Some interesting, if not encouraging, data out this morning...

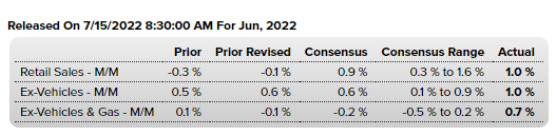

Retail Sales for June came in better than expected, with net positive revisions to the May numbers:

The Empire State Manufacturing Index killed expectations (to the upside):

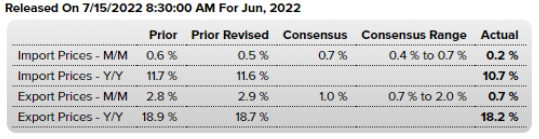

Import and Export Prices came in way under expectations. Especially month-on-month, which, as I've explained, is what you want to watch right here:

And while we know that the reported mountain of US consumer savings out there is concentrated among the wealthier among us (they say 70% of it) -- according to yesterday's Wall Street Journal the remaining 30% is quite diffuse:

"The hit from the pandemic proved short-lived for many. Two years since it began, household finances are remarkably strong.

At the end of March, households had $18.5 trillion socked away in deposit, savings and money-market accounts, more than $5 trillion above what they had heading into the pandemic, according to Federal Reserve data.

Cash reserves rose across income groups. JPMorgan, tracking 7.5 million of its own accounts, found that checking-account balances averaged nearly $1,400 among its lowest-income customers in the first quarter, up from under $900 before the pandemic. Among its highest-income accounts, balances rose to almost $7,000 from less than $5,500."

I must say, this is indeed encouraging stuff, particularly if, as the consensus seems to think, we're heading into recession.

Asian equities leaned red overnight, with 10 of the 16 markets we track closing lower.

Europe's in rally mode so far this morning, with 17 of the 19 bourses we follow trading up as I type.

US stocks are catching a bid to start the session: Dow down 309 points (1.01%), SP500 up 0.85%, SP500 Equal Weight up 0.53%, Nasdaq 100 up 0.74%, Nasdaq Comp up 0.60%, Russell 2000 up 0.13%.

The VIX sits at 25.38, down 3.86%.

Oil futures up 1.47%, gold's down 0.41%, silver's up 0.47%, copper futures are down 0.78% and the ag complex (DBA) is down 0.13%.

The 10-year treasury is up (yield down) and the dollar is down 0.34%.

Among our 35 (adjustments this morning netted us 3 fewer) core positions (excluding options hedges, cash and short-term bond ETF), 25 -- led by financial stocks, carbon credits, healthcare stocks, Nokia and energy stocks -- are in the green so far this morning. The losers are being led lower by MP Materials, utility stocks, Sweden equities, emerging market equities and gold.

"People get all excited about the price movements, but they completely misunderstand that there is a bigger picture in which those price movements happen. Price movements only have meaning in the context of the fundamental landscape. To use a sailing analogy, the wind matters, but the tide matters, too. If you don’t know what the tide is, and you plan everything just based on the wind, you are going to end up crashing into the rocks."

Have a great day!

Marty

Great Data! The data are quite encouraging in the short term. The market may expect a one (1) percentage, or 100 basis point, increase for the interest rate. Like you have been saying all along that the dynamic risk is still there and we are not near the bottom yet of 3500 S&P.

ReplyDeleteThanks Sam. Looking (as of right now) like .75 will be this month's rate hike. At least 2 Fed Governors have pushed back against the 100 bps for this month's meeting. And you'll want to pay attention to the commentary from WSJ columnist Nick Timiraos, all indications are that the Fed uses him to signal markets (so as to not shock them) ahead of their moves. He's strongly pushing back against the 100 bp hike. And Fed funds futures are now back to pricing in 75.

DeleteGot It! Thanks!

Delete