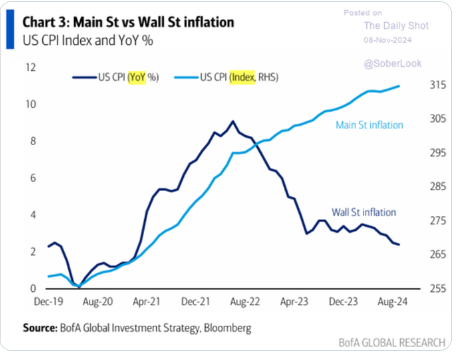

At the end of the day, or, let’s say, in reality, while politicians, and financial markets, may celebrate a calming of inflation’s go-forward rate-of-change (purple line), consumers – particularly those in the lower 40% of income earners – continue to suffer (some, devastatingly) from inflation’s 4-year cumulative effect (blue line).

HT Bob Elliott

Below is Peter Boockvar's reporting on this week's Housing Index release… Still net-contractionary, but, clearly, sentiment is picking up post-election… That said, the policies proposed don’t help the labor headwind mentioned (largely immigrant labor in the industry), nor materials prices.. Although they do offer a potential tailwind via deregulation:

"The November NAHB home builder index rose 3 pts m/o/m to 46, better than the estimate of 42, though still below 50. The upside was mostly due to a jump in the Expectations component to 64 from 57. The Present Situation is still below 50, though barely at 49 vs 47 last month. Reflecting still the big challenge of affordability, Prospective Buyers Traffic was just 32 but up 3 pts from October.

The NAHB is pointing to the election results as reason for the lift in builder confidence. “With the elections now in the rearview mirror, builders are expressing increasing confidence that Republicans gaining all the levers of power in Washington will result in significant regulatory relief for the industry that will lead to the construction of more homes and apartments.” The supply side of the home industry certainly hopes for more home building, as does the first time home buyer but many of the regulatory levers that can enable more homebuilding is more at the local and state level in terms of zoning and permitting.

On the building side, the NAHB also said, “While builder confidence is improving, the industry still faces many headwinds such as an ongoing shortage of labor and buildable lots along with elevated building material prices.” On the demand side, we know all about the affordability challenges that first time buyers face and it’s mostly the bigger builders that can ease some of the pain via mortgage rate buydowns and other discounting, more so than smaller builders.

All this as the pace of transactions of existing homes hover around 30 year lows and all the ancillary business activity that does not take place because of this, like buying paint, flooring, appliances, etc…"

Meanwhile, single family starts continue to trend uninspiring:

Not to mention, permits:

Make no mistake, this has a lot to do with mortgage rates:

Definitely some encouraging earnings commentary out there!

While I’ve been referencing mostly earnings reports that confirm our concerns over the economy, clearly, there are pockets of serious strength. HT P. Boockvar:

Instacart: "we are seeing very strong consumer demand. And in fact, we track that very closely and we look at a lot of data points. We haven't seen meaningful trade down, whether you look at it on a pair item, like types of item basis, whether you look at different types of retailers, with the notable exceptions of clubs being very strong. We are also not seeing different behaviors across income segments... And we think that's a testament to the fact that people really do value convenience and we are able to provide that to them."

From Disney: "we certainly feel like the consumer is strengthening...we obviously saw growth in domestic parks and certainly feel very positively about that. And that's our expectation going forward; a gradual strengthening in the consumer."

But, then again:

Advance Auto Parts: "This quarter results came in below our expectations as the sales softness that began in early Q3 persisted throughout the quarter. Macro headwinds and economic uncertainty continue to weigh on consumer spending, while our results were also impacted by other events such as hurricanes and the Crowdstrike outage."

Very different setup for the next bull market:

Like I keep saying, US stocks are historically-extended, relative to the rest of the world.

I.e., PWA and MRB Partners are on the same page on this one:

"...projected very low real earnings growth and a material de-rating indicate that U.S. stock prices will decline modestly in real terms over the next decade. Partly as a result, non-U.S. markets are poised to outperform the U.S. in the next decade, led by European and emerging market stocks."

Stay tuned...

No comments:

Post a Comment