To stay on track each day I have a pre-market and post-market checklist of things to do. Some of the pre-market stuff typically hits my morning comment. The post-market stuff informs me as to the credit, equity, commodity and currency market dynamics of the day, as well as their prevailing trends. I also record any global economic data releases.

In terms of the credit market, up until this week stress therein had clearly (thanks to the Fed) been abating. In fact, while there are still splashes of red on this snapshot of last Thursday's look at credit, that's notably better color than, say, 6 weeks ago:

Here, however, is today's:

Suffice to say that conditions have deteriorated in the credit space over just the past week. Enough to make the stock market nervous? Well, based on how equities have traded of late, perhaps, but only at the margin. Fundamentally-speaking, is there enough going on in the credit market to question current stock market valuations? Oh, and how! But, as we've pointed out ad nauseam herein, stocks haven't been trading along with the fundamentals of late.

As for stock market internals today, well, the under the surface details confirm what the degree of today's selloff itself suggests, stocks were sold with passion today:

Volume was notably above average and breadth was the definition of bearish. The up/down volume for the NYSE was 109/7051. Advancers vs decliners for the S&P 500 was 1/504. Every single Dow component closed in the red. Nasdaq Comp decliners led advancers 15 to 1.

In terms of leadership, our top-5 core positions were UUP (dollar bull ETF), FXY (yen), GLD (gold), DBA (Ag commodities) and Verizon. UUP and FXY were the only positions closing up on the day. 12 of our 17 core positions outperformed the S&P 500.

Financial media suggest that today's selloff had to do with a spike in COVID-19 cases. While that may very well be the case, recall this from this Wednesday's evening note:

Our PWA Fear and Greed Index is, as of this morning, back in the red (net greed), albeit slightly (+12.5 [max greed is +100]), after reading max fear back at the March bottom.

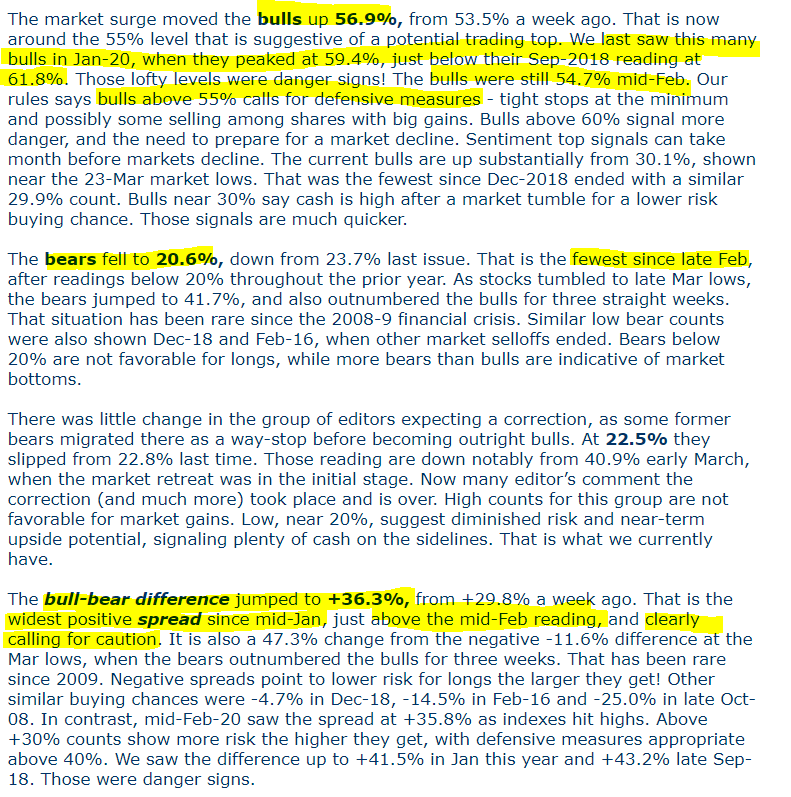

Two of its components -- adviser sentiment and the equity put/call ratio -- are currently sending huge warning signals.

Adviser Sentiment:

Click to enlarge...

The equity put/call ratio (white line) is virtually screaming "selloff" (yellow line S&P 500) -- now even lower vs the historic low it flashed at the February high:So, with or without a spike in COVID cases, the sustainability of the rally (may very well still be intact, mind you) off of the March low is, in our view, very much in question.

Click to enlarge...

As for today's data releases (there were few), they reflect what you'd expect given the current state of global economic affairs:

- 1.5 million Americans filed new unemployment claims last week, while 20.9 million remain on the rolls. Mind-boggling!

- French Non-Farm Payrolls down 2%

- Italian Industrial Production down 42.5% (YoY)

- South Korean Export Price Index down 8.2%

- South Korean Import Price Index down 12.8%

- New Zealand Business PMI 39.7 (below 50 denotes contraction)

- South African Manufacturing Production down 1.2%

- South African Mining Production down 47.3%

Bottom line with regard to the current global equity market setup; like I said this morning:

"Markets love unlimited money printing, until, that is, the economic consequences of a debt-filled bubble come home to roost.

There's much left to play out this go-round..."

No comments:

Post a Comment