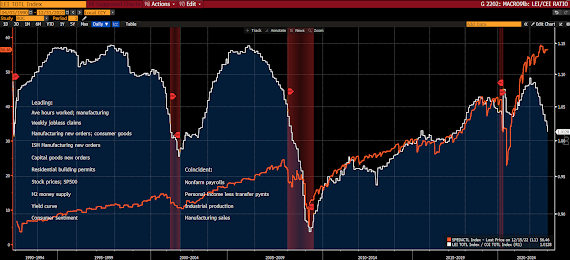

Now, apparently, assuming the above statement captures reality, the market appears to be living in, let's say, a bit of Lalaland right here -- in that corporate earnings projections, the orange line in the chart below, don't remotely reflect the prospects for the data (economy) rolling over, as illustrated by the white line (Leading Economic Indicators/Coincident Economic Indicators ratio)... I.e., the market sees earnings holding up just fine, amid a macro setup that says they're clearly in jeopardy... Hmm...:

With regard to the exceptionally-strong upside reaction to yesterday's Fed action, and, so far, to today's ECB action, keep in mind that futures speculators were substantially short global equities heading into the week... I.e., they (yours truly included, btw) expected far more hawkishness out of central bankers than what was delivered... Hence, and make no mistake, a not-small part of the impressive rally is simply the unwinding of significant short interest... Like I said Monday:

"...the bears are still sticking their necks out there -- risking getting their heads handed to them if indeed the Fed delivers a dovish message... I.e., that "huge short-covering if they come in dovish," will serve to add a not-small upside boost to stocks..."

Now, thinking beyond short-covering rallies, yada yada, Economist/Macro Strategist Peter Boockvar pulls no punches in this snippet from a bit of rant this week:

"Some in the mkts think that we're just going back to the days of '21 & prior where inflation is going to magically & quickly go back to 1-2%, the Fed after hiking rates will soon cut them sharply, the monetary fantasyland that once existed will come back, and the temporary moderation off record high profit margins will be temporary.

No, we are not going back anytime soon to that period of paradise. It's time to use a different investing playbook from the one used over the past decade.

The world has changed, the macro environment is different, cheap labor out of China is over, blue collar workers have wage leverage they haven't had in decades, just in time inventory is dead, big cap tech just can't grow their businesses as fast as they once did, central banks don't want to lose this fight against inflation and thus rates will stay high for a while, QT will continue on and just maybe the idea of NIRP and ZIRP are gone forever."

In general, as clients and regular readers know, we sympathize… Although I do believe that the Fed is very capable of cutting rates soon after they stop hiking… In fact, in a swift/deep recession scenario, I’d bet on it.

Otherwise, yes, the world, or the regime, as we like to say, has indeed changed, calling for a notably different investment playbook going forward.

As I’ve expressed herein, we think the longer-term macro setups are very clear, and VERY investable, once the current setup (bear market/likely recession) plays itself out.

January was amazing for stocks, surprised me for sure! Interestingly, some of January’s best performers were some of last year’s most deserving disasters... Question being, have their prospects improved enough to justify such an impressive snap back?

That’s a very good question?!?

Asian stocks were mostly green overnight, with 10 of the 16 markets we track closed higher.

Europe's in rally mode so far this morning, with 17 of the 19 bourses we follow trading up as I type.

US equity averages are, save for the Dow, higher to start the session... Sector breadth, however, is suspect (utilities, energy, staples, healthcare and materials are all in the red): Dow down 60 points (0.17%), SP500 up 0.99%, SP500 Equal Weight u 0.59%, Nasdaq 100 up 2.37%, Nasdaq Comp up 2.07%, Russell 2000 up 1.16%.

The VIX sits at 17.47, down 2.24%.

Oil futures are down 0.24%, gold's down 0.42%, silver's up 1.41%, copper futures are up 1.27% and the ag complex (DBA) is up 0.75%.

The 10-year treasury is up (yield down) and the dollar is up 0.35%.

Among our 36 core positions (excluding options hedges, cash and short-term bond ETF), 22 -- led by Amazon, communication stocks, MP Materials, Dutch Bros and uranium miners -- are in the green so far this morning. The losers are being led lower by energy stocks, materials stocks, Vietnam equities, healthcare and staples stocks.

Think about today's quote, and market prospects right here, in light of the current economic setup:

"Only a strong economy can create higher asset values and sustainably good returns for savers."

--Former Fed Chair Ben Bernanke

Have a great day!

Marty

Agree! There is no going back.

ReplyDeleteApple, Google, and Amazon missed earnings. This market went up today for no reason. Corporate earnings should be rolling over first half of 2023. Rate hikes will affect corporate earnings.

Ben Bernanke in my opinion is far better than Powell. The market including myself doesn't believe a word Powell says (huge credibility issue). Now, we have four (4) new members in the group (12 members group) and they politically care more about their reputations than doing their jobs.