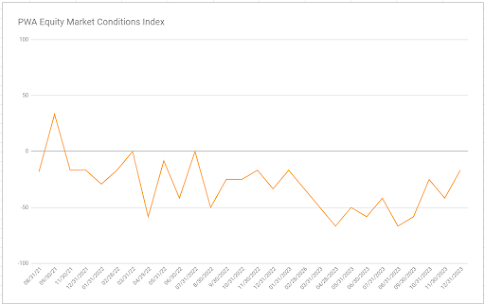

12/31/2023 PWA EQUITY MARKET CONDITIONS INDEX (EMCI): -16.67 (+25 from 11/30/2023)

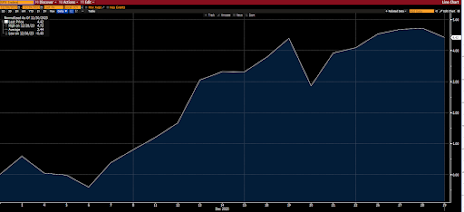

SP500 Index December 2023, +4.42%:

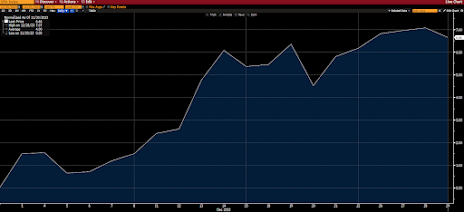

SP500 Equal Weight Index December 2023, +6.66%:

As we pointed out in November’s report, despite an overall deterioration in conditions, strong seasonality was such that a continuation of the then rally should come as no surprise.

From last month’s report:“Seasonality, on the other hand, is very strong right here, so it’s certainly not out of the question for stocks to continue rallying -- with these extended factors persisting -- for a few more weeks going forward.”And while a number of those “extended factors” indeed persisted, conditions, while still negative, did see a notable boost as December wound down… And one of the factors that contributed to that boost happens to be THE one that market actors are most-intensely focused on, Federal Reserve policy.

Here’s from the body of this report:"Fed-speak has turned notably more dovish, which presents a tailwind for stocks… While “soft landing” seems to be the current Wall Street consensus, the 6 cuts discounted by fed funds futures for 2024 doesn’t happen outside of recession, in our view.The Fed’s more accommodative stance has us upgrading our Fed Policy component to positive.”The go-forward setup:

The setup heading into January improved in the context of Fed policy and overall equity market breadth… Serious headwinds – the dollar, interest rates (technical setup), the (equity market) technicals and sentiment – however, as we enter January, puts the present rally on overall shaky legs… But, as we stated with regard to December, this doesn’t mean a correction begins right as January gets underway… It simply suggests that the go-forward setup, on balance, remains too precarious to add risk at this juncture.

Inputs that showed improvement:

Interest Rates and overall liquidity (from negative to neutral)

Fed Policy (from neutral to positive)

Breadth (from neutral to positive)

Inputs that deteriorated:none

Inputs that remained bullish:

Sector Leadership

Credit conditions

Inputs that remained bearish:

US Dollar

Valuation

Economic Conditions

Geopolitics

SPX Technical Trends

Sentiment

Inputs that remained neutral:

Fiscal Policy

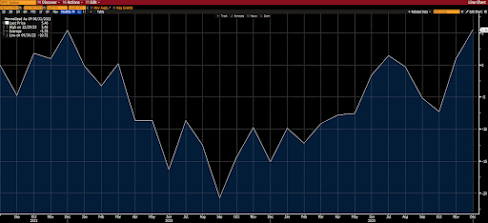

EMCI since inception:

SP500 since EMCI inception:

COMPONENT ANALYSES:

1. US DOLLAR: -1 (nc)

Per the below, our view of the dollar heading into December was “near-term bullish,” which was bearish for stocks, based on the prevailing character of equity market trading.

From last month’s analysis:“...as we enter December, the technicals reflect a near-term bullish profile for the dollar (bearish influence on stocks):The early December action in the dollar confirmed the technical setup referenced above, retracing 40% of the November downtrend by the 6th of the month... That, however turned out to be it for the December dollar rally, as price consolidated over the next 5 days, then rolled over notably the 12th, 13th and 14th, in response to the surprisingly (shockingly to some) dovish stance by Fed Chair Powell during the December meeting press conference.

Hence, we’re rerating the dollar to positive heading into December, which, again, reads near-term bearish for equities.”

As it turned out, per the following chart, the retracement formed a classic bear flag pattern that played out in virtual textbook fashion.

Ultimately, however, by the end of December, price moved back into a bullish falling wedge pattern, accompanied by bullish divergences on both the MACD and the RSI… We're therefore maintaining our short-term bullish outlook for the dollar, which presents a potential headwind for equities as we enter the new year.

Asian equities traded down overnight, with 9 of the 16 markets we track closing lower.

Same for Europe so far this morning, with 14 of the 19 bourses we follow trading down as I type.

US equity averages are lower to start the session: Dow down 99 points (0.26%), SP500 down 0.68%, SP500 Equal Weight down 0.40%, Nasdaq 100 down 1.21%, Nasdaq Comp down 1.24%, Russell 2000 down 0.33%.

As for Friday’s session, US equities closed lower: Dow by 0.1%, SP500 down 0.3%, SP500 Equal Weight down 0.2%, Nasdaq 100 down 0.4%, Nasdaq Comp down 0.6%, Russell 2000 down 1.5%.

This morning the VIX sits at 13.97.

Oil futures are down 0.25%, nat gas futures are up 2.11%, gold's up 0.21%, silver's up 0.52%, copper futures are down 0.69% and the ag complex (DBA) is up 0.39%.

The 10-year treasury is down (yield up) and the dollar is up 0.77%.

Among our 32 core positions (excluding options hedges, cash and money market funds), 10 -- led by Range Resources, XLE (energy stocks), Johnson & Johnson, AT&T and SLV (silver) -- are in the green so far this morning... The losers are being led lower by XLK (tech stocks), FEZ (Eurozone equities), VWO (emerging mkt equities), VPL (Asia-Pac equities) and DEM (emerging mkt equities).

Per our latest messaging:

"The leaders of today may not be the leaders two years from now" --Jesse Livermore

Have a great day!

Marty

No comments:

Post a Comment