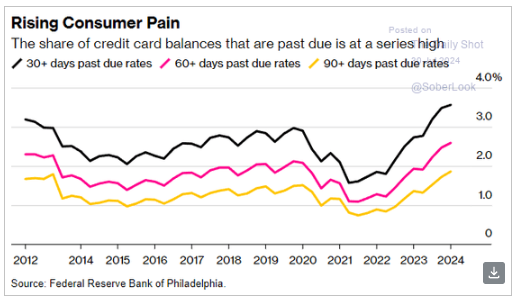

While those who don’t see recession looming (looking out 6-12 months) will cite the fact that the upper half of income earners are still spending quite healthily, and that their spending represents the lion’s share of US consumption, we should nevertheless take the latest credit data seriously.

I.e., while the below may indeed reflect the pain among those not in the upper 50% of income earners, it nevertheless speaks to the evolving state of the economy, and, in our view, should be viewed as a serious warning sign:

The latest consumer confidence readings confirm the rising stress:

However, the degree to which Americans continue to splurge "on luxuries" abroad says that the higher income half is more than hanging in there:

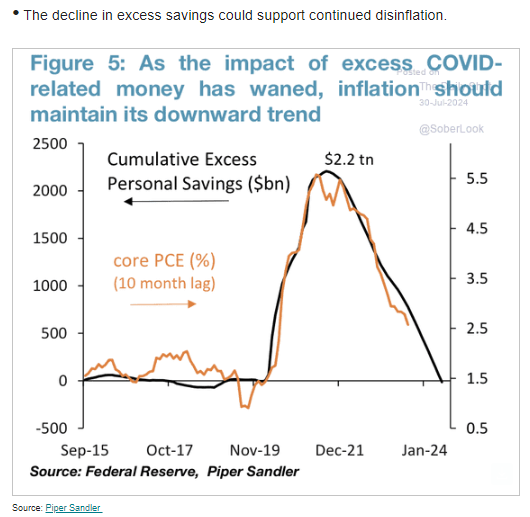

Inflation's Following Savings

Among the factors that made 2023 a massive miss for economists (the consensus was overwhelmingly forecasting recession [our base case as well btw]) was the misunderstanding, and/or miscalculation, of the amount of spendable “excess savings" (or “pandemic savings” if you will) that remained in people's pocketbooks.

Well, per the Fed (below), those savings are pretty much done working their way through the economy.

Now, as we’ve stressed ad nauseam, while there are indeed structural forces afoot that mean persistently higher long-term inflation over many years to come than folks grew accustomed to the past few decades, between here and there a slowing economy will indeed bring inflation down notably vs the 2021 peak… As inflation continues to cool, the prospects for significant easing of monetary policy will increase... We’ll indeed see what the Fed’s thinking at the conclusion of this week’s policy meeting Wednesday, and Chairman Powell’s press conference.

Markets may welcome strong hints that lower rates are coming, which will be justified if said slowing doesn’t result in outright recession... If it ultimately does -- still our base case -- stocks, for example, are presently dangerously overpriced.

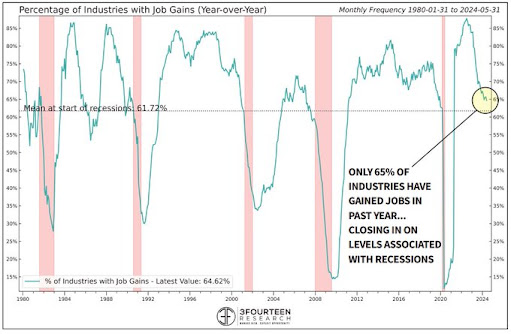

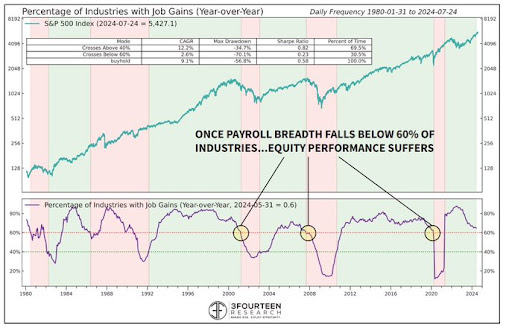

The Fed's Labor Market Focus

While sticky inflation, record stock market valuations, and, for example, strong Q2 GDP, etc., argue against Fed rate cuts anytime soon – which is the base case (no cuts yet, or nothing more than a token cut or two) for a few credible macro players – the following from Warren Pies is, in my view, a far more plausible near-term thesis on the whys and wherefores of monetary policy right here:

FED This week, expect Powell to focus on (negative) labor market momentum to justify a Sept cut. The percentage of industries growing jobs (YOY) has fallen below 65%. Average recession begins w/ this number just above 60%. @3F_Research

Historically, it's tough to reverse negative labor market momentum. Once industry breadth falls below 60%, it begins to negatively impact stocks.

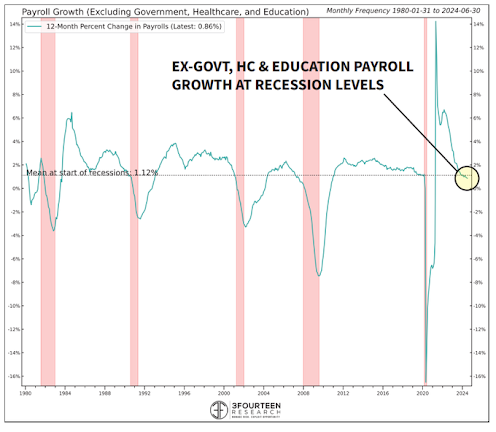

Ex-government, HC, and Education job growth is already below 1% (YOY)...this is a recessionary level historically.

None of this is normative. But, I see too many threads on Twitter that seem genuinely confused why the Fed would cut (NGDP is decent, inflation isn't back to target, FCI loose, etc). All fair points. But, the nervousness coming from the Fed stems from the (real) deterioration in labor momentum. For better or worse, this is the driving policy force. Cuts will begin in September. If UE ticks up even another .1%, then the conversation will shift to a 50 bp cut...

No comments:

Post a Comment