Here's the intro to our latest internal report on our own Equity Market Conditions Index:

7/31/2023 PWA EQUITY MARKET CONDITIONS (EMCI) INDEX: -41.67 (+16.66 from 6/30/2023)

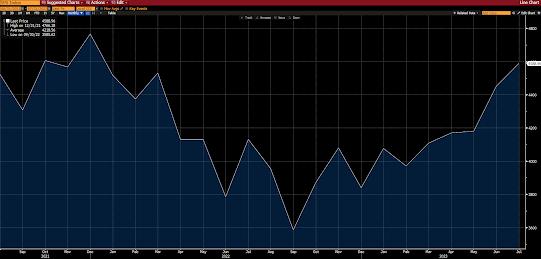

SP500 past 30 days, +3.11%:

SP500 Equal Weight past 30 days, +3.36%:

Despite the overall deterioration of equity market conditions recorded in our June report, stocks continued their 2023 rally through July.As we enter August, conditions have improved by 16 points... However, at -42, we're still looking at a notably poor go-forward setup for US equities.

Our bullish (bearish equities) end-of-June technical assessment of the dollar entirely missed the mark during the first half of July… I.e., DXY plunged through 7/13, providing a tailwind for stocks that carried through to month-end, despite the dollar’s second-half rebound.

At the end of the day, and clearly, the equity market’s continued rally through July reflected a notable move in sentiment (bearish to bullish) – as bears capitulated and joined the buying spree.As it stands, individual and advisor sentiment has reached concerningly bullish levels, representing a flip versus the beginning of the year -- essentially thinning the underlying equity market support that comes from large-scale defensive positioning.In terms of sentiment overall, however, our fear/greed barometer went from bearish (too much optimism) to neutral by the end of July – reflecting Nasdaq futures speculators turning net short and the put/call ratio spiking from 50 to 70 the past few days of the month (denoting a defensive bias heading into August).

Bottom line: Given what are historically-high US equity market valuations, what remains relatively tight monetary policy, generally high geopolitical risks, notably uncertain economic conditions (above average recession odds, per the PWA Index, on a 6-12 month outlook), lopsidedly bullish market sentiment (surveys), and, on-balance, tight credit market conditions, odds that the positive market action of late ultimately turns out to be a classic “blowoff top” are too elevated for us to add measurable risk to our current core allocation.

Hence, we believe it remains most prudent to hedge any extreme downside risk by actively/prudently managing our SPX put positions, and by maintaining our current overweights to cash, to gold, to staples and healthcare equities for the time being.

Inputs that showed improvement:

Economic Conditions (from negative to neutral)

Sentiment (from negative to neutral)

Inputs that deteriorated:

none

Inputs that remained bullish:

Sector Leadership

Inputs that remained bearish:

US Dollar

Interest Rates and overall liquidity

Fed Policy

Valuation

Geopolitics

Credit conditions

Inputs that remained neutral:

Fiscal Policy

SPX Technical Trends

Breadth

EMCI since inception:

SP500 since EMCI inception:

Europe, on the other hand, is mostly lower so far this morning, with 12 of the 19 bourses we follow trading down as I type.

US equity averages are mostly up to start the session: Dow by 128 points (0.36%), SP500 up 0.58%, SP500 Equal Weight down 0.03%, Nasdaq 100 up 0.86%, Nasdaq Comp up 0.98%, Russell 2000 down 0.05%.

As for yesterday’s session, US equity averages traded lower: Dow down 0.2%, SP500 down 0.3%, SP500 Equal Weight up 0.2%, Nasdaq 100 down 0.2%, Nasdaq Comp down 0.1%, Russell 2000 down 0.3%.

This morning the VIX sits at 14.93, down 6.22%.

Oil futures are up 0.50%, nat gas futures are up 1.33%, gold's up 0.58%, silver's up 0.74%, copper futures are down 1.22% and the ag complex (DBA) is up 0.28%.

The 10-year treasury is up (yield down) and the dollar is down 0.64%.

Among our 34 core positions (excluding options hedges, cash and money market funds), 27 -- led by MP Materials, VNM (Vietnam equities), EWW (Mexico equities), XLE (energy stocks) and Range Resources -- are in the green so far this morning... The losers are being led lower by HACK (cyber security stocks), DBB (base metals futures), Dutch Bros, XME (base metals miners) and AT&T.

"...my greatest discovery was that a man must study general conditions, to size them so as to be able to anticipate probabilities."

Have a great day!

Marty

No comments:

Post a Comment