Please keep in mind that this monthly analysis is in no way designed, or intended, to be a market timing indicator... But rather, it serves as a general assessment of the present risk/reward setup for primarily the US equity market; as history has proven, time and again, that stock market action -- in either direction -- can defy fundamental logic for extended periods of time.

Ultimately, however, and make no mistake, even in a world where powers-that-be strive mightily to keep asset prices elevated, fundamentals do tend to matter!

Now, all of the above, and the below, said, we have seen some recent improvement in overall economic conditions -- i.e., odds still favor recession going forward, but less-so of late... This is something we're of course paying very close attention to.

Our bottom line: Our aim here at PWA is to manage our clients' long-term assets in a manner we deem most prudent from a risk/reward perspective, given our deep, ongoing assessment of global macro conditions.

Asian equities were mostly green overnight, with 10 of the 16 markets we track closing higher.

Same for Europe so far this morning, with 15 of the 19 bourses we follow trading up as I type.

US equity averages are mixed to start the session: Dow up 21 points (0.06%), SP500 down 0.13%, SP500 Equal Weight down 0.71%, Nasdaq 100 down 0.16%, Nasdaq Comp down 0.37%, Russell 2000 up 0.51%.

This morning the VIX sits at 13.60.

Oil futures are up 1.11%, nat gas futures are down 2.69%, gold's up 0.39%, silver's flat, copper futures are up 0.47% and the ag complex (DBA) is down 0.23%.

The 10-year treasury is up (yield down) and the dollar is down 0.13%.

Among our 33 core positions (excluding options hedges, cash and money market funds), 25 -- led by EWZ (Brazil equities), VWO (emerging mkt equities), XLB (materials stocks), XLRE (REITs) and DEM (emerging mkt equities) -- are in the green so far this morning... The losers are being led lower by AT&T, XLK (tech stocks), XLP (consumer staples stocks), Range Resources and XLC (communication stocks).

01/31/2024 PWA EQUITY MARKET CONDITIONS INDEX (EMCI): -41.67 (-25 from 12/31/2023)

SP500 (cap-weighted) Index January 2024, +1.59%:

SP500 Equal Weight Index January 2024, -0.89%:

The positive SP500 (cap-weight) move in January was not inconsistent with the EMCI improvement reflected in the December 31 report... While the negative SP500 Equal Weight Index move in January more comports with the overall EMCI message.

I.e., January’s gain in the SP500 cap-weighted index gibed with an accommodative turn in Fed-speak, as well as with a marked improvement in breadth… By the end of the month, however, both metrics – along with sector leadership – deteriorated to the point of taking our overall score notably lower.

Here's our own (bullish) commentary on Fed policy from the end-of-December report:"Fed-speak has turned notably more dovish, which presents a tailwind for stocks… While “soft landing” seems to be the current Wall Street consensus, the 6 cuts discounted by fed funds futures for 2024 doesn’t happen outside of recession, in our view."“The Fed’s more accommodative stance has us upgrading our Fed Policy component to positive.”Versus our commentary in this (our latest) report:"Fed-speak has taken yet another (in this case less-dovish) turn, based on the statement, and, in particular, the press conference from the late-January policy meeting… Powell essentially snuffed out market expectations of a March rate cut… Inspiring us to re-rate our fed policy input down a notch, to neutral."While overall stock market breadth improved in December to the point that had us upgrading its score to positive, the setup turned notably in the opposite direction by the end of January.

Here’s the latest on breadth:10. BREADTH: -1 (-2)SPX/SPW/RTY shows breadth deteriorating markedly during January:1-month:

Year-to-date:

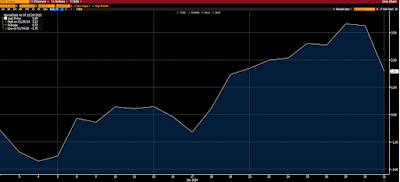

SPX A/D LINE: The A/D line continued to move with price (although with less steepness) during January:

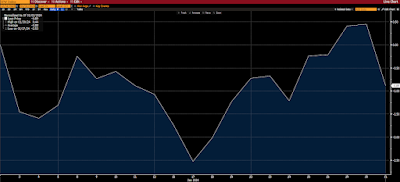

NASDAQ COMP A/D LINE: Massive bearish divergence remains (exceedingly ugly/concerning breadth):

65% of SPX members trading above 50-dma, which reflects a slightly bearish divergence vs price:

72% above 200-dma:And on sector leadership (from this report):6. SECTOR LEADERSHIP: 0 (-1)

Among growth/cyclical sectors: Only Tech outperformed SPX this past month. Hence our downgrade from positive to neutral:

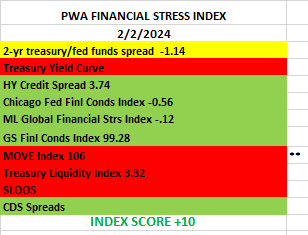

The go-forward setup: The setup heading into February has deteriorated markedly, with only one (although significant) input – credit conditions – scoring positive.

Here's our latest on current credit conditions (note the inflation-risk aspect):12. CREDIT MARKET CONDITIONS: +1 (nc)

Credit conditions continue to reflect a net-easing in overall financial conditions… While this is bullish for equities and merits a positive score herein, easing conditions presents a notable tailwind for inflation, a potential not-small challenge for the Fed, in the present environment:

Bottom line: Per the above, and the following, current overall conditions leave us uninspired to add measurable risk, or to hedge less, at this juncture.

Inputs that showed improvement:

US Dollar (from bearish to neutral)

Inputs that deteriorated:

Fed Policy (from positive to neutral)

Sector Leadership (from positive to neutral)

Breadth (from positive to negative)

Inputs that remained bullish:

Credit conditions

Inputs that remained bearish:

Valuation

Economic Conditions

Geopolitics

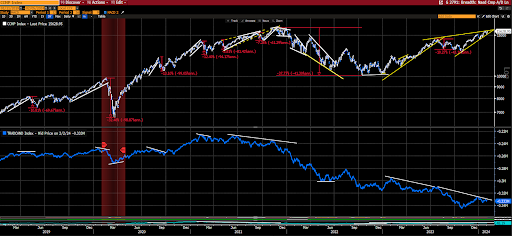

SPX Technical Trends

Sentiment

Inputs that remained neutral:

Interest Rates and overall liquidity

Fiscal Policy

Asian equities were mostly green overnight, with 10 of the 16 markets we track closing higher.

Same for Europe so far this morning, with 15 of the 19 bourses we follow trading up as I type.

US equity averages are mixed to start the session: Dow up 21 points (0.06%), SP500 down 0.13%, SP500 Equal Weight down 0.71%, Nasdaq 100 down 0.16%, Nasdaq Comp down 0.37%, Russell 2000 up 0.51%.

This morning the VIX sits at 13.60.

Oil futures are up 1.11%, nat gas futures are down 2.69%, gold's up 0.39%, silver's flat, copper futures are up 0.47% and the ag complex (DBA) is down 0.23%.

The 10-year treasury is up (yield down) and the dollar is down 0.13%.

Among our 33 core positions (excluding options hedges, cash and money market funds), 25 -- led by EWZ (Brazil equities), VWO (emerging mkt equities), XLB (materials stocks), XLRE (REITs) and DEM (emerging mkt equities) -- are in the green so far this morning... The losers are being led lower by AT&T, XLK (tech stocks), XLP (consumer staples stocks), Range Resources and XLC (communication stocks).

"We shall not grow wiser before we learn that much that we have done was very foolish."

--Frederich Hayek

Have a great day!

Marty

Marty

No comments:

Post a Comment