Highlights from our internal notes:

9/30/2024

Despite the notable improvement in our own macro index, the global liquidity setup (see below), etc. (i.e., recession risk has indeed abated a bit of late), we need to be very cognizant – as I’ve illustrated in recent video commentaries – of the fact that it is the norm to get a positive spike in the data just before recession ensues.Totem Macro’s Whitney Baker (she’s an exceptional analyst, btw) pointed that out last week, along with the factors that she sees pointing to recession.

“Sure - bear in mind trailing data looks the strongest right before a recession. Forward looking outcomes are dictated by the sustainability of income growth and credit flows.

So in that vein here's what's pointing to a recession:- job growth has approached 0% as it always does pre-recessionIn short - financing flows (money, credit and income) have all slowed pretty dramatically, and now spending is slowing across sectors in both real and nominal terms, while deflationary demand shocks from China are hitting the rest of the world and choking off their nascent recoveries all at the same time.

- HH employment income growth down to 3%, essentially break-even vs. inflation leaving 0 real growth

- complete timely collapse in consumer confidence current conditions (reflects lack of job growth and slowing income)

- collapse in jobs plentiful relative to hard to get (reliably precedes every recession)

- large decline in US credit creation across HH and NFC sectors

- large (c.2.5ppts GDP) fiscal drag YTD despite still large deficit in level terms

- deflationary price action in rates market

- deflationary data especially in September, everywhere, globally - acute collapses across the board

- collapsing PMIs both manuf and services everywhere globally, especially new orders, export orders, and employment...especially in September when the global deflationary shock from Chinese demand collapse was expected to hit and is hitting as expected

- action in commodity markets

- simultaneous contraction in money printing in all jurisdictions at the same time, for first time since GFC

- easing always happens at this point in the cycle, and is always too late to prevent/counteract the recessionary income/spending declines already in place...start of rate cuts more a harbinger of recession than deliverance from it

-magnitude of priced in cuts recessionary, and corroborated by the real and price data globally

- China stimulus is window-dressing, and not remotely of the size or type needed to counteract property collapse and deflationary debt spiral...more aimed at juicing the equity market than anything real

- US unemployment rate trending up as normal pre-recession

- US NFIB earnings trends - deep in recession territory

- yield curve disinversion, reliable indicator of recession either leading or coincident

- credit collapse in China - the largest contributor to global credit creation this cycle by far, now gone and payback occurring for the unproductive debts taken on.

Stimulus will follow - correct there - but not for a little while, and the stimulus follows the onset of recession, especially because, in this cycle, there's a highly fraught US change in administration in the meantime.”

—------------------------------------------

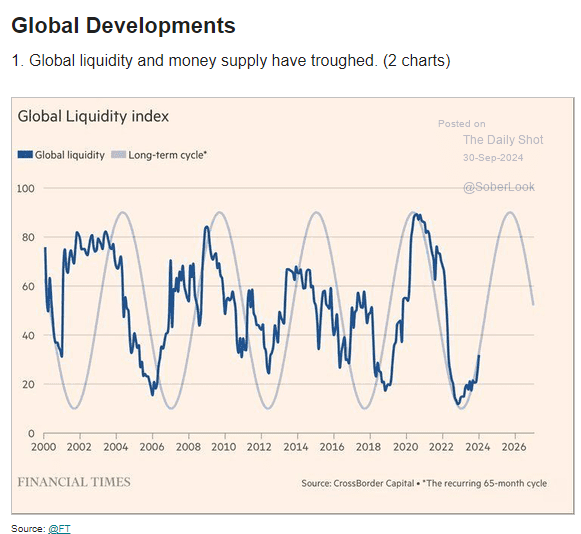

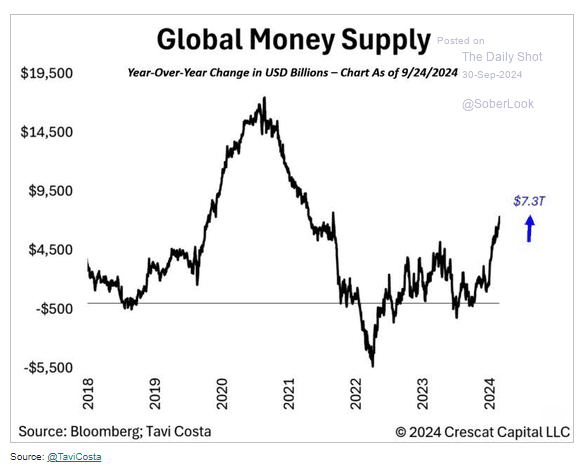

More liquidity charts out this morning; this is not bearish for asset prices!

9/29/2024

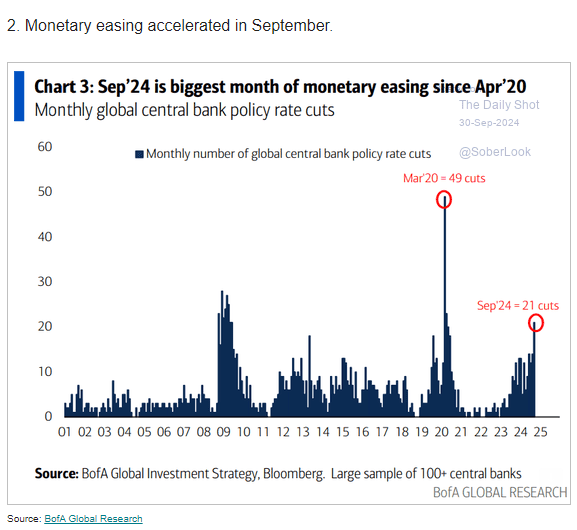

I’m noticing this as well:

9/26/2024

China bears are falling all over themselves to downplay this week's moves!! All very smart people (the ones we listen to), all may be correct, but I sense an air of desperation (to be proven correct) among them.

I'm currently thinking about the theory of reflexivity, and the notion that markets (expressing participants' views) can influence economic results (vs conventional wisdom's opposite view)... I.e., markets indeed play an active role, potentially influencing the very earnings flows (for example) they are believed to simply reflect... In other words, perceptions (discounted by markets) can indeed be more than simply a reflection of perceived reality, they can actually inspire actions that alter reality in a way that jibes with the perception.It's been my experience/observation that perception effecting, or altering, reality, indeed explains (at least to me) phenomena at times, but not always.

In terms of China, and how low it's gone, and the political incentive/necessity to perhaps finally do whatever's needed (serious stimulus from the world's 2nd largest economy) to reverse the trend; if you get a global buy-in, reflected in markets and engendering animal spirits, then suddenly recession odds diminish on that 6-12 month outlook.

Not saying this has suddenly become our base case, but it indeed bears watching.

No comments:

Post a Comment