Often during client meetings I'll point to the large monitor on my office wall, not always to discuss a featured graph, but at times to discuss the monitor itself -- the fact that it costs a mere fraction of what its far inferior predecessor would've run me, say, 20 years ago.

Yes, one key deflationary feature of all of that productivity-enhancing information technology has been its own declining price over the years.

Well, amid inflation rates we haven't seen since the 70s, even tech (the price of) can't seem to help us out.

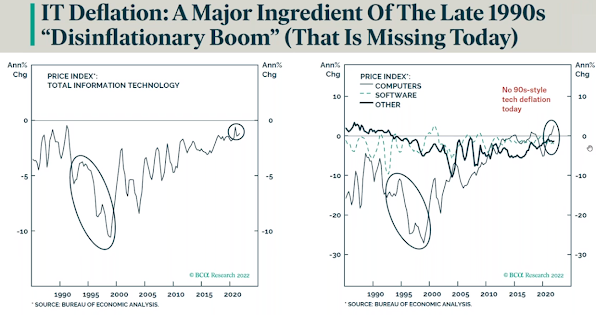

BCA research's left hand chart tracks the price of all IT since the start of the 90s. The right hand chart captures computers themselves, software and "other."

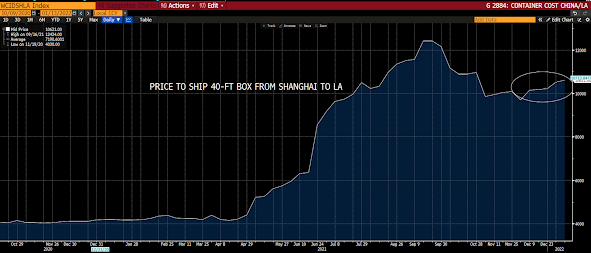

Like most in our space (our long-term bullish inflation narrative notwithstanding), we've been calling for a letting up of the rate of inflation come the spring. And while indeed base effects (comps relative to last spring when inflation was spiking) -- and some bottleneck relief -- will help that narrative, graphs like this one (the cost of shipping a container from Shanghai to LA),

“I’ve been doing this 30 years and I’ve never seen markets like this. This is a molecule crisis. We’re out of everything, I don’t care if it’s oil, gas, coal, copper, aluminum, you name it we’re out of it.”

Among our 39 core positions (excluding cash and short-term bond ETF), 23 -- led by ALB (lithium miner), AMD (chip maker), silver, Viacom/CBS and energy stocks -- are in the green so far this morning. The 16 losers are led lower by AT&T, Verizon, Indian equities, carbon credits and Nokia.

"People were quite literally throwing money at us, so why should we be telling them to stop? There is an institutional dynamic towards myopia in such situations still best summed up in the words of Sinclair Lewis: “It is difficult to get a man to understand something, when his salary depends upon his not understanding it!”"

Have a great day!

Marty

No comments:

Post a Comment