Ackman tweeted his comments at 6:45am.

Here's TLT (long-term treasuries) yesterday, I circled 6:45am:

As for equities, I see decent odds of a near-term bounce that’ll recapture some of the hit stocks have taken since their late-July high… Some argue for upside from here based on favorable seasonality and perhaps anticipation of a strong retail season… That’s not my take.

My take is that, again, equities may indeed rally in the near-term, but that’s if/when further evidence emerges that the economy is weakening toward recession over the coming months… I.e., in that instance, stocks will likely get bought, as investors/traders seem to believe that it’s all about the Fed, and that weak data will have them thinking that the Fed will ease up measurably on monetary policy.

Conversely, should the economy actually show real strength into year-end, I’m thinking stocks may actually struggle, as such a scenario supports inflation and, therefore, supports the notion that, as Powell put it last Friday, monetary policy is not too tight right here.

The move in bonds on Ackman's tweet captured in the chart above would also be the sort of kneejerk reaction we can expect from a meaningfully weak data point...

As for equities, I see decent odds of a near-term bounce that’ll recapture some of the hit stocks have taken since their late-July high… Some argue for upside from here based on favorable seasonality and perhaps anticipation of a strong retail season… That’s not my take.

My take is that, again, equities may indeed rally in the near-term, but that’s if/when further evidence emerges that the economy is weakening toward recession over the coming months… I.e., in that instance, stocks will likely get bought, as investors/traders seem to believe that it’s all about the Fed, and that weak data will have them thinking that the Fed will ease up measurably on monetary policy.

Conversely, should the economy actually show real strength into year-end, I’m thinking stocks may actually struggle, as such a scenario supports inflation and, therefore, supports the notion that, as Powell put it last Friday, monetary policy is not too tight right here.

The move in bonds on Ackman's tweet captured in the chart above would also be the sort of kneejerk reaction we can expect from a meaningfully weak data point...

Let's layer on QQQ (the Nasdaq 100 Index ETF):

Yep, right on cue.

So, for the time being, bad news remains good news, and vice versa.

Beyond the time being, however, bad economic news will indeed turn out to be bad equity market news, as it will bring on what the last meaningful leg of any bear market is made of – declining corporate earnings.

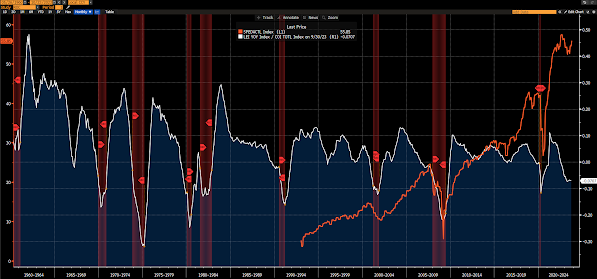

LEI/CEI (leading economic indicator/coincident economic indicator) ratio along with S&P 500 Earnings (orange), recessions in red:

Stay tuned...

Asian stocks leaned green overnight, with 9 of the16 markets we track closing lower.

Europe's mostly higher so far this morning, with 13 of the 19 bourses we follow trading up as I type.

US equity averages are higher to start the session: Dow by 275 points (0.83%), SP500 up 0.70%, SP500 Equal Weight up 0.77%, Nasdaq 100 up 0.74%, Nasdaq Comp up 0.67%, Russell 2000 up 1.11%.

As for yesterday’s session, US equity averages were mixed: Dow down 0.6%, SP500 down 0.2%, SP500 Equal Weight down 0.6%, Nasdaq 100 up 0.3%, Nasdaq Comp up 0.3%, Russell 2000 down 0.9%.

This morning the VIX sits at 19.65.

Oil futures are down 0.81%, nat gas futures are up 0.27%, gold's down 0.53%, silver's down 0.50%, copper futures are up 0.45% and the ag complex (DBA) is down 0.09%.

The 10-year treasury is down (yield up) and the dollar is up 0.45%.

Among our 32 core positions (excluding options hedges, cash and money market funds), 29 -- led by REMX (rare earth miners), AT&T, Dutch Bros, VNM (Vietnam Equities) and XLC (communication stocks) -- are in the green so far this morning... The 4 losers are SLV (silver), GLD (gold), DBA (ag futures) and XLE (energy stocks).

The secret is to get out of the “shadow”—to escape the slavish habits and delusive hopes of “what we call our future”—and to recognize deeper patterns at work.

Have a great day!

Marty

No comments:

Post a Comment