In the tech bubble, buyers didn’t worry about whether a stock was priced too high because they were sure someone else would be willing to pay them more for it. Unfortunately, the greater fool theory works only until it doesn’t. Valuation eventually comes into play, and those who are holding the bag when it does have to face the music.

• The positives behind stocks can be genuine and still produce losses if you overpay for them.

• Those positives—and the massive profits that seemingly everyone else is enjoying—can eventually cause those who have resisted participating to capitulate and buy.

• A “top” in a stock, group or market occurs when the last holdout who will become a buyer does so. The timing is often unrelated to fundamental developments.

• “Prices are too high” is far from synonymous with “the next move will be downward.” Things can be overpriced and stay that way for a long time … or become far more so.

• Eventually, though, valuation has to matter.

JOEL GREENBLATT: Read that final bullet again!

PAUL JOHNSON: These points are so very true, although challenging to master while engulfed in the endorphin rush of a mania or bubble. “BUBBLE.COM,” JANUARY 3, 2000

Now, to be clear, we are not predicting (in the months to come) the kind of market meltdown experienced when the tech bubble imploded, or during the 2008 "Great Financial Crisis." In fact we're making no prediction whatsoever... What we are doing -- from a very top-down macro, and fundamental, vantage point -- is assessing the present risk/reward setup, and, clearly, to us, this is not a time to go chasing headline equity benchmark returns.

Here are a few key highlights from our latest messaging herein:

This, from Howard Marks, captures the messaging herein of late:

"...you’re unlikely to succeed for long if you haven’t dealt explicitly with risk. The first step consists of understanding it. The second step is recognizing when it’s high. The critical final step is controlling it."

"...as I've witnessed, firsthand, veteran professionals, and investors, who actually lived through the likes of the late-90s convince themselves that eerily similar dynamics in the present day will not ultimately end in the same fashion... Apparently they've convinced themselves that human nature does indeed change (proving, I suppose, that it indeed doesn't), and that this time is different.

Now, you always hear me say that we have to remain open to all possibilities, and we do, but, my oh my!, we simply can't deny the fact that, at a minimum, history indeed instructs us as to when the risk is dangerously high, and, thus, in our case, inspires us to accommodate for it in our allocations."

"...resource-rich economies, both from a valuation standpoint and given our view on the dollar during the next cycle, are one of those opportunities... Whether or not now's the time to take on full positions, well, that remains to be seen.

With regard to Brazil, their aggressive early response to inflation, along with very cheap equity valuations, inspired to us to take a position in anticipation of outright policy easing earlier than the rest of the world... That position is presently up 20% year-to-date... Our other two individual foreign country exposures are Mexico and Vietnam, up 25.13% and 13.26% respectively, year to date... However those two are more about near-shoring of manufacturing (Mexico), and "friend-shoring" away from China (both Mexico and Vietnam).

Also, with resource-rich countries in mind, we very recently diversified our broad emerging markets exposure into an ETF (DEM) that captures a bit more of that theme than does our older core position, with a high dividend (6.05% past 12 months) objective along with it... DEM is up 4% during the brief time we've owned it.

Now, taking a step back from boasting about our returns on these particular positions, we hold no delusions that they're not subject to our present base case scenario, which is recession in 2024... Per Tuesday's note:

"If we indeed happen to escape the woods without recession, and inflation settles back in at the Fed's 2% target, all's good in the land of equities, and we'll introduce, and add to, positions/asset classes that our long-term thesis says will shine over the years to come... Presently, however, odds that we'll be able to capture them at more attractive (cheaper) levels over the coming months are simply too high to ignore."Hence, we've just carefully scaled in to this point."

"This morning's CPI report comports perfectly with our current and go-forward theses... Current being the market reaction (up) to a weaker than expected print, the go-forward being that weaker inflation is 100% consistent with a weakening economy... The market reaction also, as I've been pointing out in the video commentaries, comports on balance with the short-term technical setup for equities, yields and the dollar.

Now, the "problem," as we've been expressing ad nauseam (most recently last Friday), is that investors seem to forever, at this stage of the cycle, get sucked in by deteriorating data -- as they anticipate a friendly Fed response -- only to suffer the disappointment (if not devastation) that comes with the recession-induced last leg down of a bear market.

Now, make no mistake, I'm not speaking inevitability here, I'm simply speaking the go-forward risk/reward setup... Today's news, rather than taking us out of the woods, confirms that we are deeply within... If we indeed happen to escape the woods without recession, and inflation settles back in at the Fed's 2% target, all's good in the land of equities, and we introduce, and add to, positions/asset classes that our long-term thesis says will shine over the years to come... Presently, however, odds that we'll be able to capture them at more attractive (cheaper) levels over the coming months are simply too high to ignore."

"Like I keep saying, last week’s rally in stocks comports perfectly with our present thesis… The economy will likely enter recession next year, and as the data turn down, equity markets initially turn up as traders and investors have grown to believe that stocks always rise when the Fed cuts interest rates.

Of course history tells a different story, when, that is, recession is part of the mix… Stocks at 21 times earnings (P/E), and 2.4 times sales (P/S) -- like today -- are resoundingly expensive compared to where they historically trough during recession.

For P/E, that would be 14.5 in 1990, 15.2 in 2002, 9.7 in 2008, and 14.3 during covid.

For P/S, 0.7 in 1990, 1.2 in 2001, 0.7 in 2008 and 1.6 during covid.

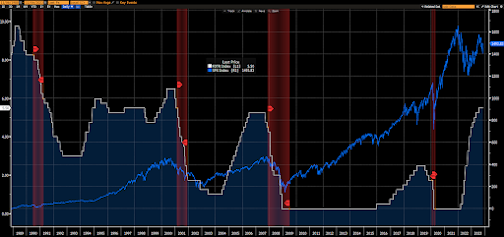

And, per the below, the Fed was cutting aggressively while stocks (blue line [SP500]) were selling off:

Again, it makes sense that, only for the time being, stocks rally on weak data… If/when indeed one of those red-shaded areas (recession) shows up, however, it’ll highly likely be a different story...

Frankly, that’s opportunity, if, that is, you’re properly hedged and diversified going in.Of course, conversely, should inflation heat back up, or simply stay sticky, stocks will likely struggle there as well... But that'll be far less actionable, as long as recession risk remains in the mix."

Asian stocks leaned slightly green overnight, with 9 of the 16 markets we track closing higher.

Europe's in the red so far this morning, with 13 of the 19 bourses we follow trading down as I type.

US equity averages are mostly lower to start the session: Dow by 95 points (0.27%), SP500 down 0.46, SP500 Equal Weight up 0.12%, Nasdaq 100 down 0.99%, Nasdaq Comp up 0.94%, Russell 2000 down 0.82%.

As for yesterday’s session, US equities closed higher: Dow by 0.6%, SP500 up 0.7%, SP500 Equal Weight up 0.4%, Nasdaq 100 up 1.2%, Nasdaq Comp up 1.1%, Russell 2000 up 0.5%.

This morning the VIX sits at 13.58.

Oil futures are down 0.46%, nat gas futures are up 0.49%, gold's up 1.37%, silver's up 1.92%, copper futures are down 0.18% and the ag complex (DBA) is down 0.11%.

The 10-year treasury is up (yield down) and the dollar is up 0.09%.

Among our 32 core positions (excluding options hedges, cash and money market funds), 13 -- led by SLV (silver), GLD (gold), REMX (rare earth miners), XLV (healthcare stocks) and AT&T -- are in the green so far this morning... The losers are being led lower by Dutch Bros, Range Resources, EWW (Mexico equities), XLE (energy stocks) and XLP (consumer staples stocks).

Have a great day!

Marty

No comments:

Post a Comment