last December, and it remains lit a full year later... And, while I state, ad nauseum, in the videos that our model is not a timing indicator, but rather a risk measure, we nevertheless need to get our heads around what's held the economy up amid such dire signals from too much of the data.

Now, before we go there, I should mention that what is widely viewed as the most reliable of all recession signals -- when the 2s/10s treasury yield curve goes inverted -- comes (historically) with a lag of 7 months to 2 years between initial inversion and the onset of recession .

I should also mention that in October 2022, Bloomberg Economics literally assigned a 100% probability that we'd be in recession within the ensuing 12 months... Well, that didn't happen.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

As you (clients) know, I enjoy using analogies to explain our view of market and economic general conditions... In the past I've associated our macro analysis with the flight path of an eagle affixed with electrodes, etc., that allow us to monitor its vital functions as it glides across blue skies, sores to high altitudes, and flaps its way through the storms that occasionally cross its path.

Fishing, basketball and ice skating have also inspired some storytelling that has helped me drive home how we approach the task of preserving, protecting and growing our clients' wealth in a manner that has them satisfying their objectives while, ideally, feeling comfortable amid the inevitable ups and downs delivered by world markets.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

The following quote (and video), along with our own models, speaks to our stubbornness around remaining hedged right here:

"Stock investors should hope for the best but prepare for the worst when it comes to gauging the outlook of the US economy. Soft-landing optimists have a case to make, yet the historical evidence is overwhelmingly bearish when it comes to the end of previous Fed hiking cycles. Equities face steep losses if the economy sees a “softish” or hard landing.

In the 11 times when the Fed has tightened monetary policy to combat inflation since 1965, stocks escaped largely unscathed only about three times. The other occurrences saw average peak-to-trough losses of nearly 30% in the years after interest rates peaked."

-- Tatiana Darie (Bloomberg)

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

FYI, for the next few weeks (to year end), I'll be a bit less active, and less voluminous, here on the blog, as I'll be devoting the time normally spent organizing, then articulating, my thoughts for the daily message to what, as usual, will be a several part year-end message (delivered over the final two weeks of the year)..

So, for this morning, just the following graph (H/T BCA Research), followed by my brief assessment, and some critical investment wisdom from the late great Charlie Munger:

Bloomberg's Cameron Crise this morning speaks to what has stocks green at the open:

"When you are a bull, everything looks like a red cape, which kind of explains how the market is likely to interpret this morning’s data. The salient features were a downward revision to the Q3 core inflation index, a downward revision to last quarter’s household spending, and downside surprises to October inventory data (which should produce a downgrade to current-quarter growth estimates.) That all casts a dovish hue on the policy backdrop..."

All of which denotes a slowing economy, which of course is to be expected if the 2024 recession narrative is to play out... In the meantime, as is typical at this stage, confirmation of such, is, ironically, bullish for stocks.

I can’t emphasize enough how markets, (monetary) policymakers and politicians are so stuck between the proverbial rock and a hard place... Folks are asking if next year’s election gives us any pause in our economic assessment (recession odds elevated), for, as we know, all conceivable strings are pulled by incumbents to bolster the economy as election times near.

Yes, we've touched on this plenty of late, but, again, per our weekly results update below, the divergence among equity sectors this year has been utterly shocking... And while indeed a serious broadening (the 8 of 11 sectors that are, let's say, not having a magnificent year playing catch up) may be in the offing, history offers up some serious red flags to consider.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Comments made by Hedgeye CEO Keith McCullough in today's Macro Show resonated with me, and has me calling up the following from my video commentary this morning:

"Let's see this for what it is; this is not a time, from these levels and from this stage in the cycle, to expect that the next new raging bull market is about to begin...

Toward the end where I mention jobless claims, I suggested that a weak number would be bullish for stocks (given the present character of the trading), I actually meant that a strong number (denoting a weak labor market) would be bullish... Now, go figure, the number was weaker than expected (denoting a strong labor market) and equity futures didn’t budge... Although, I should add that last week’s number was revised up (weak sign), and Nvidia didn’t whiff yesterday... Hmm...

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

As we gear up to produce our deep diving, and typically lengthy, year-end message, we think it appropriate, given present market dynamics, this year to focus a good bit on risk.

While organizing my thoughts and perusing my library of related content/literature, I came across a quote that our current assessment of the near-term risk/reward setup inspires me to share right here.

And I must say, having lived intimately with, and managed through, the tech bubble -- while unpopularly (among some clients) reducing our tech exposure (in 1999) during the final massive runup -- I deeply sympathize with the following, from Howard Marks' exceptional book "The Most Important Thing:"

This, from Howard Marks, captures the messaging herein of late:

"...you’re unlikely to succeed for long if you haven’t dealt explicitly with risk. The first step consists of understanding it. The second step is recognizing when it’s high. The critical final step is controlling it."

Peter Boockvar and I have seen a few rodeos in our day... Listening to an interview with him recorded yesterday; I couldn't agree more with the following:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

In this morning's video (recorded yesterday) I mention Walmart's outlook on the consumer... To really pound home their expectations; this from the CEO:

"We may be managing through a period of deflation in the months to come."

I can not stress enough what such a scenario would do to corporate earnings, particularly this go-round.

Premium research provider Numera Analytics, like us, sees late cycle dynamics at play, and is, thus, cautious on equities right here... They, also, per their just-released Global Asset Allocation Report, nevertheless see opportunity in certain emerging markets:

Amidst our constant reminders that the present equity market setup remains somewhat precarious, we also continue to hint that our go-forward thesis sees unique global opportunities ahead -- beyond, that is, what's left in the current cycle.

Crescat's Tavi Costa points to one that we agree makes great sense going forward:

Yes, resource-rich economies, both from a valuation standpoint and given our view on the dollar during the next cycle, are one of those opportunities... Whether or not now's the time to take on full positions, well, that remains to be seen.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

This morning's CPI report comports perfectly with our current and go-forward theses... Current being the market reaction (up) to a weaker than expected print, the go-forward being that weaker inflation is 100% consistent with a weakening economy... The market reaction also, as I've been pointing out in the video commentaries, comports on balance with the short-term technical setup for equities, yields and the dollar.

Not much to add this morning to Friday and Saturday's video commentaries... CPI tomorrow, retail sales Wednesday, earnings announcements, Fed speakers, and, alas, the government shutdown circus I suspect will give us plenty to comment on over the next few days.

Here's your weekly sector, region and asset class results update (and a quote to ponder):

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Diane Swonk is a very good, thoughtful, objective economist... This morning's message is all her:

"One lesson I learned early in my career was that consumers will resist, with everything in their power, reductions in their standard of living. Later I learned that it was not just the amount people accumulated that mattered, but the pace at which they accumulated stuff that became so entrenched. A version of keeping up with the Joneses played out en masse.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Like I keep saying, last week’s rally in stocks comports perfectly with our present thesis… The economy will likely enter recession next year, and as the data turn down, equity markets initially turn up as traders and investors have grown to believe that stocks always rise when the Fed cuts interest rates.

Here are the highlights from Bloomberg's Tatiana Darie's warning about the signal in Caterpillar's latest numbers (which [Cat's global sales growth], btw, happens to be one of the 47 inputs to our PWA Index).

Emphasis mine:

Caterpillar Is Sending a Warning About the Economy: Macro View (Bloomberg) -- Caterpillar earnings spooked investors, who saw a drop in its order backlog as an ominous sign for the global economy. At least for the US, its largest market, that holds some truth, which means it’s also a warning for the stock market.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

We published this month's equity market conditions report (the intro to our internal analysis) in a separate post, as Monday's will be long enough with our weekly sector, region and asset class results update:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

In yesterday's chart of the day, I illustrated the point that, at this juncture, weak economic news is strong stock market news... I think I've expounded sufficiently as to why in our latest commentaries... The other thing the equity market has going for it is resoundingly sour sentiment, all of a sudden.

The setup is pretty similar to what we sniffed out at the beginning of October.

As clients and regular readers have no doubt noted, while the next leg of the current bear market (should there be one) will be characterized by declining corporate earnings amid notably weakening economic conditions, in our view the latter, in its early stages, will, ironically, very likely inspire a potentially not-small rally in stocks.

In today's chart of the S&P 500 below, I green X'd the moment the ISM Manufacturing Survey for October was released, and two spots during Fed Chair Powell's press conference:

As for the ISM survey, expectations had it coming in at 49, which just barely denotes contraction... The actual reading, however, was a surprisingly low 46.7, sending it (the manufacturing sector) deeper into recession territory...

And, lo and behold, stocks immediately popped higher on the release -- validating our latest messaging herein.

As for that volatility around Powell's presser, when he came out of the gate with some tough talk on remaining vigilant, stocks bolted lower -- the market is desperate for the Fed to lighten up (not considering the conditions [and the earnings setup] that will actually make that happen) -- he then proceeded to celebrate the progress they've made thus far 😕, and to essentially not say anything to further upset the market applecart right here.

As I've pointed out in the last 3 video updates, the technicals were also pointing to pretty strong odds of a rally right here.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Our last 2 video commentaries pretty well cover our view of the short and long-term scheme of things... I.e., according to the technicals, odds favor a near-term rally in equities, according to the fundamentals, continued caution is very warranted.

In case you missed them:

Technicals Point To A Near-Term Rally, But, Ultimately.....

The Consumer, Market Signals, Earnings Call Insights and Yes, We're "Late in the Game"

And here's your weekly sector, region and asset class results update:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

While Q3 GDP came in better than expectations, its underlying inflation gauge came in softer than expected... Combine the latter with higher than anticipated weekly unemployment claims (particularly continuing claims, as I highlighted in last Friday's economic update), and a clearly dovish ECB monetary policy statement, and you get a knee jerk market reaction which entirely comports with our short-term view (bad economic news = short-term good news for stocks).

Here's SP500 futures action so far this morning -- it's presently10 minutes before the open (the green arrow points to the moment the GDP and jobless claims numbers were released):

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Long-term treasuries rallied yesterday, seemingly sparked by Bill Ackman’s assertion that the world is simply too risky to be short bonds right here… While, per below, his comments did inspire some buying, I have to believe that, at these levels, investors are poised to pounce on treasuries on any sign of economic weakness going forward… And that’s despite the high level of issuance to come.

Ackman tweeted his comments at 6:45am.

Here's TLT (long-term treasuries) yesterday, I circled 6:45am:

If you've been tracking our weekly results updates you've noticed, of late, a growing shade of red... As we've maintained since the October '22 bottom, macro dynamics have remained such that a next leg down carries odds too high to ignore.

Now, many on Wall Street have taken the stance that the bear market is over and done, and that a new bull market is just getting underway.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Just a quick note this morning; anything more from me today would be simply redundant.. I.e., not much more to report beyond our latest written and video messaging... Not much, that is, other than yesterday's 20-year treasury bond auction, which came as quite the surprise to the market, and, given the messes that were last week's auctions (mentioned in Friday's important video update), to yours truly as well.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Two points I'd like to make in the opening to this morning's message:

1. I am indeed in the camp that believes AI is a real long-term game-changer.

2. Like I said yesterday, "... today's CEO has been reduced to little more than shepherd of his/her company's stock price (quoting Julian Brigden)"

Now, with regard to my view of AI, the operative words there are "long-term." In the short-term, however, per last Monday's Wall Street Journal, there are issues that those Q2 earnings calls conveniently failed to mention (or at least emphasize).

So, Q4 of the year is known for its friendliness toward the stock market... And, from a sentiment and Fed-speak standpoint, one could argue that -- geopolitical turmoil aside -- the 2023 Q4 setup isn't all that bad... I certainly don't think that Q3 earnings results, by themselves, will pose a challenge to the near-term bullish narrative.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

So, headline CPI came in a titch hotter than expected, while core (ex-food and energy) came in bang on expectations... Stocks flinched a bit in the premarket, then settled slightly higher ahead of the open... Bonds took a bit of a hit (yields up), but, all in all, while, say, 2 weeks ago this report might've rattled markets (although the day is very young as I type, so, you never know), Fedheads seem to have, for the moment, calmed market waters with their unanimous hints that they're pretty much done hiking rates... In fact, two more overnight (just ahead of fresh CPI data no less), echoed that chorus.

We'll tackle CPI and the rest of the week's data in tomorrow's economic update.

In the meantime, here are a few key highlights from our latest messaging herein:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

On our strategy call yesterday morning, while I traveled between offices, we noticed the abrupt intraday turnaround (akin to last Friday's) in the equity market... My comment, without looking, was that it virtually had to be someone at the Fed saying something soft about go-forward monetary policy.

Sure enough, the typically-hawkish (higher rates advocate) Fed Vice Chair Phillip Jefferson essentially turned the tide with:

Goes without saying, there’s much to unfold in the days ahead related to tragic weekend events… The uncertainty will reflect across asset classes, oil and “safe havens” in particular.

Stay tuned.

Here’s your weekly sector, region and asset class results update:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

As you'll gather from this morning's video commentary (recorded last evening), yours truly was anticipating a "soft" jobs number this morning, and, as bad news is, for the moment, good news, a rallying stock market to go with it.

Well, scratch that! The number came in literally double the consensus estimate, and an astounding 100k above the most aggressive upside prediction... And, to top it off, the prior 2 months were revised up by 119k.

Now, that said, there was some softness that, when "the market" digests it, just might mitigate a bit of the premarket selloff we're seeing across equities and bonds... That softness came in what matters most in terms of inflation, average hourly earnings... They were up 0.2% month-on-month; consensus estimate had it at 0.3%.

Interestingly, gold is up .16% (silver's up 1.4%) premarket, despite a notable jump in real yields -- perhaps precious metals traders are already sniffing out that "softness" (although the morning's very young).

Anyways, here's your end of week market analysis... In this one I take you way beyond the latest action... We'll tour the past few market cycles, what worked, what didn't, and I scratch the surface on how one money manger (us) is presently addressing near-term dynamics, and what we're anticipating beyond the present cycle.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Yes, "hiring slowdown" is consistent with economic slowdown, and, yes, "the market" is obsessively focused on the Fed, as if the thing that ultimately matters most, corporate profits, does not in fact matter.

In our view, another rate hike is highly unlikely, as it is highly unnecessary, given that leading indicators are signaling uncomfortable odds of recession (and, thus, falling inflation) in the months to come.

Among our recent video commentaries, this one from September 15th is a must-watch (at least from the 4:00 to 14:20 mark) for those interested in a historical perspective on why -- despite what current trading action might otherwise portend -- an inflation-slaying economic slowdown will be problematic for stocks, even while the Fed is cutting rates in response:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Peruse the numbers in your weekly results update below and you'll notice, among equities, that 5 of the 11 major US sectors remain notably in the red year-to-date, while three of the positive 6 have delivered low single-digit returns... I.e., as we continue to stress, all of the heavy lifting has occurred in 3 sectors that essentially capture the half-dozen or so biggest positions in the S&P 500 and Nasdaq 100 Indexes, that, per Jim Bianco, pretty much tell the whole story:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Here are a few key highlights from our recent messaging herein:

This Tuesday:

"...another way to view the present setup would be to recognize that -- while stocks look [to perhaps put it mildly] expensive -- bonds are beginning to look pretty (historically-speaking) cheap. Hence, my comment that, while it may still be a bit early, we'll definitely be eyeballing duration going forward."

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

In last week's video update I suggested that we're keeping a very close eye on "duration," implying that assets that respond most-positively to falling rates have our attention, althoughwe’renot yet adding to any, right here...

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Call it, per Bloomberg's Michael McKee, "a unanimous hawkish pause." Yep, no rate hike at yesterday's Fed meeting, but threats of one by year-end, and projections that show monetary policy staying yet tighter for longer than they thought last time they told us what they thought.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Among a plethora (11) of central bank meetings this week, the US’s of course will be the one most likely to move markets (although Japan's [commentary] indeed could)… With 100% certainty I’ll say that there’ll be no rate hike come Wednesday... Not because the Fed wouldn’t be justified, in fact, if Powell were indeed true to his rhetoric, there’d be one – as the latest inflation-related data conflicts with the recent disinflationary trend – it’s just that the market is discounting virtually zero odds of one.

For this morning's message we'll start by reposting Friday and Saturday's video commentaries... Both of these are we think very timely and should be viewed by anyone who’s at all interested in the current risk/reward setup for markets, and in what the latest consumer data say about the present stage of the economic cycle:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Here's the opening to a post I penned back on April 20, 2020:

"Keynes suggested circa a century ago that trading (as opposed to, I'll say, investing in) markets is not about assessing fundamentals, it's about what traders think other traders are going to do. And for the more savvy traders, it's about what they think other traders think other traders are going to do."

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

The signs for the global economy sent out by the "first mover" among the economic indicators - the sentix economic index - point to a further downturn and a strengthening of the economic downturn forces. The situation in Germany remains particularly precarious. Here we are measuring the weakest situation values since July 2020, when the economy was slowed by the first Corona lockdown. Germany is also weighing heavily on the economy in the euro zone as a whole. The recession is progressing.

But even for the USA, which has so far held up well and defied the restrictive FED policy, the economic data are falling markedly. The tipping point of a global recession is less distant than one might think.

Clients, if you haven't taken in Friday's video commentary yet, please do... I think it does a nice job describing a few of the drivers of our present assessment and overall allocation... I'll include the player at the very bottom of this note.

The following from thewidely followed/highly respected Sentix September Economic Report comports with our current view of overall general conditions:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Today’s action in US equities screams to the still-prevailing “soft-landing” market mood… I.e., bad news is viewed as good news, because, presumably, any weakness will not land us in recession, and (or perhaps because) it’ll inspire the Fed to ease policy.

So, when this morning’s ISM Services Survey came in better than expected, stocks immediately sold off (red circle below):

As we've been pointing out during client portfolio review meetings of late, beyond whatever's left in the current cycle (our view is that odds lean toward another round of turbulence along the way), we see a number of what we believe to be very exploitable themes.

Here's the intro to our latest Equity Market Conditions internal report, along with our detailed technical assessment of the dollar:

8/31/2023 PWA EQUITY MARKET CONDITIONS INDEX (EMCI): -66.67 (-25.00 from 7/31/2023)

SP500 past 30 days, -1.77%:

SP500 Equal Weight Index past 30 days, -3.37%:

While stocks staged an impressive move over the final few days of August, the SP500 was unable to squeeze out positive results for the month… Breadth deteriorated notably, as evidenced by significantly worse results for the SP500 Equal Weight Index, as well as by the other metrics scored herein.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.