Briefly on gold:

Suffice to say that gold resting at all time highs amid rising long-term treasury yields, and, not to mention, a strengthening dollar isn’t what you’d call intuitive.

So, what gives?

Three possibilities come to mind:

Gold is reflecting underlying economic weakness and, thus, the prospects for recession and/or exceptionally-easy monetary policy going forward.

Gold is the shiny thing foreign central banks like – and are therefore bidding up – in lieu of the US greenback these days.

Gold is forecasting a stretch of negative real interest rates in the years to come – resulting from the need to fund massive budget deficits, alongside the rolling over of trillions in low interest debt as far as the eye can see. Virtually demanding that the Fed be the buyer of first and last-resort for treasuries, as they’ll need to quell otherwise rising yields amid high US debt issuance and what are now notably structural inflation forces far into our future… It’s called “yield curve control (YCC)”

So, suffice to say that possibilities 1 and/or 2 are very plausible, all things considered… Whether markets are as forward-looking as #3 proposes, I dunno… But the likelihood that YCC is in our not-too-distant future is, well, let’s just say, not small!

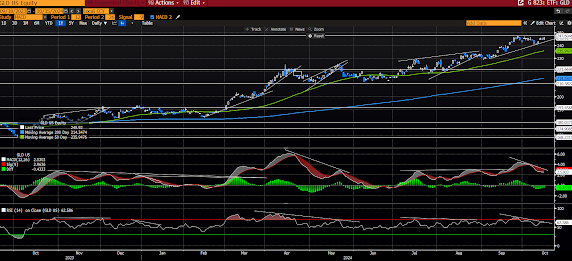

Now, for the every-tick-watcher among you, I'll add that the obvious (i.e., gold remaining a long-term core position for us), notwithstanding, short-term it’s looking toppy, technically-speaking:

On the current equity market setup:

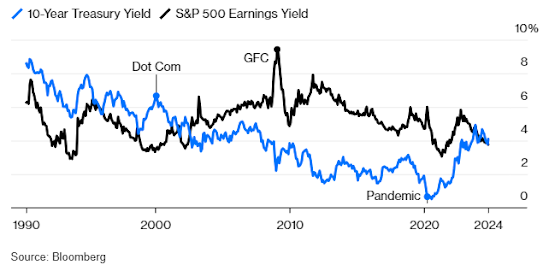

Bloomberg’s John Authers points to the relationship between 10-year treasury yields and equities' earnings yields to imply that it may be time to “get the heck out of stocks.”

“A Market Tipping Point

For the first time in 22 years, bonds are yielding more than stocks

Big gaps between the two measures are unusual. When in stocks’ favor, they signaled historic buying opportunities (as in early 2009 when the worst phase of the GFC was coming to an end, and again during the 2020 pandemic lockdowns). The last big gap in Treasuries’ favor, in early 2000, signaled correctly that it was time to get the heck out of stocks.”

And while I indeed sympathize with the notion that US stocks are, for a number of reasons, in a precarious spot right here, we should note that virtually the whole period between 1990 and the early-2000s featured that (treasury yield higher than SP500 earnings yield) dynamic… Nevertheless, this just adds to an abundance of evidence that, at a minimum, says current conditions do not remotely possess the characteristics of the beginning of a sustainable long-term up move in equities.

Like Jeremy Grantham (HT John Hussman) recently pointed out:

“We have totally full employment, totally wonderful profit margins. All the things you would not want to start a bull market from. This is where you start bear markets from. Great bull markets start with exactly the opposite.”

Not to say that full employment and “wonderful” profit margins are anything to complain about, it’s just that, for me – when I consider present valuations, the fact that we are way late-cycle (in our humble view), and that at least the soft data say the labor market is showing signs of weakness – well, I suspect that we are indeed flirting with a dangerously overextended market… Call it the overtime innings, if you will.

Now, that said, it would not surprise me in the least to see the stock market melt yet higher over the coming few months, as seasonality (flows, etc.) – and, not to mention, entering earnings season amid the lowest expectations in years – are very much in its favor… I.e., the ball game is still on folks... With, of course, not-small odds of a not-small spike in election-driven volatility as it plays out.

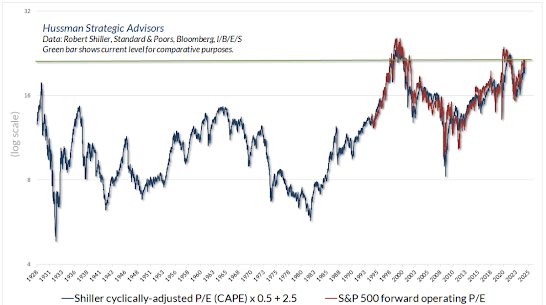

Speaking of John Hussman, he — like few, if any, others — has done the work on long-term returns for stocks based on starting valuation levels… Here’s where his analysis currently has us, on a 10-year go-forward horizon:

Even if one accepts analyst estimates of year-ahead S&P 500 operating earnings at face value, current valuations are at rare extremes. Since the price/earnings ratio on forward operating earnings has only been popular since the 1990’s, investors often overestimate what “normal” valuations are. One can get a better sense by comparing the forward P/E with Robert Shiller’s cyclically-adjusted P/E (CAPE), which has a far longer history. The green horizontal line shows the current extreme for comparative purposes. In the available data since the 1980’s, the current price/forward operating P/E is associated with subsequent 10-year average S&P 500 nominal total returns between -2% to 3% annually.

The following from the close to his latest monthly market analysis resonates with me:

“What will matter from here is full-cycle discipline, flexibility, and mindfulness of market conditions as they change. Unfortunately, those are the last things investors have on their minds. Instead, investors have become convinced that it is enough to buy and hold stocks with no thought about price, valuation, or the relationship between market conditions and market outcomes. Investors seem to imagine that expected returns will simply mirror average historical returns, completely ignoring the valuations that were responsible for those historical averages.”

Sadly – investors “convinced that it is enough to buy and hold stocks with no thought about price, valuation, or the relationship between market conditions and market outcomes” – is the thinking that immediately precedes major market tops (has to, virtually by definition).

But of course that says little, if anything, about precisely when those tops will occur (I.e., that thinking can persist, and prevail, for a long time)… It’s just that – amid historically-high valuations and sketchy market internals – the risk that it’ll be sooner than later is too high to ignore, or, let’s say, too high to not account for in one’s investment strategy.

Stay tuned...

No comments:

Post a Comment