Each week we study exchange traded fund (ETF) flows among the countries, the asset classes and the sectors they track to help us get a sense of global investor sentiment.

At first blush, the country flow the past couple of weeks is perhaps counterintuitive.

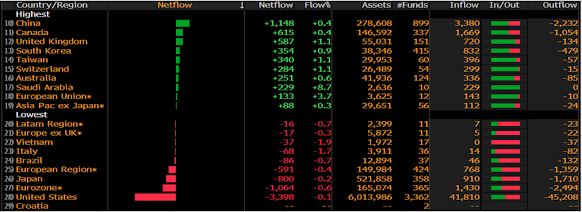

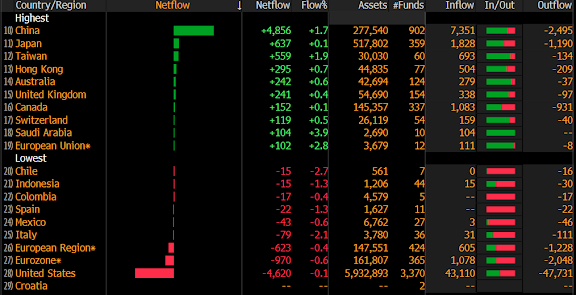

I.e., China, with all of its issues (self-imposed with regard to the locking down of millions of its people), has actually seen the highest net inflow the past two weeks running, while the US has seen notable net outflow:

Week ending 4/8:

Last week:

Now, at second blush, I believe we can suffice to say that the above is a reflection of policy (both monetary and fiscal). I.e., while China is promising to do what it takes to keep its economy afloat (and further exacerbate its debt bubble in the process), the US (central bank) is promising to do what it takes to bring inflation to its knees... Clearly, considering what drives markets these days, the former would be equity bullish, the latter bearish...

Speaking of sentiment, our own fear/greed barometer moved from +20 (net bearish) to flat (0) week-over-week. While sentiment among individual investors literally fell off a cliff -- the American Association of Individual Investors weekly survey has the bulls at a multi-year low of just 15.8% of its members -- futures traders have gone from net bearish to net bullish on the S&P 500 and the Nasdaq 100. Other measures of short interest and options positioning denote a general fence-sitting sentiment among market actors overall.

In our view, as I stated last Friday, with regard to the Fed, "the extent of the tightening they’re threatening is simply not fully discounted in stock prices."

The majority of Europe's bourses remain closed for Easter.

US stocks are mixed to start the session: Dow up 5 points (0.01%), SP500 up 0.08%, SP500 Equal Weight down 0.12%, Nasdaq 100 up 0.37%, Nasdaq Comp down 0.13%, Russell 2000 down 0.46%.

The VIX sits at 23.43, up 3.22%.

Oil futures are up 0.79%, gold's up 1.03%, silver's up 1.99%, copper futures are up 2.03% and the ag complex (DBA) is up 1.09%.

The 10-year treasury is down (yield up) and the dollar is up 0.27%.

Among our 39 core positions (excluding cash and short-term bond ETF), 17 -- led by silver, oil services companies, semiconductor stocks, base metals futures and gold-- are in the green so far this morning. The losers are being led lower MP Materials, AT&T, uranium miners, healthcare stocks and Disney.

The main message in Goodhart and Pradhan's The Great Demographic Reversal (published August 2020) jibes to a virtual T with our own long-term inflation thesis, and, with regard to central banks, is looking prescient right here:

"The world is still not ready to think about the inflation that is likely to rise structurally. Central banks will, soon enough, have to revert to their normal behaviour. The zero lower bound (ZLB) is largely the consequence of a combination of a China effect, an unprecedented demographic backdrop and the deepest cyclical shocks since the Great Depression, once during the financial crisis and more recently during the pandemic.

The re-birth of inflation is our highest conviction view among the effects of demographics, and it is one that both financial markets and policy-makers are dismissing at their own peril."

Have a great day!

Marty

Marty

No comments:

Post a Comment