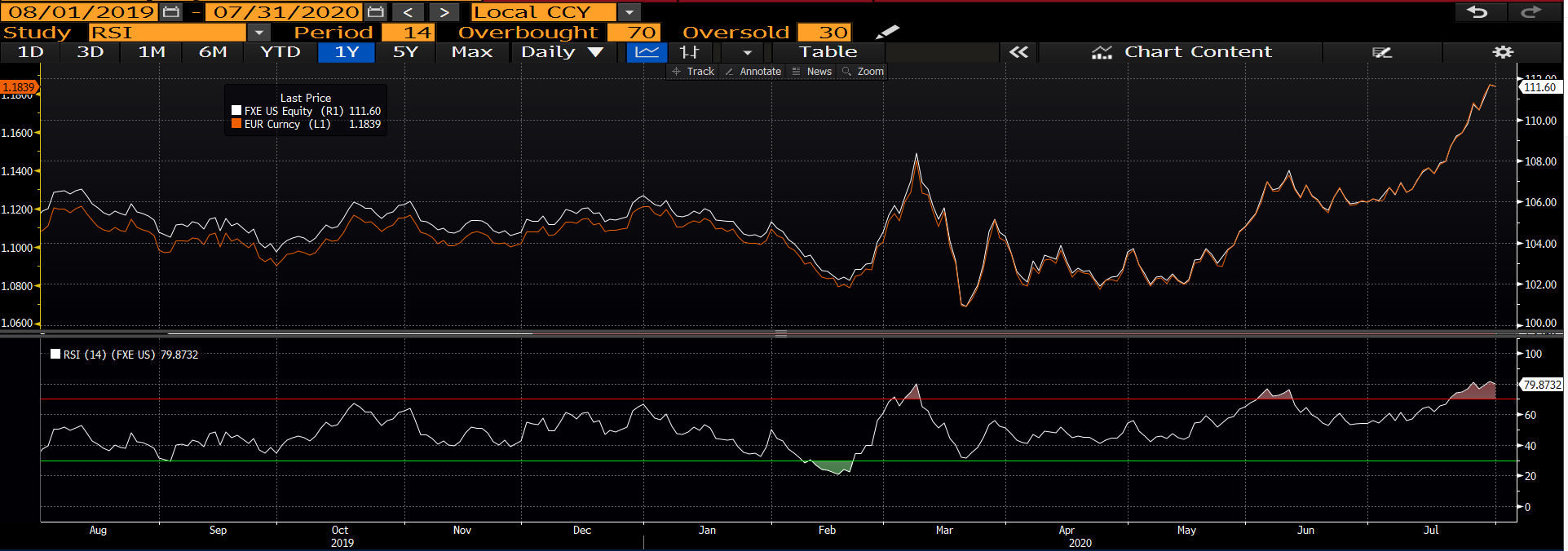

European equities are seeing mostly red this morning, with 15 of the 19 markets we track trading lower. Among other things, Eurozone exporters have a problem, their currency; it's been on a real tear of late.

Here's our chart:

The recent bailout love-fest (not really, but there were hugs) has the world -- via the currency -- thinking there are better days ahead for the block. However, when you're a European exporter and your currency's making everything markedly more expensive for your already limping foreign customers, well, let's just say that you're right now not feeling the love...

As for US stocks this morning, despite last night's ostensibly stellar earnings reports from the companies' stocks that have literally driven the US market this year, the Dow's down 155 points (-.59%). The S&P is off -.18%, the Russell 2000 is off a big -2.3%, but the Nasdaq, where those names account for 40% of what goes on in there, is up .55%.

The VIX (SP500 volatility) is up 2.75%, while the VXN (Nasdaq vol) is essentially flat.

Gold's up $18, silver's rebounding from its recent selloff, up 3.2%, copper's down -1% and the ag complex is mostly green this morning.

The 10-year treasury's yield is higher (price lower) and the dollar is up a smidge, .1%.

Our core portfolio is off as well this morning, by -.42%, with our commodities positions -- and of course the put hedge (+5.6%) -- being the only holdings working for us; silver and ag notably; +3.2% and 1.2% respectively.

Next up, later today, our weekly macro update.

Have a great day!

Marty

No comments:

Post a Comment