Attention Clients, this is an important post to take in... Thanks for reading!

The following are excerpts from the latest entries to our internal market log.

In summary.

1. Since the election:

- 6 of the US major equity sectors are up, 5 are down.

- The US is the only major regional equity market in the green... The others featured are notably in the red.

- Among the major industrial commodities we track, all have sold off significantly, save for natural gas.

- Among the ag commodities we track, 8 are up, 6 are down.

- US Treasuries have taken quite the hit (as interest rates popped higher), Investment grade corporate bonds are flat, junk bonds are up slightly.

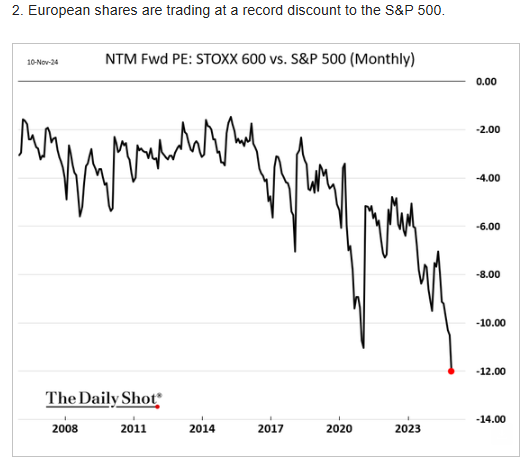

2. Foreign equities are all-time cheap relative to the US.

3. US equities are, by themselves, at (or near) all-time expensive valuations.

3. Zip Recruiter warns about the state of the labor market and, therefore, the economy.

4. Me (via an email with a friend) on the prospects for commodities going forward, the nat'l debt, and the history of the early stages of world-changing technologies.

Bottom line, the rip-roaring rally of the past week has been the definition of concentrated. I.e., not so great for balanced portfolios that diversify across asset classes, sectors and regions... But, make no mistake, the setup, as we ultimately move into the next cycle, offers many historically-attractive opportunities for macro-centric portfolios.

Read on for context.

11/12/2024

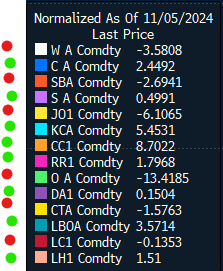

Global Equity Indices performance since the election (only US in the green):

Commodities performance since the election:

Ag Commodities performance since the election:

US Bonds performance since the election:

11/11/2024

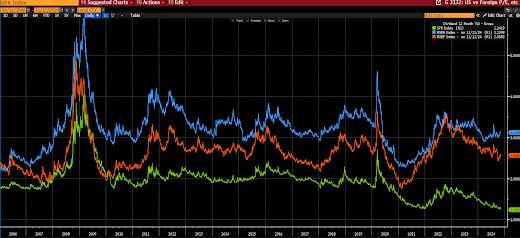

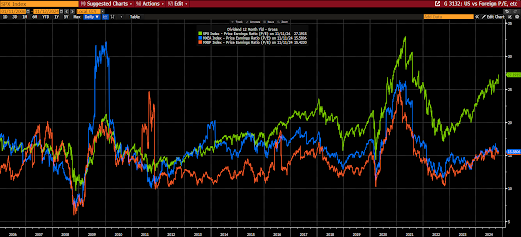

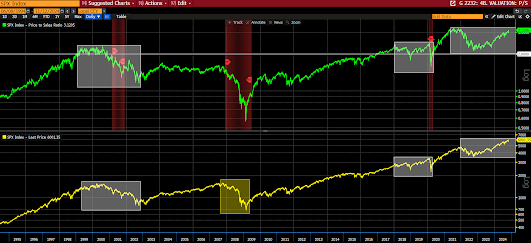

Like I keep saying, foreign equities are historically cheap, in relation to US equities:

Our charts (green = US, blue = Developed non-US, orange = Emerging mkts).

Current dividend rate:

Price to Earnings Ratio:

Price to Sales Ratio:

Price to Book Ratio:

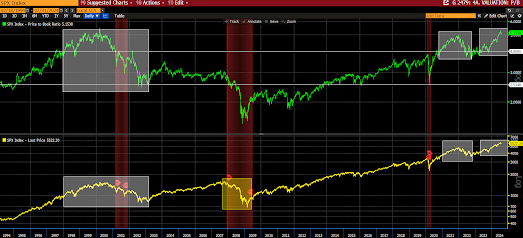

Forgetting about US relative to ROW for now, here are 30-yr graphs of the above valuation metrics for the SP500… Note that we’ve never remedied such extremes without quite the drawdown… The most tepid of the shaded examples was -20% (although the current is yet to play out)... The others were -50%, -57% and -25% respectively (the -20% and -25% [still in the currently-extended P/S state] drawdowns occurred outside of recessions)...

Price to Earnings (top panel… sp500 bottom):

Price to Sales:

Price to Book:

11/7/2024

The following, via Peter Boockvar, on/from Zip Recruiter supports our view that there remains not-small recession risk going forward:

"ZipRecruiter continues to navigate a protracted labor market downturn." Their Q3 revenues fell 25% y/o/y "primarily due to reduced demand from SMBs (small and medium sized businesses) with continued uncertainty and volatility in the labor market." They said their bigger customers were a little better in terms of hiring demand.

"While each labor market cycle is distinct, by several measures, this is one of the more prolonged downturns in hiring activity. Seasonally adjusted hires have declined on a y/o/y basis every month since August of 2022, which is approaching the same duration in hiring declines as the recession of 2008. Further, the great stay continues with the currently employed leaving their jobs at the lowest rate since 2015, excluding the onset of the Covid pandemic. This persistent reduction in employee churn is further driving down hiring levels."

In terms of job sectors, "healthcare, despite softness we saw, remain fairly robust compared to other verticals and healthcare is a significant, obviously, chunk of the economy. So that was sort of the notable bright spot. I would say on the more negative side of things, we saw transportation, storage, travel and leisure being on the weaker side of the ledger, where we saw softer performance. And then in terms of those early verticals, you talked about finance and technology in particular, which is where we saw weakness at the very beginning of this particular downturn back in mid '22. They were sort of in the middle, in between the bookends of healthcare being a little big stronger and things like transportation and storage being on the weaker side."

And this is what we've seen in the jobs data from both ADP and the BLS where healthcare has been the pretty consistent job hire, along with government, with more of a mixed bag elsewhere. Do not discount what ZipRecruiter has to say as they are a major digital/online recruitment site.

11/6/2024

My response to a friend's email regarding the nat'l debt, and reference to a WSJ article featuring Blackrock's Larry Fink:

"Just read the article, sure, the numbers support that narrative.

Now, we have to be realistic about our capacity to absorb the kind of investment he's talking about. Currently, just the global green energy mandates over the next few years require more (and I'll just name one input) copper than the world currently has the capacity (existing mines, etc.) to produce... Of course I'm talking higher resources prices in the years to come, and, as you know, the cure to higher prices is higher prices... I.e., higher prices lead to expansion in production, yada yada... Thing about my example (copper) is that a new mine takes on average 16 years from discovery to production.

He mentioned the stress on the grid to power all of the AI "production." Have to think in terms of limited (at current) resources needed to expand that capacity there as well. (there's a reason bonds tanked [yields spiked higher] today -- exacerbating the trend of the past few weeks)

This has been the narrative of so many optimists (opportunists -- Fink being the poster child of our time) over all these years of deficit spending... Now, I am indeed an optimist on the rich investment environment to come -- should be no surprise that we're bullish on much of the commodity complex going forward!

With regard to the national debt, amid the massive deficit spending to come... The Laffer Curve notwithstanding, cutting taxes and ramping up spending (infrastructure, etc.) has unequivocally never slowed down the debt train.

Now, all that aside, there remains zero threat to the dollar's world reserve status at the moment... There is -- and I've written about this a lot, and commented on videos the past couple of years -- a solution that is virtually the only way out of this mess... It's called yield curve control (YCC), and it's how the US inflated its way out of the only other time in history where we saw nat'l debt in excess of GDP -- that was just after wwII...

The Fed bought up all the treasury issuance necessary to cap yields at 2.5%... Inflation was allowed to run consistently hotter during that time (circa 1945 to 1952) than the cost of the nat'l debt... I.e, GDP (inflation of the "value" [read price] of the goods and services we consume domestically), while no debt got paid off, grew faster than the debt.. Hence, by 1952 we had gone from 116% debt to gdp to 80%... Secular forces had evolved by then to the point where we didn't need the YCC any longer...

By the time Volker "needed" to raise rates to 20% (late 70s/early 80s) we were down to 30% debt to GDP... I.e., he had no constraints (other than simply economic) on raising rates to that extent... No way on earth with the present US debt and deficit backdrop can that be pulled off today... We're back to the mid-1940s scenario, and the same solution is what we'll virtually have to implement...

Fink talks about the railroad equating to AI... Read "The Engines That Drive Markets" and you'll get the history of every life-changing technology since the beginning of our country (including when railroads replaced canals).. .Without exception it was met with massive capital investment (we had 10,000 US Automobile companies in the early 20th century), that led to a massive bubble, that led to a massive bust, leaving the most robust (survivors) to take us productively into the new era... you and I of course lived through the internet scenario, and the financial engineering mania between then and the GFC...

Stay on your toes."

No comments:

Post a Comment