Stocks were rallying notably in the pre-market ahead of this morning's CPI number. But, as I suggested in yesterday's video (one to watch if you haven't yet), we did not expect a market-friendly read out of September's inflation numbers... The way certain components are measured, along with base effects, simply didn't offer much hope of a downside (upside for stocks) surprise.

Well, that's what's playing out in the premarket this morning... Which is a virtual replay of last month's action... Stocks rallying into the number (although news out of the UK was globally bullish this morning), then tanking on the disappointing CPI release.

Now, make no mistake, there's information in that market action... I.e., despite the sour sentiment, there's some serious nervousness around missing a market upside pop should the slightest catalyst emerge...

Fascinating, at least at the moment, that the volatility index (VIX) is actually trading lower as I type... In a panicky selloff, you'd expect the VIX to be soaring as options traders pile into downside bets... The opposite appears to be occurring (but only for the moment, mind you)...

As we've reported -- while we've maintained that there's yet more downside to plumb for the current bear market -- the technicals have been constructive, and fear remains high, which is the recipe for some violent bear market rallies... I suspect that's what has traders hesitating to load up on downside derivative bets (again, mind you, only for the moment).

On another note, per the second line in the snip below, Janet Yellen's getting concerned:

So, what's the worry? Well, a lack of liquidity essentially denotes a lack of interest, or a lack of buyers... In an illiquid market/security, should a disruption occur that incites a panic or rapid selloff, the price of said security can utterly plummet in value, and, in the case of bonds, send yields to the moon.

Case in point, the earthquake in gilts (UK government bonds) last week, that, had the Bank of England not intervened (bought like crazy), it appears as though margin-call-disaster would've hit the UK pension industry.

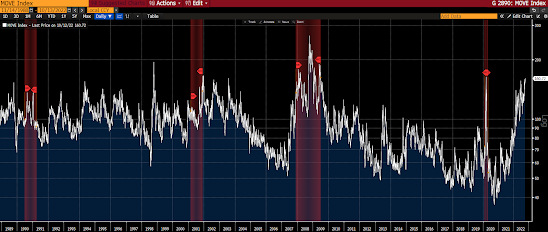

Two of the components within our own financial stress index are the Treasury Liquidity Index and the MOVE Index (tracks implied volatility on treasury options)... In both cases, a rising line ain't good.

Treasury Liquidity Index:

MOVE Index

Asian equities struggled yet again overnight, with 13 of the 16 markets we track closing lower.

Same for Europe so far this morning, with all but 2 of the bourses we follow trading down as I type.

US stocks are getting hammered to start the session: Dow down 518 points (1.80%), SP500 down 2.26%, SP500 Equal Weight down 2.37%, Nasdaq 100 down 2.96%, Nasdaq Comp down 3.04%, Russell 2000 down 2.79%.

The VIX had now turned, albeit slightly, at 33.68, up 0.33%.

Oil futures are down 0.29%, gold's down 1.66%, silver's down 2.38%, copper futures are down 0.93% and the ag complex (DBA) is down 0.75%.

The 10-year treasury is down (yield up) and the dollar is up 0.22%

Among our 35 core positions (excluding options hedges, cash and short-term bond ETF), 0 (save for put options) are in the green so far this morning. The losers are being led lower by Albemarle, MP Materials, AMD, base metals miners and cyber security stocks.

Not saying it's time to get greedy right here, but of course we're getting closer by the day:

"...be greedy when others are fearful"

--Warren Buffett

Agree! Today's volatility was to the extreme. I could definitely see that the Bulls were mad and fought back. A lot of them thought that today was the bottom and supported like you said at the 3500 level for S&P. You are absolutely right about the darkness dark and the black swan.

ReplyDeleteThank you so much for keeping us up-to-date with the daily market activities.

Yeah Sam, the 3,500 level found a lot of support... Keep in mind, as I've been presenting of late, there's huge flows working through this market having to do with options dealers who have to hedge their own positions... Clearly, many of them were short futures contracts and were forced to cover as the market bounced, exacerbating the huge turnaround... Also, as I've been pointing out, our fear gauge has been flashing a very high reading, and, overall, futures traders have remained net short the equity market... Today was largely about sentiment shifting (fear of missing out) and massive short-covering... plus, per our charting on the videos, a relatively constructive technical setup going in... And, lastly, seasonality right here favors the bulls... This rally could have legs, but of course time will tell... Today's presumed U-turn with regard to fiscal policies proposed by the UK's new leadership, was huge for global markets... At this point, however, nothing's been carved in stone there... anything that suggests those assertions aren't what they seem come next week will be met with more volatility... Given the danger to the pound, gilts and the UK pension system, the market is likely correct in assuming that today's news was legit...

DeleteQuick question: wouldn't that Fed tightening is a good thing for the banking sector? Banks can make a killer for lending money to the government in lieu of lending it to Average Joe?

ReplyDeleteGM Sam, following up on last evening's reply to your banks question, here's an article this morning that touches on the factors I mentioned:

Deletehttps://www.cnbc.com/2022/10/14/jpm-jpmorgan-chase-earnings-3q-2022-.html

Good question... The way to think about how the federal govt borrows money is to simply think in terms of the treasury auctions... i.e., the treasury issues debt (bills, notes and bonds) periodically, that can be purchased by anyone, and, yes, commercial banks (along with individuals, foreign governments, the Fed, state and local govts, mutual funds, etc) are indeed buyers (lenders to the govt)... With regard to monetary tightening, yes, to the extent that it raises interest rates, it can serve to improve bank's net interest margins, and, therefore, by itself, improve their bottom lines... However, to the extent that tightening hits the economy, it can hurt the banks as it negatively impacts the public's borrowing activity (they receive higher returns [charge higher interest rates to individuals and to companies than safe treasuries pay] from their loans to the private sector)... Plus banks invest in capital markets just like the rest of us, and to the extent that tightening hits the markets, it hits banks as well... Plus, their investment banking operations can get hit very hard as IPO's, corporate debt issuances (in a higher rate environment) that they underwrite, yada yada, can come to an abrupt stop in the latter stages of the tightening cycle... JP Morgan just announced that they expect their investment banking fees to decline by 50% going forward! Lastly, the big banks make a ton in trading fees, which can take a hit on certain products during a market downturn... Citi just "warned that a slump in revenue from trading spread products" will likely bring total trading revenue down by mid-to-high single digits this year (compared to last)...

ReplyDelete