As, alas, BCA analyst Davil Joshi pointed out in this morning’s chat,

“The winners of the old technology are never the winners of the new technology.”

His concern being that the market continues to, in his view, mistakenly bid up the companies that are essentially the winners of yesterday’s technology, that the true long-term winners of AI have yet to be discovered.

Per Alan Watts (on human nature):

I.e., the old Wall Street adage:

Here are the latest entries to our internal log... A little something for the bulls (particularly non-US equities bulls) and the bears... I.e., the picture remains very mixed:

Per Alan Watts (on human nature):

"We are driving a car, looking at the rear-vision mirror. The environment in which you believe yourself to exist is always a past one, it isn't the one you're actually in."And that, in reality, waves and cycles are as inevitable in economies and markets as they are in nature:

“…there is no such manifestation as half a wave. We do not find in nature crests without troughs and troughs without crests.”And that the longer the cycle, the more the crowd loses sight of this unalterable reality:

“The slower the wave goes the more difficult it is to see that the crest and the trough are inseparable.”I.e.,

“Trough implies crest just as crest implies trough.”Thus, call it human nature, recency bias, what have you, it's easy for markets to ultimately do what they do best.

I.e., the old Wall Street adage:

"Markets will do what confuses the most people."Here's another (old Wall Street adage) that I suspect will ultimately prove apropos for these times:

"Never run after a bus or a stock."Meaning:

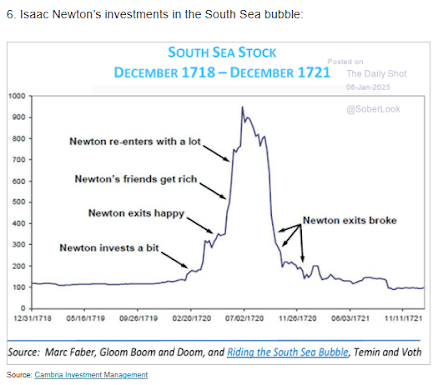

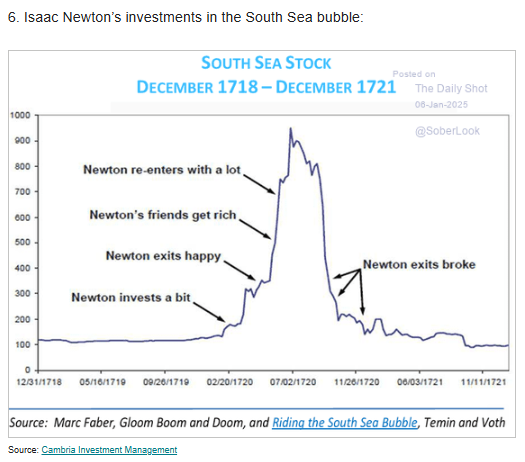

"If you have missed the opportunity to buy an asset at the right price, do not get so stuck on that asset that you go ahead with investing at the wrong price. The next investment opportunity will come along as surely as the next bus will come along. If you have enough patience, you can take advantage of the next opportunity."Sir Isaac Newton's personal experience speaks to the long long history of human nature playing itself out in markets (HT/Daily Shot):

As for the present:

After December's sizable drubbing in US equities (the S&P 500 Equal Weight Index declined by 6.4% on the month!!), the start to 2025 has seen quite the volatility:

Suffice to say that this pattern of opening up and closing down on the trading day, is, well... not bullish... But we won't get carried away just yet -- one week does not a trend make!

Now, that last point made, at some point -- and this I can promise -- there will be a dip that simply won't get bought, in any sustainable fashion, that is... Not saying that the next bear market is upon us, for all we know it could be months, if not years, away, it's just that, as we've been illustrating, existing market dynamics demand that we keep our wits about us.Here are the latest entries to our internal log... A little something for the bulls (particularly non-US equities bulls) and the bears... I.e., the picture remains very mixed:

1/7/2024

The degree of concentration in today's US stock market remains historic!

I sympathize with Bespoke’s concern re: NVDA:

“We can’t help but note that NVDA has ridden a very specific product specialty to incredible highs and is now announcing a much wider footprint on the back of that surge as well as an all-encompassing, utopian vision for its products. That sort of arc doesn’t guarantee dramatic downfall but it certainly does ring in the same tune as a hubristic peak.”

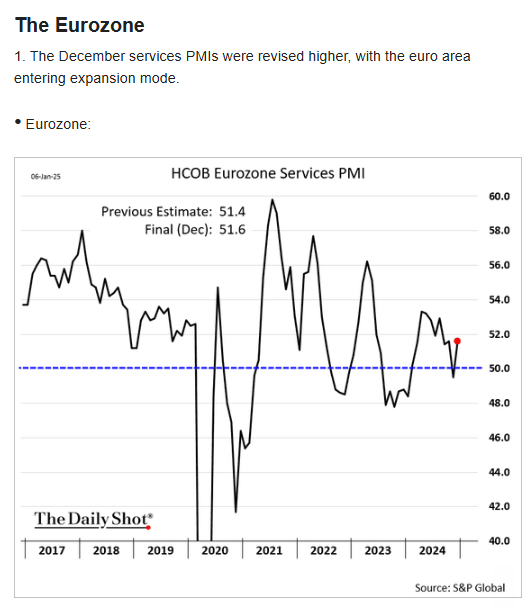

Eurozone PMIs are improving across the board:

1/6/2025

Of economic note (HT Bespoke):

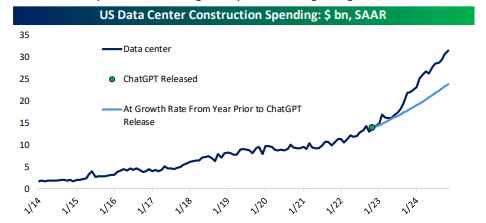

"Microsoft. On Friday, a blog post from Microsoft (MSFT) reported the company plans to spend $80bn globally on data centers during the fiscal year ending June 2025. “More than half” of that investment will be in the US.

As shown in the chart below, data center construction reported by the US Census is running around $30bn annualized, well short of the $40bn MSFT’s letter implies for its own spending let alone all the other hyperscalers. One major reason is the distinction between structures (measured by the Census) and all the equipment that goes into them (including chips, the various support systems that help keep them powered and cool, and so forth). Regardless, it’s clear that the spending on data centers is not slowing down any time soon, a major domestic economic catalyst as well as a sign the pace is rolling along."

Nothing scary about global PMIs right here (HT Bespoke):

"S&P Global PMIs. To start the week, we got a range of PMI readings from S&P Global tracking like-for-like measures of services or broad activity across sectors in a wide range of countries. Services readings in the largest economies (China, India, and the Eurozone) all picked up, and while all remain similar to recent readings (including India, which remains one of the strongest PMI readings in the world) they are nonetheless stronger than recent levels.

As for frontier economies in the Persian Gulf or Middle East, average composite readings picked up to the fastest pace since June of 2023. Sub-Saharan African readings are more stable and rose."

The below is bullish for our palladium position:

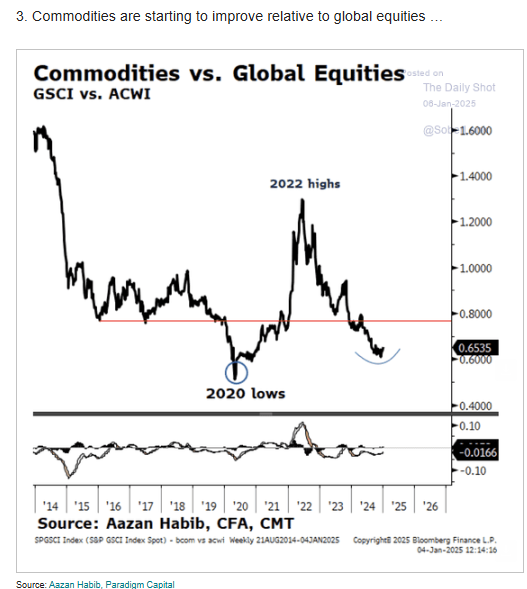

Commodities looking technically-compelling relative to equities:

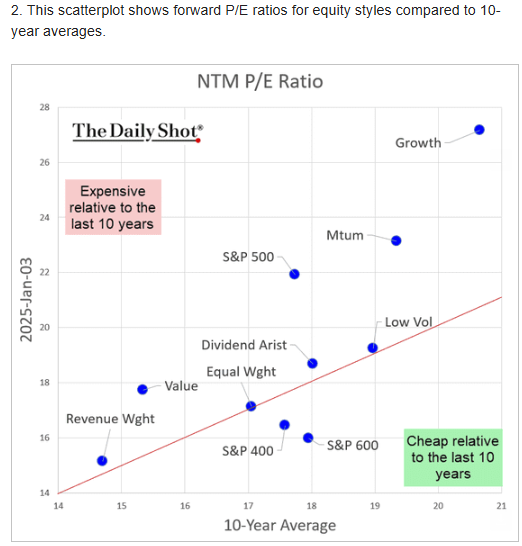

Among US equities, small and midcap are the only things “cheap” relative to 10-year average p/e:

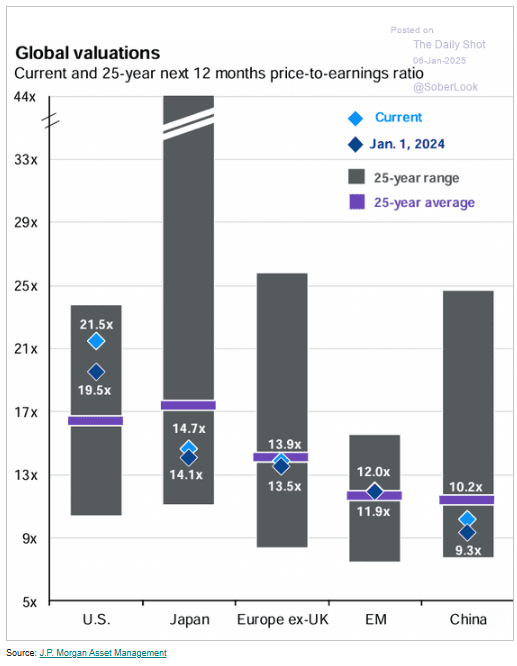

ROW looks relatively attractive:

Liquidity red flag for US equities right here:

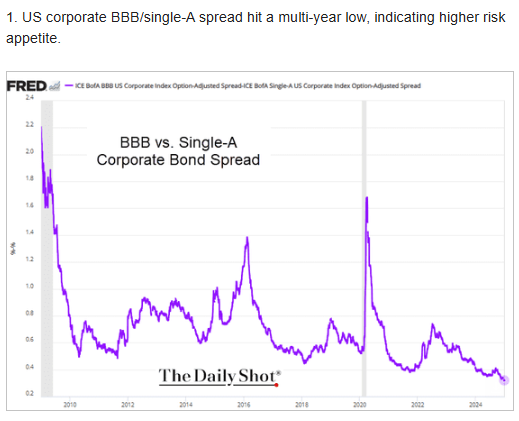

Amazing how sanguine the credit markets remain!

And human nature has played out over and over, and over, again since!

↓

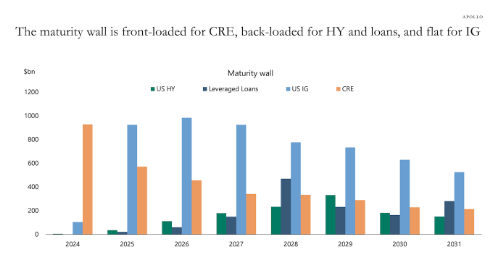

Peter Boockvar on what’s to come in terms of debt refinancing amid corporations and the federal government:

"'Long and variable lags' when it comes to the impact of monetary policy on the economy is something we've heard all about for years with the only debate being how long and how variable. After 15 years of essentially zero interest rates preceding the 2022 rise in them, I still believe the impact will be very long and very variable as long as interest rates still stay higher for longer, which I believe they will. Below is a chart from my friend Torsten Slok back in October that he put out in his daily writings quantifying the maturity wall in coming years in high yield, leveraged loans, investment grade and commercial real estate. As seen, the biggest jump over the coming years is from investment grade companies.

Now we don't have to worry about the credit quality of these IG names but I do want to point out that the interest rate this debt will refi into will be a few hundred basis points above the rate on the maturing loan which was most likely priced pre 2022. Keep in mind that one of the key factors in the notable rise in corporate profit margins over the past 20 years has been artificially low interest expense. That along with the lower corporate tax rate and low labor costs.

With respect to the US government's maturity wall this year, my friend Stephanie Pomboy in a recent note mentioned the $10 trillion of maturing US debt this year with about $6 trillion being bills and $4 trillion being longer term notes. Those notes will likely refi also about 200 bps above the maturing rate. On $4 trillion, that's an added $80 billion of interest expense and doesn't include the about $2 trillion extra of debt the US government needs to sell just to finance the budget deficit. By the way, the US Treasury is issuing $119b of new debt just this week.

As for private equity and what higher for longer rates mean for them, this was an interesting tidbit I read over the weekend in the FT 'Long View' column from John Plender. He cites this from McKinsey, "that roughly two-thirds of the total return for buyout deals entered in 2010 or later and exited in 2021 or before can be attributed to broader moves in market valuation multiples and leverage, rather than improved operating efficiency." In other words, much of private equity's success during that time period was due to easy money and a low cost of funding deals."

1/4/2025

Listening to Russell Napier on Hidden Forces... excellent, far-reaching interview! I sympathize:

On asset allocation:

"I try to focus on at least a 3-year time horizon... So, on a 3-year time horizon I'd be happy to go for value equities over cash... But, if you really think that you can time this and that equities are going to get even cheaper, and you can wait a bit, and even the value equities will get cheaper, and they probably would if the S&P fell dramatically, then you can take the risk of owning cash, but I never own a huge amount of cash because timing these things is difficult... There's lots of stocks all over the world, I could mention the UK, that just look unbelievably cheap, unbelievably cheap! And it's hard to imagine that anybody with a reasonable time horizon isn't going to make some money, even if you lose in the short run as things fall in sympathy with the S&P 500."

https://hiddenforces.io/podcasts/national-capitalism-death-of-the-international-monetary-system-russell-napier/

1/3/2025

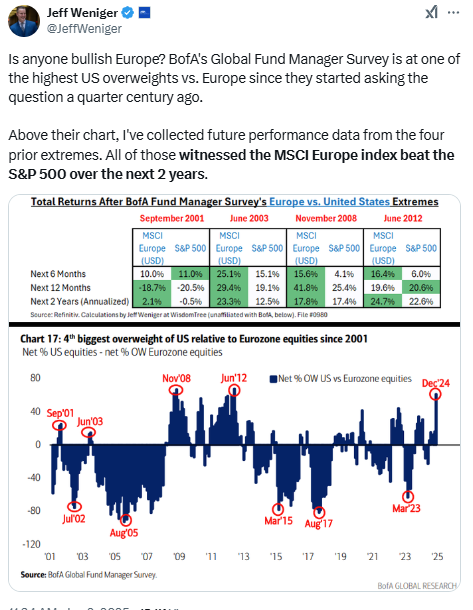

More on the relative (in a contrarian sense) attractiveness of Eurozone stocks right here:

No comments:

Post a Comment