Now, before you read on, rest assured that while the following will not leave you feeling warm and fuzzy about the economy's, nor, therefore, the stock market's prospects going forward, there will nevertheless be opportunities for us to explore -- and exploit -- on our clients behalf as the future unfolds (some, ironically, generated by the conditions that I suspect lie ahead) ...

At this point the ball is entirely in the Fed’s court; barring, that is, a legitimate, lasting trade deal with China (virtually zero consequential progress was made this week, by the way) and trade peace going forward with the EU (both are required) -- a scenario that would by itself only favor, say, the intermediate-term (1 to 3-year) outlook.

I thus sympathize with Julian Brigden's (Macro Insiders) opinion that -- again, barring a major trade deal -- the Fed is now essentially the economy’s primary (if not only) hope, and that they’ll have to go a full 100 bp (cut) very soon if there’s any hope of ultimately extending the current expansion (my interpretation of his latest narrative). Although one might argue that -- despite the ballooning Federal budget deficit -- there’s room on the fiscal side in the U.S. to implement something (spending) and inspire a pickup in growth: Infrastructure spending, or maybe a cap gains tax cut (as suggested recently), would be your obvious examples -- we of course must seriously question the political will to accomplish anything along those lines for the foreseeable future.

Globally-speaking, Germany is in a much better position to implement consequential fiscal measures, but that’s not their way (although they’re beginning to rumble a bit, and I suspect they will [albeit tepidly] implement something [govt spending] if their already ugly economic trends continue to deteriorate). China can, and I suspect will (engage in more fiscal stimulus), although, that said, they do seem to be cognizant of their own debt issues and present bubble risks, so we’ll see.

A side note, and one that I have been quite bullish on as a potential game-changer -- and one that I’ll definitely keep my eye on -- is 5G. Unfortunately, as we sit here today, this potentially revolutionary game-changer in terms of productivity gains and so on is likely to face notable headwinds amid such a polarized, populist and protectionist-minded, backdrop...

The problem I have with the central-banks-can-save-the-day narrative is that unless a Fed-juiced stock market indeed reignites corporate animal spirits and gets businesses back in investment (expansion) mode, such a scenario sets the stage for the mother of all bear markets.

I am exceedingly skeptical... I.e., I see virtually zero chance of businesses reengaging amid the uncertainty of global trade (and/or capital) wars, which are not likely to abate, particularly amid an ongoing bull market in stocks. Probably better if we crash and burn now and force better political governance in the process.

Problem is, the Fed will do everything humanly possible as the crashing and burning begins, and if, as Brigden points out, we go to negative interest rates, "that’s a sucking black hole that we’ll never get out of"…

Of course, as my Dad always said, "never is a very long time", but I agree, a negative interest rate regime is the last thing we want at this (or, frankly, at any) point!

The following, from Greenspan’s 2014 book, speaks (screams) to what we’re presently experiencing!

I'll allow the charts (click to enlarge) to speak for themselves.

Have a nice weekend!

Marty

Labor "Earnings" (payrolls, wages, hours) Growth Rolling Over

Global Leading Indicators Began Rolling Over in Early '18

Job Openings Rolling Over

Midwest Job Openings Plummet

Asian Demand Dropping Markedly

Ominous Gap Separating Consumer And Business Confidence

Smaller Credit Card Issuers Seeing Spike In Delinquencies

Bond Market Similarities To The 1930s

Home Furnishing Prices Spike Likely Due To Tariffs

Budget Deficit Under Trump

CFO Survey Year-Over-Year Change In Optimism

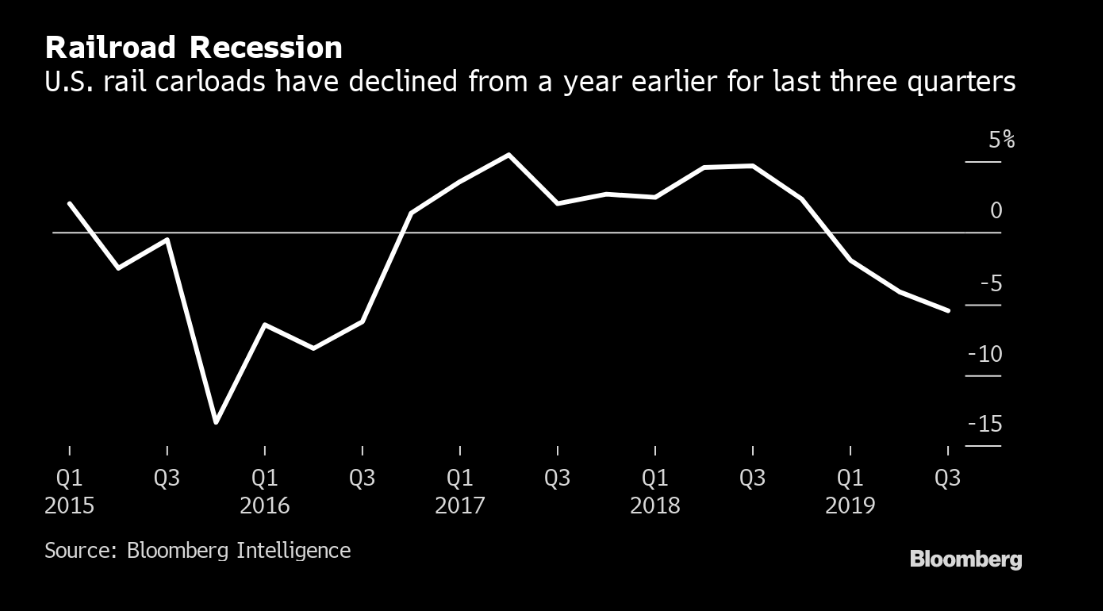

Rails In Recession

Futures Speculators Are Bearish On The Economy

ISM New Export Orders Exceedingly Low

Defensive Sector Equities Dominate Q3 Inflows

Riskier Issuers Increasingly Accounting For Bigger Share Of Leveraged Loan Mkt

Bifurcated Credit Markets

CEO Expectation At Recession-Level Low

Chinese Consumers' Debt Service Burden Rising

Aluminum Demand Slowing Globally

Incentives Saved Q3 Auto Sales

Q3 Commodity Performance Screams Slowdown

Companies (Buybacks) Are The Largest Buyers Of Stocks

Consumers Pessimistic On The Economy

Bespoke's 5 Fed Manufacturing Survey Outlook

S&P 500 Profit Margins History & S&P 500 Stock Index

S&P 500 Aggregate Earnings/Share & S&P 500 Stock Index

Record Share Buybacks In 2018

World Trade Volume Declining Rapidly

NFIB (Small Business Survey) Jobs Component Rolling Over

Buybacks And Dividends (More So Than Capital Investment) Consuming Corporate Profits

A side note, and one that I have been quite bullish on as a potential game-changer -- and one that I’ll definitely keep my eye on -- is 5G. Unfortunately, as we sit here today, this potentially revolutionary game-changer in terms of productivity gains and so on is likely to face notable headwinds amid such a polarized, populist and protectionist-minded, backdrop...

The problem I have with the central-banks-can-save-the-day narrative is that unless a Fed-juiced stock market indeed reignites corporate animal spirits and gets businesses back in investment (expansion) mode, such a scenario sets the stage for the mother of all bear markets.

I am exceedingly skeptical... I.e., I see virtually zero chance of businesses reengaging amid the uncertainty of global trade (and/or capital) wars, which are not likely to abate, particularly amid an ongoing bull market in stocks. Probably better if we crash and burn now and force better political governance in the process.

Problem is, the Fed will do everything humanly possible as the crashing and burning begins, and if, as Brigden points out, we go to negative interest rates, "that’s a sucking black hole that we’ll never get out of"…

Of course, as my Dad always said, "never is a very long time", but I agree, a negative interest rate regime is the last thing we want at this (or, frankly, at any) point!

The following, from Greenspan’s 2014 book, speaks (screams) to what we’re presently experiencing!

“Today, the political pressure on government officials to respond to every perceived shortcoming in economic performance has become overwhelming. I observed it build over my more than two-decade stretch in public office. Even if policy makers acknowledge that allowing market declines to exhaust themselves may indeed return markets to balance, there always exists some uncertainty of how long an unimpeded market decline will persist or how deep it will go. Accordingly, in recent years policy always has seemed biased toward short-term activism when, more often than not, allowing markets to rebalance and heal is the most prudent policy.

It has been my regrettable experience that the political response to policy makers’ actions heavily biases the policy makers toward catering to short-term benefits, largely disregarding long-term costs.”

Greenspan, Alan. The Map and the Territory 2.0 . Penguin Publishing Group.The following chart pack comes from a file I recently created and titled "Charts That Trouble Me" (these data are in addition to those we formally track in our macro index).

I'll allow the charts (click to enlarge) to speak for themselves.

Have a nice weekend!

Marty

Labor "Earnings" (payrolls, wages, hours) Growth Rolling Over

Global Leading Indicators Began Rolling Over in Early '18

Job Openings Rolling Over

Midwest Job Openings Plummet

Asian Demand Dropping Markedly

Ominous Gap Separating Consumer And Business Confidence

Smaller Credit Card Issuers Seeing Spike In Delinquencies

Bond Market Similarities To The 1930s

Home Furnishing Prices Spike Likely Due To Tariffs

Budget Deficit Under Trump

CFO Survey Year-Over-Year Change In Optimism

Rails In Recession

Futures Speculators Are Bearish On The Economy

ISM New Export Orders Exceedingly Low

Defensive Sector Equities Dominate Q3 Inflows

Riskier Issuers Increasingly Accounting For Bigger Share Of Leveraged Loan Mkt

Bifurcated Credit Markets

CEO Expectation At Recession-Level Low

Chinese Consumers' Debt Service Burden Rising

Aluminum Demand Slowing Globally

Incentives Saved Q3 Auto Sales

Q3 Commodity Performance Screams Slowdown

Companies (Buybacks) Are The Largest Buyers Of Stocks

Consumers Pessimistic On The Economy

Bespoke's 5 Fed Manufacturing Survey Outlook

S&P 500 Profit Margins History & S&P 500 Stock Index

S&P 500 Aggregate Earnings/Share & S&P 500 Stock Index

Record Share Buybacks In 2018

World Trade Volume Declining Rapidly

NFIB (Small Business Survey) Jobs Component Rolling Over

Buybacks And Dividends (More So Than Capital Investment) Consuming Corporate Profits

No comments:

Post a Comment