Update: The following content was posted yesterday for today's distribution... In the meantime, here's an entry to our internal log this morning:

Google (Alphabet) stock is getting slammed this morning on earnings comments that very much jibe with our concerns over the AI hype… They implied that patience will be needed when it comes to justifying the massive spending they and others are devoting to AI.

Like I said yesterday:“With regard to AI, so far it’s all about companies competing to see who can spend the most on it, while seeing virtually zero offsetting profitability gains yet emerging… They’ll likely come, but there’s little evidence that said profitability will emerge to offset the bottom line hits – which tend to roil perfectly-priced markets – that’ll show up amid the heavy AI spenders in coming quarterly earnings reports.”

Context

I can't emphasize enough how all the hoopla over all-time highs in US stocks needs some serious context.

Essentially, the extent to which a mere handful of stocks have done all the lifting is historic (and, by the way, historically-unhealthy).

Here's from the 2021 peak, nearly 3 years ago... Note that while the S&P 500 and Nasdaq 100 cap-weighted indices (white and purple) have done okay since then (well, actually, since last December), the same stocks equal-weighted have produced just barely positive results for the S&P (green) and slightly negative results for the Nasdaq (yellow):

The bull-bear spread jumped to +49.3%, from +46.9% last issue. That is just above the end of Mar-24 difference of +48.3% for one of the widest ever! Of course it holds in the elevated risk danger zone above 40%. After the Mar extreme stocks declined and the bull-bear spread contracted to +24.7%, lowering risk. That may happen again.

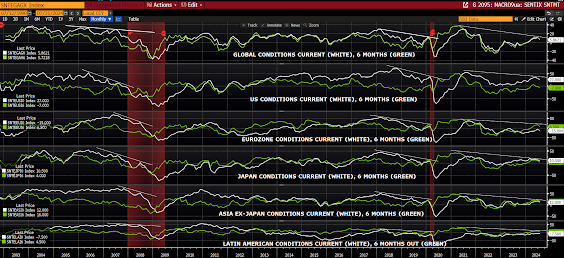

While Global Economic Sentiment Wanes

After a multi-month stretch of positive global sentiment, per Sentix, it’s presently rolling back over across the board, which jibes with the latest trends in global cyclical currencies, as well as our go-forward economic outlook:

The Ultimate Top Is Yet To Be Seen, However Caution Is More Than Warranted Right Here

Like ours, John Hussman's work points to extreme equity market valuations alongside generally unfavorable internals… Also like us, he nevertheless is not calling for the ultimate market top right here, just warning that the risk in the data says we could be getting close…

Here’s what turned out to be a most prescient, yet also telling in terms of how historically-negative signals can persist amid record high stock prices, quote from just before the tech bubble burst:

“Are we the only sane people on the planet? Let’s not be shy: regardless of short-term action, we ultimately expect the S&P 500 to fall by more than half, and the Nasdaq by two-thirds. Shorter term, we have another story. We can say without hesitation that this market looks similar in nearly every respect to the 1929, 1968 and 1972 tops, but the finer interpretation becomes less clear. Is the current market like October 1929, or is it more like April? If it’s like April, then we’ve got a few months of advances ahead of us. Is the current market like the November 1968 top? If so, the ‘new era’ stocks didn’t start crashing until about June of 1969. Once again, it makes a difference in the short term.

Frankly, we can’t say that this market is characterized only by the exact peaks of 1929, 1968 and 1972. In all three cases, there was a long and pronounced divergence between the broad market and the popular averages for months. The 1929 and 1972 instances were primarily blue-chip frenzies, while the late 1960’s instance was a performance stock frenzy. This time we have both, so we’ll probably see tops on two dates – one in the S&P and one in the Nasdaq. The difficult part of all this is the short term. I have no answer for that, except that in each prior instance, every scrap of short-term gain was wiped out in the eventual downturn.

A final note, I don’t write like this because I want to go ‘on the record’ before a plunge. I write like this because I know the terrible financial difficulty and utter shock that investors felt following declines which originated in similar conditions. Some of my more seasoned subscribers also lived through the 1969-70 and 1973-74 plunges, and have related the pain of buying respectable stocks on a 20-30% dip, only to watch their portfolio cut in half from there. When people watch the Nasdaq, there is a real pressure to chase performance. It can really seem like defensiveness is an enemy, and speculation is a friend. And again, the same was true in the late 1960’s, when McGeorge Bundy of the Ford Foundation directed the managers of university endowments to become more aggressive: ‘We have the preliminary impression that over the long run, caution has cost our colleges and universities much more than imprudence or excessive risk-taking’. In the plunge that followed, that preliminary impression turned out to be horribly incorrect.”

– John P. Hussman, Ph.D., February 9, 2000

"The bubble peak a few weeks later was followed by a 50% loss in the S&P 500 Index, a 78% loss in the Nasdaq Composite Index, and an 83% loss in the tech-heavy Nasdaq 100 Index."And another, just ahead of the ‘08 bear market:

“I generally try to avoid near term forecasts of market direction. The predictable amount of market return over a one-week period is overwhelmed by short-term volatility, and forecasts based on longer time horizons implicitly assume that the Market Climate we identify will not change over the forecast period. Given my general avoidance of forecasts, there are very few situations when I would state my views about the market as a ‘warning.’ Unfortunately, in contrast to more general Market Climates that we observe from week to week, the current set of conditions provides no historical examples when stocks have followed with decent returns. Every single instance has been a disaster. We can’t rule out the possibility that investors will adopt a fresh willingness to speculate (which we would observe through an improvement in market internals). Such speculation might prolong the current advance modestly, but even this would not substantially alter the risks that have ultimately been associated with overvalued, overbought, overbullish conditions.”

– John P. Hussman, Ph.D., Warning – Examine All Risk Exposures, October 15, 2007

Conflicting Bullish Narratives Are ALL Priced In -- at the same time!

One might argue that, up until last week’s selloff, recent equity market gains were reflecting a Trump victory in November, bringing with it corporate-friendly, fiscally-stimulative policy… Previous to that point, one could argue that the market was at least partly influenced by the pricing in of multiple fed rate cuts beginning in September… Ultimately, though, the gains of the past year -- evidenced by how incredibly concentrated they were (a mere handful of stocks did virtually all of the lifting) -- were hugely based on all that AI promises in the months/years to come.

Thing is, the market, as we sit here today, is now pricing in all of the above playing out in essentially perfect form, and in perfect unison.

Well, for one, if indeed a Trump win brings what the market has priced in, it’ll almost certainly have to un-price multiple fed rate cuts going forward – as an economy fueled by tax cuts and other potentially-stimulative (read inflationary) initiatives doesn’t lend itself to accommodative Fed policy.

With regard to AI, so far it’s all about companies competing to see who can spend the most on it, while seeing virtually zero offsetting profitability gains yet emerging… They’ll likely come, but there’s little evidence that said profitability will emerge to offset bottom line hits – which tend to roil perfectly-priced markets – that’ll show up amid the heavy AI spenders in coming quarterly earnings reports.

Bob Elliott did a nice job emphasizing the above:

Buying stocks today is a bid priced at the best possible outcome of: * AI support to investment, growth & margins * Trump election & corporate favorable policies * Fed starting a significant cutting cycle. A near implausible pricing of perfection at today's levels.

The AI story has been a key driver of equity market strength for roughly a year, and at this point has largely priced in a likely implausible combination of extremely high investment, economic growth, and margin expansion from AI.

The benefits to S&P500 companies from rising AI-related spending and increased economy-wide productivity are modest even in an extremely optimistic case.

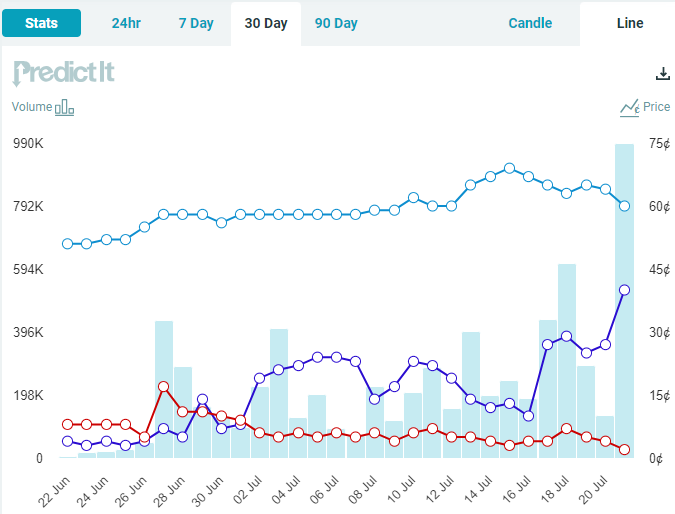

Trump's increasing expectations of victory added to the stock rise in recent weeks, reflecting an extremely high probability of full control and implementation of corporate friendly policy. But with the Biden drop out, traded odds that peaked at >70% are falling thru 60%:

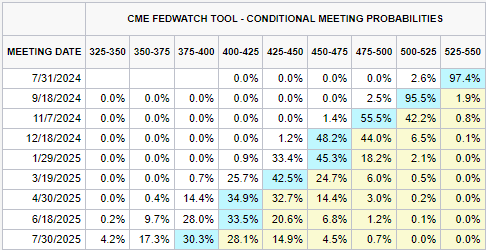

Adding further fuel to the equity rally in recent weeks has been a shift to expectations of large Fed cuts coming ahead. Now pricing in with certainty 3 cuts this year, and a cut nearly every meeting post-Sept, just as US economic conditions are showing improvement.

The challenge with trading this period in stocks with any sort of prudence is that there is no obvious bubble, certainly akin to the tech bubble of the past. Instead each of these fundamentals could easily be taken as good reason for why stocks should press higher.

The challenge is that when extraordinary expectations build not just in one area, but across a range of different beneficial themes, the aperture for meeting all those expectations that justifies the current prices shrinks significantly.

It's not certain which of those different themes will not hit, but all three look to be pricing in pretty extraordinary outcomes, and an almost implausible set of conditions where all of them happen together. For instance aggressive easing during an expected growth boom.

Getting *additional* rallies will require even better outcomes than what is currently priced in across all these factors. That is an even bigger AI boom, Fed cuts to <350bps by next summer, or even more corporate friendly Trump policies.

Such high expectations almost inevitably lead to disappointment. It looks likely that by the end of the year markets will look back and realize that the summer bid on stocks priced in a series of outcomes together that couldn't ultimately be met together.

No comments:

Post a Comment