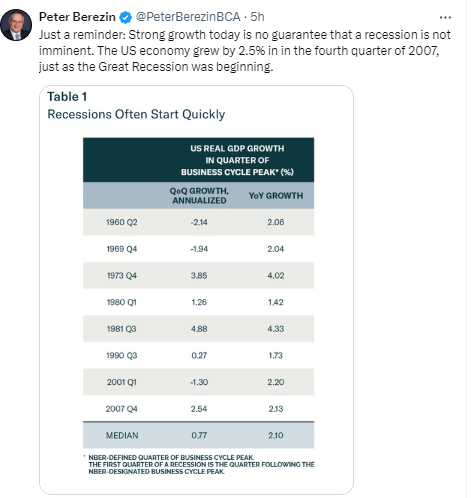

After whatever correction the next few days or weeks delivers (if any), I expect the data to weaken as we move further into Q3, with stocks possibly rallying on the prospects for a September Fed rate cut...

Of course seasonality has to be mentioned, as a Q3 rally would be bucking the long-term worse-quarter-of-the-year trend.

"I may as well just say it. Based on the present combination of extreme valuations, unfavorable and deteriorating market internals, and a rare preponderance of warning syndromes in weekly and now daily data, my impression is that the speculative market advance since 2009 ended last week.

Barring a wholesale shift in the quality of market internals, which are quickly going the wrong way, any further highs from these levels are likely to be minimal. In contrast, current valuation extremes imply potential downside risk for the S&P 500 on the order of 50-70% over the completion of this cycle."

"Emphatically, nothing in our investment discipline relies on a market peak, and every element of our discipline remains open to a change in market conditions that would encourage a more constructive outlook. We just don’t see those conditions at present."

And the following in bold will sound very familiar to clients, particularly those who've been with us through past market cycles... I.e., this is essentially how we approach our responsibilities as well:

As our long-term readers know, I try to avoid statements that sound like forecasts. Our investment discipline is not to forecast, but to identify – to align our outlook with prevailing, observable, measurable conditions. Given that the S&P 500 just set a record intra-day high of 5505.53 on Thursday of last week, suggesting that the bubble has peaked is extreme, even for me. Still, as I observed at the 2000 and 2007 peaks, we don’t know any other way to approach the market than to ask “What are the conditions now?” and “How have those conditions historically been resolved?” Then, as now, we had only one answer.

Taken as a whole – extreme valuations, divergent market internals, overextended market action, euphoric sentiment, tepid participation, deteriorating leadership, and other warning signs – the current set of market conditions provides no historical examples when stocks have followed with decent returns. Instead, the “nearest neighbors” are either major market peaks or extremes that preceded steep corrections.

In addition to the sheer depth and breadth of his excellent analyses, here's some history that vividly demonstrates why we should take John's opinions seriously:

With the market nearly 20% off its highs, it is rather easy to say that stocks are in a ‘bear market.’ However, this type of label is simply a snapshot and says nothing about future prospects for the market. The stock market is now fairly valued. We expect that many investors, particularly short sellers, will realize several months from now that they sold at wholesale. Reestablish a 100%, fully invested position.

-John P. Hussman, Monthly Market Letter, October 12, 1990

Over the following 25-year period, the annual total return of the S&P 500 averaged 10.1%

So yes, we believe that the crash risk of the market is extremely high. The short term, however, is unclear. Nothing in the market is certain, but we don’t know any other way to approach the market than to ask “What are the conditions now?” and “How have those conditions historically been resolved?” In this case, we have only one answer.

– John P. Hussman, Monthly Market Letter, March 7, 2000

Last week, we noted in our weekly market comment that the market has recruited enough ‘trend uniformity’ to shift the Market Climate to a favorable condition. As usual, we don’t forecast, we identify. Our view is not that stocks must advance, nor that the economy must expand. Rather, current conditions match those that have historically generated favorable market returns, on average.

– John P. Hussman, Monthly Market Letter, May 12, 2003

Given my general avoidance of forecasts, there are very few situations when I would state my views about the market as a “warning.” Unfortunately, in contrast to more general Market Climates that we observe from week to week, the current set of conditions provides no historical examples when stocks have followed with decent returns. Every single instance has been a disaster.

– John P. Hussman, Examine All Risk Exposures, October 15, 2007

Probably the best way to begin this comment is to reiterate that U.S. stocks are now undervalued. Last week, we also observed early indications of an improvement in the quality of market action, and an easing of the upward pressure on risk premiums. In 2000, we could confidently assert that stocks would most probably deliver negative total returns over the following 10-year period. Today, we can comfortably expect 8-10% total returns even without assuming any material increase in price-to-normalized-earnings multiples. Given a modest expansion in multiples, a passive investment in the S&P 500 can be expected to achieve total returns well in excess of 10% annually.

– John P. Hussman, Why Warren Buffett is Right (and why Nobody Cares), October 20, 2008

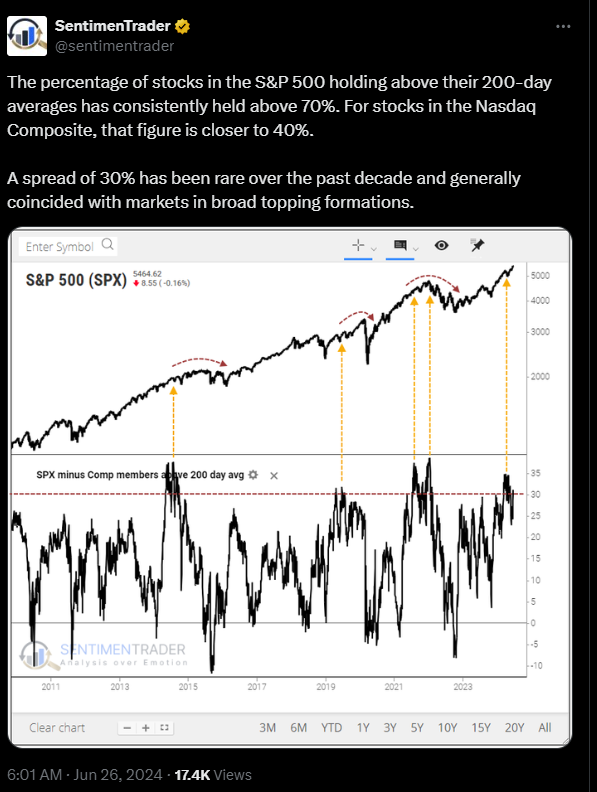

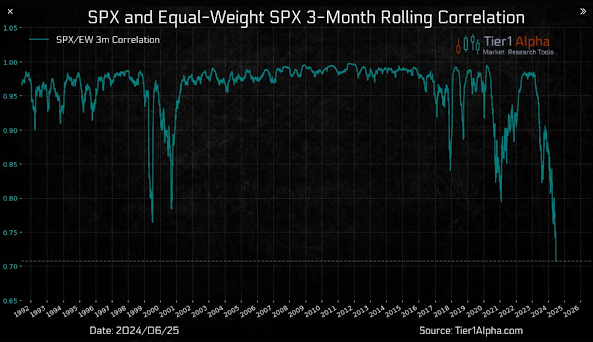

Never been there without recession:

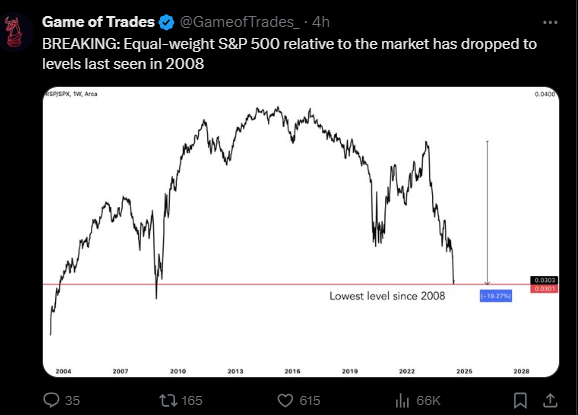

Not since the great recession:

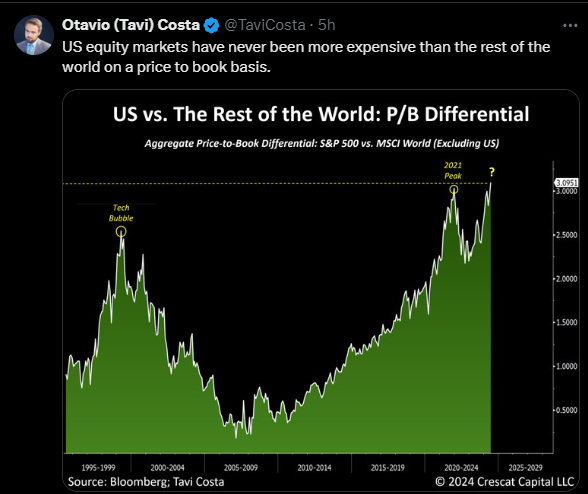

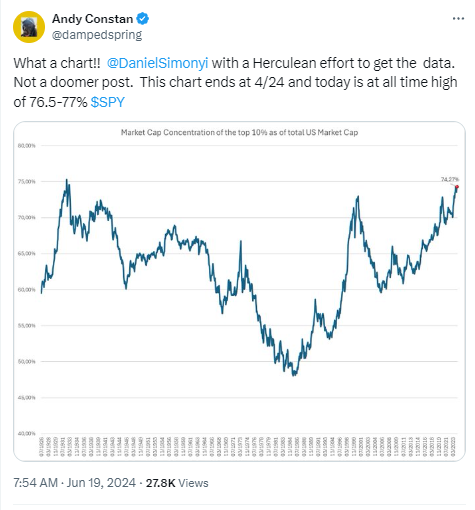

Most expensive, relative to the rest of the world, in history:

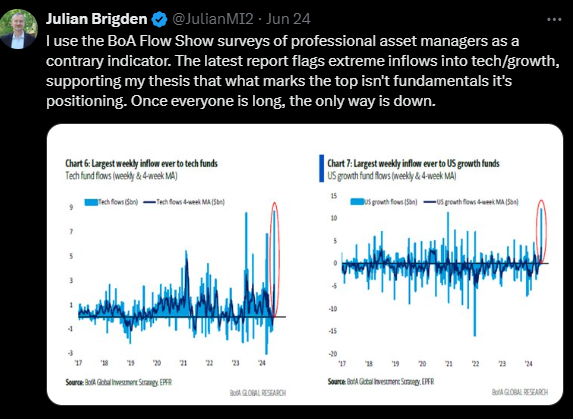

Yesterday I listened to one of the most insanely bullish on stocks podcasts I’ve heard in a very long time, if ever… It was by Goldman Sachs, and the guest was on their equity team, I believe “sales” was in his title…

I say “insane,” not because the bloke was bullish – there’s clearly a bullish narrative to appreciate (as always) right here – but because this guy was off the charts bullish, offering virtually zero room for compromise… His chief claim seemed to be that across virtually every class of investor, everyone was essentially all in… Although he did try to make a case that while fund manager cash is at a historic low, the sum total of all that cash was yet a very big number – anticipating that said cash was also there to find its way into the stock market.

Now, I can take this in so many directions, but I’ll start with the latter… The fact that the historically-low % of cash in the hands of fund managers amounts to a lot of money, is, in my humble view, a resoundingly irresponsible point to make when suggesting it provides potential oomph for stocks from here… I.e., it’s 100% relative: If, for example, one is sitting on 5% cash in a $20 million portfolio, that $1 million, while not a small amount of money, is not considered juice for additional stock purchases by the investor… It’s simply an albeit small % cash allocation; holding it simply for the sake of holding it... The portfolio, for all intents and purposes, is all in stocks already.

And breadth remains utterly horrific… Today, for example, the S&P 500 (cap weighted) was up roughly .40% – while 387 (nearly 4 out of 5) of its members closed in the red (with an average loss of 1.28%)… S&P 500 Equal Weight was down 0.69%, Dow was down 0.75%, Russell was down 0.33%... While the Nasdaq Comp rose 1.3%, with nearly 2 to 1 decliners over advancers.

Then we can get into valuations, yada yada, but we get the picture.

Bottom line: While indeed the current rally may have legs, the risk of ultimately giving back a year or three of gains is exceedingly high over the coming months.

Or, as Julien Brigden put it yesterday:

Nvidia’s prospects, and the equity market setup relative to AI:

In this morning’s roundtable, BCA’s Irene Trunkel made sense (to me) of Nvdia’s selloff and of the potential overall market setup related to AI:

“I’m not sure this is the end of the Nvda rally, whether we deem it rational or not, simply because there are still lots of people who believe in generative AI… I was comparing expenditures across the “Magnificent 7,” and what is interesting to me is that this whole industry is becoming like 5g and telecoms, because all of these companies are actually pushed into spending billions on generative AI… And if you think about it, what is the advantage for Google offering generative AI and then it offers the links when you do google search now; it costs billions and I really doubt that marginally it’ll seriously increase their advertising revenue… And same thing with Apple, I thought that what they presented at the conference was absolutely incremental.So this rally is, what, about a year and a half old? In 2001 the internet bubble rally started in ‘99, ended at the beginning of 2001, so it took a little bit longer… And that’s why unless something really puts the brakes on this, it would be hard to bet against, even though I consider this a bubble.”

So I think the question is that these companies are pushed into spending lots of money on something that potentially they don’t use, just because of the peer pressure… Just like telecoms had to spend on 5g networks, just like the Big 3 (automakers) had to spend on EVs, and channel all of their profits into this new venture.

And so I think that the big picture is business is pushed to spend on something that is not clear whether it will get the return, I think that this is something that imperils future profitability… I’m not sure that this revolutionary change is actually going to take place among companies that are spending billions now… I think that’s a long-term story.

I think that for now this rally could potentially continue because lots of people will see this as an opportunity to enter this trade, but if we have a recession or it becomes apparent that companies are spending and not making any money, that will put an end to this rally.

A strengthening setup, or a head fake?

S&P Global’s May PMIs signal either a sustainable resumption in US economic growth, or the pre-recession head-fake we presently suspect:

Manufacturing overall: 51.7

Services overall: 55.1

Manufacturing employment: 53.5

Services employment: 51.4

Manufacturing future output: 62.1 (although down from high 60s in May)

All the while, the Conference Board’s LEI (leading economic indicators) declined 0.5% in May, which marks 27 months of consecutive declines (a record)... The 6m/6m change has never been this low without signaling recession.

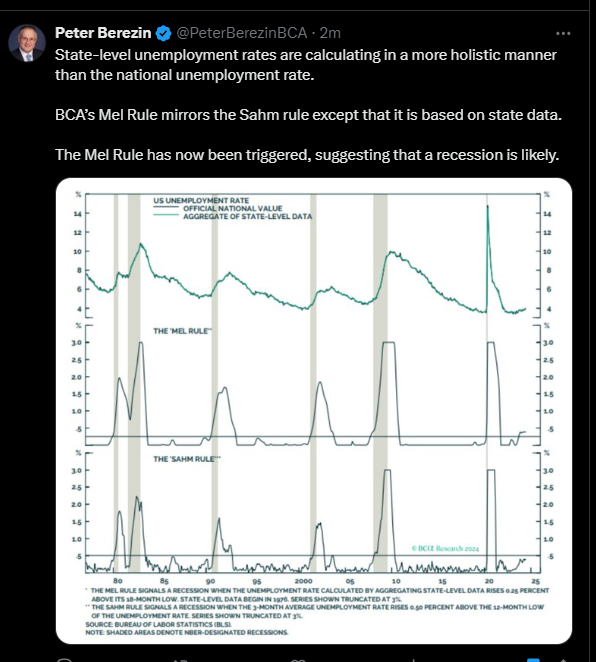

My observation as well (growth spiking just ahead of recession is not at all unusual):

No comments:

Post a Comment