Among the many things that have that tech bubble smell, the present valuation gap between US equities and the rest of the world is like nothing we've seen since then.

US (SP500) price to sales ratio in white, Developed Foreign Markets orange, Emerging Markets blue... Red arrow at the tech bubble peak:

In the meantime, with regard to stocks, here's from the latest narrative in our monthly internal US equity market conditions report (our index presently scores a less than ideal -44.44):

US equities (cap-weighted indices in particular) produced positive results in June, which jibes with last month’s commentary, per below… While, at the same time, the underlying character continues to reflect dangerously abysmal breadth (SP Equal Weight, Russell 2k and Russell 2k Equal Weight were actually down on the month):

“Ironically, while my stated concern ultimately leads to consequently-lower equity prices, along the way to a harder-than-priced-in-landing, a notable rally in equities (classic “blowoff top” perhaps) is very much on the cards – as the economy/inflation cools.”

Button line for now: The likely equity market transition for the no-soft-landing scenario sees stocks flat to down as long as inflation remains elevated… Then stocks rally as the economy and, thus, inflation cools… Then stocks finally rollover when recession becomes reality… Then a fundamentally-sound buying opportunity presents itself.”

Inputs that showed improvement:

US Dollar (neutral to positive)

Interest Rates, Liquidity and Overall Financial Conditions (from neutral to positive)

Inputs that deteriorated:

Sentiment (from neutral to negative)

Inputs that remained bullish:

none

Inputs that remained bearish:

Valuation

Sector Leadership

Economic Conditions

SPX Technical Trends

Breadth

Inputs that remained neutral:

Fiscal Policy

And here's more from our internal market log:

Bill Blaine is making a lot of sense to me as I listen to this week’s Macrovoices podcast, here’s the opening dialog:

Erik: Joining me now is Bill Blain, editor of Blain's Morning Porridge. Bill, it's great to get you back on the show. Let's start with the usual suspects, boy, S&P 500, so many smart people on this program have made so many great arguments for why it shouldn't be just melting straight up. But boy, that's what it keeps doing.

Bill: Well, there is no stock market anymore, is there? All there is Nvidia and all the other stuff and Nvidia goes up 3% a day after falling 17% in the days before, it's moments like this when I'm always reminded that global markets are not clever, they are not intelligent. They are just voting machines, reflecting all the participants think, and if the participants don't have anything else to think about, and they make big mistakes, and they've got all the wrong things in their minds, then you get strange behaviors.

Of course, the markets are never completely wrong. So you've got to wonder what's behind it. And I rather suspect that it's a triumph of hope over reality. But you know, I believe in bonds, I've spent my whole career being a bond trader watching bonds and bond markets, there is truth, I always consider that stock markets just kind of go off in the back of them. If interest rates are too low, then stock markets get too enthusiastic. And I think stock markets have missed the fact that global interest rates are now normalized at much higher levels, and are not going to go back to the kind of nonsense 0% and 2% rates that we saw during the QE era. And I'm not sure stock markets realize that.

For the first time in a very long time, BCA’s global strategy team is bearish on the economy, and on stocks:

1. Overview

As was the case last month, MacroQuant’s super-leading indicators – indicators that not only lead the economy, but also lead financial markets – are flashing red.

MacroQuant can sometimes be too early in calling stock market tops. It began to sound the alarm on rising inflation in the spring of 2021, but it was not until the end of that year that investors (and the Fed) took notice.

This time around, the model is more relaxed about inflation risk but has become increasingly worried about recession risk. Simply put, the model does not buy into the soft-landing narrative. Accordingly, it is recommending that investors sell stocks and use the proceeds to buy long-duration government bonds (Chart 1).

Will the model be too early in calling the top in stocks, just as it was in 2021? Perhaps, but with the S&P 500 trading at a 48% premium to its net present value – the most overvalued it has been since August 2000 – there is too grave a risk of waiting for the music to stop (Chart 2).

Chart 1MacroQuant Recommends Selling Stocks And Buying Long-Duration Bonds

Chart 2

The S&P 500 Is More Overvalued Than At Any Time Since August 2000

I’m a bit less sanguine about the economy going forward than Unlimited Fund's Bob Elliott, but even his scenario doesn’t provide a favorable setup for equities going forward:

The Stronger for Longer outlook nailed the macro environment in 1H24, but macro dynamics and market pricing have clearly shifted. 2H24 will likely be dominated by disappointment from a Growing but Slowing economy. What it means for the economy and assets ahead.

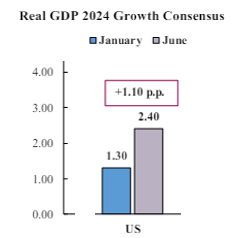

Coming into '24, expectations of US growth were soft, and the resulting upward shift in expectations helped support stocks and put a drag on bonds and short rates pricing in rapid cuts. But now, expectations for '24 growth are at 2.4%, which means ~3% in 2Q-4Q given 1Q GDP.

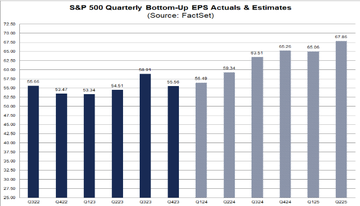

Further expectations of earnings growth at the S&P500 level are now for 17% y/y gains by 4Q24. That's a pretty notable pickup in contrast to the relatively flat earnings over the previous 7 quarters and high in context of an economy growing at 5-6% nominal at best.

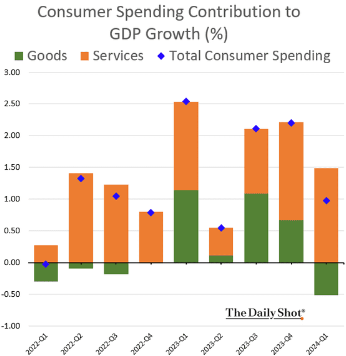

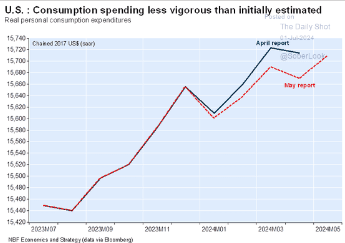

Those elevated expectations are coming at a time when its pretty clear that underlying US demand is starting to soften relative to those elevated expectations. Consumer spending contribution halved in 1Q and was revised down 60bps.

And there are signs that it has been softer since, and weaker than initially expected.

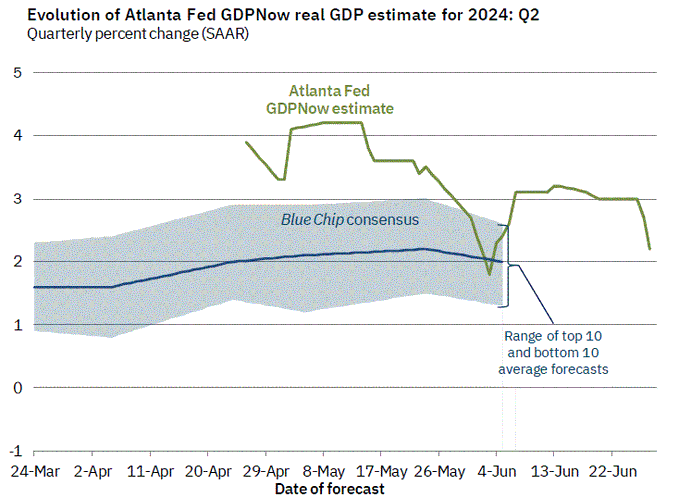

And all the 2q stats taken together suggest GDP growth closer to 2% for the 2Q, not the 3% needed to keep up with analysts expectations for the full year '24.

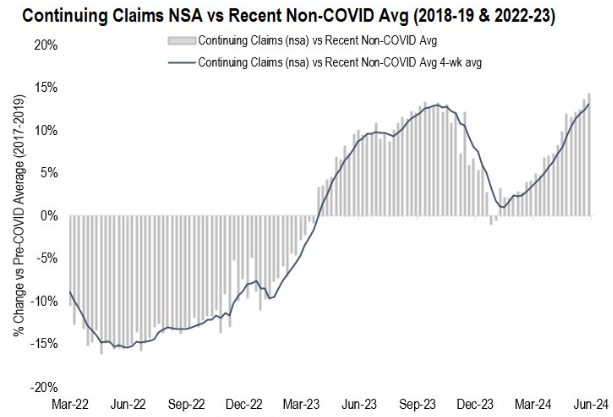

And the underlying strength in the labor markets which has been so critical to generate the income needed to pay for the expansion is showing some signs of softening, whether its a gradually rising UE rate, or timely continuing claims moving higher. h/t @Econ_Parker

Its going to be challenging to meet the current economist expectations for growth in '24 and the very high earnings expectations currently priced into stocks if this deceleration persists in the 2H. All of which is shaping up for a challenging dynamic for stocks ahead.

No comments:

Post a Comment