Small Caps Rally!!!

The action over the past week in the equity market has been extraordinary… Well, okay, I’ll just say it’s been unusual (at least seemingly, until you scroll further), to put it mildly.

It certainly bolsters the bull’s narrative that this historically-bifurcated market (the 10 biggest SP500 stocks doing ~80% of the year-to-date heavy lifting, the remainder utterly languishing) will be remedied via the rest of the market playing catch up.

While that narrative is of course plausible, it, alas, looks too much (for comfort) like the late-cycle pattern typical of the lead-ins to notable market breakdowns… The operative words there being “late-cycle.”

Make no mistake, I’d be a raging bull on small caps if we were in the early stages of the next cycle… Simply put, that’s just not where we sit right here.

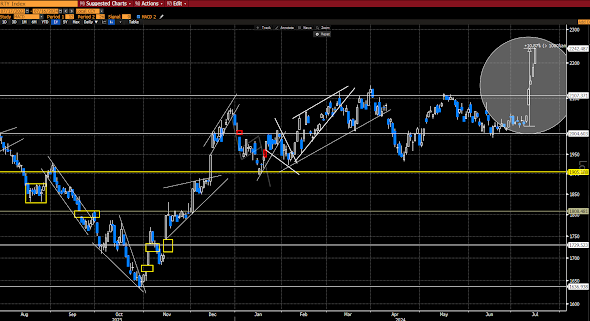

Cases in point involving the Russell 2000 Index.

Here we are today, witnessing a remarkable 11% spike over just the past week:

And here we were just over 3 years ago, experiencing a 9% surge one week before the 2021 top… Which was followed by a 33% collapse by mid-June 2022, then a retest of the low in mid-October:

Here’s a look at the mid-2008 18% surge that occurred over just 30 days, then a retest of the top 1 month later, only to culminate in a 55% collapse that bottomed in March 2009.

And here's that breathtaking 51% 4+-month rally ending right at the 2000 peak, only to then give way to a 47% collapse, which took back all of that previously rally, plus an additional 20%:

So, again, while we’ll remain 100% open to all possibilities, we simply can’t lose sight of where we sit in the current cycle!

Retail Sales Surprise

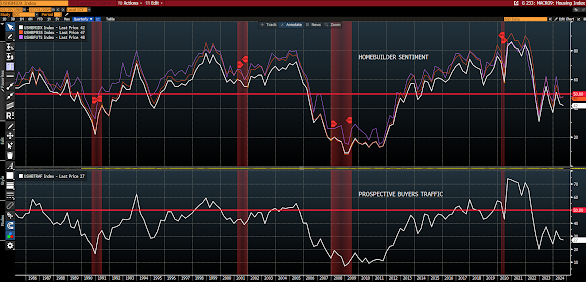

US retail sales surprised to the upside in June… Indeed, based on what’s being reported in retailer earnings calls, consumer sentiment, and, as of this morning, homebuilder sentiment, etc., an upside surprise was not on my radar… That said, the upper 50% of income earners are the heavy lifters when it comes to consumption… I chatted with a travel agent friend yesterday, and the vacation business to not-cheap destinations is booming… Clearly, the bottom half is suffering, while the top half continues to very much enjoy life.

That last line -- in today’s growingly populist world -- is a simmering political problem… And the policy remedies to wealth and income inequality lie on the fiscal side, and are structurally inflationary, to put in mildly.

Now, with regard to June’s survey, Dave Rosenberg has a different take:

David Rosenberg

@EconguyRosie

"If you were rubbing your eyes as I was over that retail sales report, I think I found the answer. A very generous seasonal adjustment factor was at play. The raw NSA data actually showed retail sales plunging -5.6% MoM in June, the worst drubbing in a decade and tied for the steepest plunge since the series began in 1992! Lies, damned lies, and statistics."

AI Priced for Perfection!

Bob Elliott does a nice job breaking down how optimistically priced the AI trade is right here:

Emphasis mine…

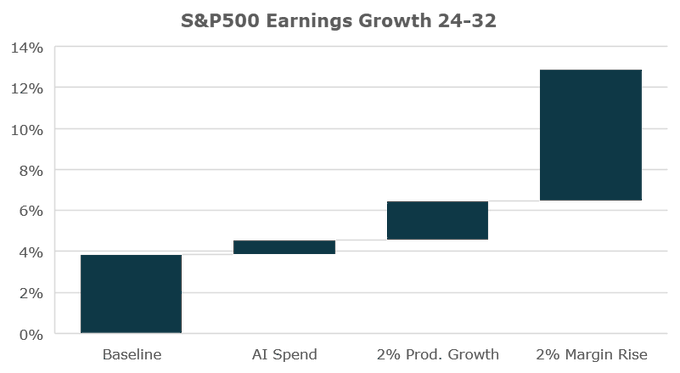

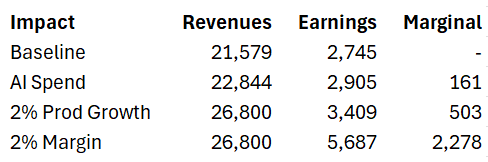

Taken together even under a boom in AI-related spend and a surge in productivity, it's a pretty marginal impact, not one that is game changing. That magnitude of this is already likely priced in. Probably was fully priced last year during the summer of the AI "boom".

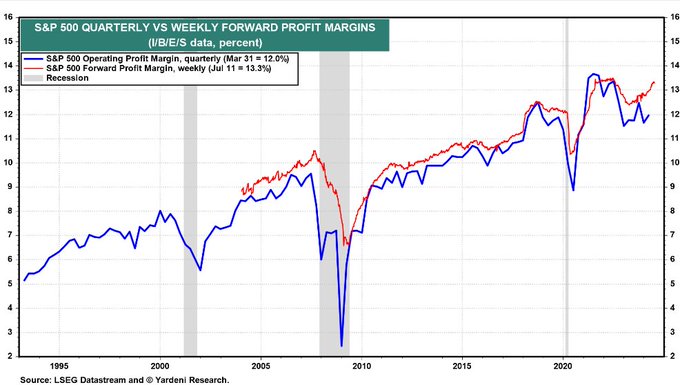

To get something that is at all in the ballpark of what the true techno-optimists claim, it's going to have to come through a surge in margins that pairs with the other pieces. And of course margins are already at secular highs and expected to rise further.

The tricky thing with rising margins is that it doesn't come from thin air. Since one sector's income is another's spending to get margin expansion (which is largely just labor paid less relative to revenue) you are gonna need a different sector to dissave on an ongoing basis.

Let's say we add a 1% margin increase into the mix *per year* in addition to the other impacts mentioned above. Then you start to get to something that looks closer akin to the mid-double digit earnings growth ahead proposed by the techno-optimist set.

And that would add an incremental 2.3tln in earnings, bringing the total to roughly 3tln more earnings in 2032 relative to the baseline expectation.

Even under those extraordinary assumptions, at 20x multiples, you are only talking about a doubling of stock market if fully priced in today assuming no discounting of any kind, a big chunk of which has been priced in over the last 12-18m already.

From a macro fundamentals perspective, achieving this level of margin expansion would not only be elevated in comparison to history, but would require a different sector of the economy to dissave at an ongoing rate 5% of GDP pace below its current level.

Meaning some combination of households, a share of businesses, or the government deficit would have to combine to offset the extraordinary margins of the corporate sector. It could happen, but it would require an extraordinary further secular shift to corporations from labor.

Believing that a surge in stock prices is justified as a result of AI impact on the economy and businesses requires pretty extraordinary assumptions around investment, productivity growth, and margin expansion, and shift from labor to corporations.

At this point current valuations and expectations are already reflecting a very high probability of this extraordinary combination of future outcomes comes together. Most likely investors at these prices will be disappointed over the long-term as they don't come to fruition.

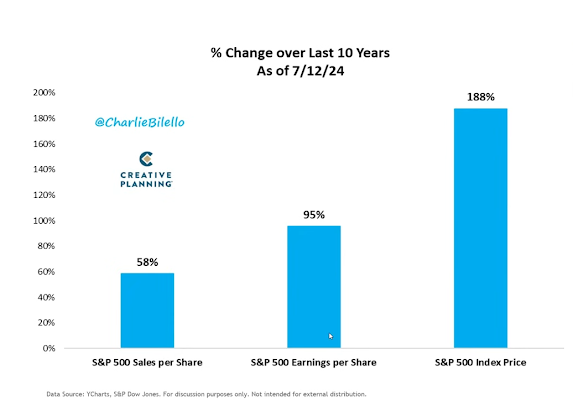

More On Market Fundamentals vs Price Action

Per Charlie Bilello, while the fundamentals (sales and earnings per share) have improved the past 10 years, stock prices themselves have dwarfed them… I.e., folks expect earnings to accelerate even further/faster in the months to come… That’s a most-ambitious outlook given the macro backdrop:

On the Yen

Peter Boockvar on the yen this morning… Again, I’m bullish on a 1-2 year horizon, and bearish on the dollar during the next cycle (after the next recession):

“When a major developed country's currency trades at nearly a 40 yr low against the US dollar, it is not just a talking point for Wall Street. It has real world implications for that country. We keep talking about Japan and the yen and the damage a weak currency has on their standard of living as the cost of imports rises sharply and wage growth is still not keeping up with inflation. I'll add another problem for Japan that the NY Times business section pointed out over the weekend. "Plunging Yen Takes Toll on Military." The article said "The government has slashed orders for aircraft, and officials warn that further cuts may be imminent. Japan buys much of its military equipment from American companies, in transactions done in dollars. The government's purchasing power has been drastically eroded by the yen's diminishing value."

Tobias Harris has a Substack on Japan and is an expert on the dynamics there. He wrote on Friday, "Dissatisfaction with the yen is present throughout the economy. Kobayashi Ken, the head of the Japanese Chamber of Commerce and Industry, which represents small and medium sized enterprises, earlier this month called on the government and BoJ to adopt FX policies that take the struggles of SMEs into consideration. Meanwhile, Niinami Takeshi, chairman of the business federation Keizai Doyukai, somewhat unusually called on Friday for a rate hike to provide relief from the weak yen."

Also, "The rising cost of imported goods has led to a mood of despair on Japan's opinion pages, as editorial writers and experts lament Japan's relative 'impoverishment' and decline."

Bottom line, expect a rate hike and a large cut to QE at the end of the month from the BoJ. The yen is down a touch today after the sharp rally last Thursday and Friday.”

No comments:

Post a Comment