In client review meetings, and herein, of late, we're painting an optimistic picture of what we view as the macro-rich setup that awaits when the next bull market gets underway, while, at the same time, we’re explaining why we do not believe now is the time to express (in our core allocation) our longer-term thesis to the extent we ultimately expect to.

You see, global general conditions presently reflect what, in our opinion, can only be viewed as uncomfortably high recession risk.

And while there's plenty of global headlines and data I can cut and paste below, for this morning I'll just share the latest (intro) from the widely followed Sentix Global Economic Report:

Sentix Economic Index: Significant spring tiredness• The sentix overall economic index for the euro zone loses 4.4 points to a level of -13.1 points, wiping away a large part of the easing signals from previous months. In particular, expectations buckle to - 19.0 points, the lowest level since December 2022.

• The German economy is also gripped by significant spring fatigue. The situation scores are down by 6.7 points, while expectations have fallen to -19.8 points. Not much remains of the laborious economic recovery.

• In the international context, the minus signs dominate. For the U.S., the declines in expectations are also striking: Here, the overall index reaches -17.5 points, the lowest level since November 2022!

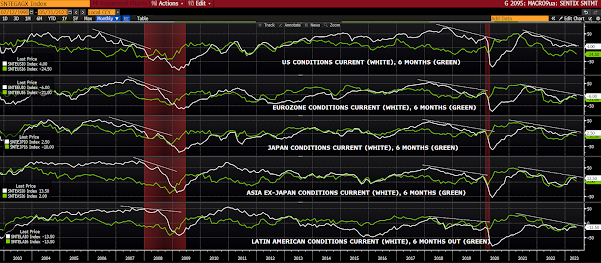

Here's how it graphs (white = current conditions, green = 6-month outlook) globally:

And broken out by area:

Note how the current trajectory today resembles the trajectory heading into the past two recessions.

Stay tuned...

Asian stocks were mostly red overnight, with 12 of the 16 markets we track closing lower.

Same for Europe, with 14 of the 19 bourses we follow in the red so far this morning.

US equity averages are lower to start the session: Dow by 375 points (1.11%), SP500 down 0.55%, SP500 Equal Weight down 0.51%, Nasdaq 100 down 0.50%, Nasdaq Comp down 0.11%, Russell 2000 down 0.74%.

As for yesterday's session, US equity averages were mostly higher: Dow down 0.09%, SP500 up 0.45%, SP500 Equal Weight down 0.01%, Nasdaq 100 up 1.11%, Nasdaq Comp up 1.04%, Russell 2000 up 0.51%.

Same for Europe, with 14 of the 19 bourses we follow in the red so far this morning.

US equity averages are lower to start the session: Dow by 375 points (1.11%), SP500 down 0.55%, SP500 Equal Weight down 0.51%, Nasdaq 100 down 0.50%, Nasdaq Comp down 0.11%, Russell 2000 down 0.74%.

As for yesterday's session, US equity averages were mostly higher: Dow down 0.09%, SP500 up 0.45%, SP500 Equal Weight down 0.01%, Nasdaq 100 up 1.11%, Nasdaq Comp up 1.04%, Russell 2000 up 0.51%.

This morning the VIX sits at 18.13, up 0.72%.

Oil futures are down 1.65%, gold's down 0.98%, silver's down 4.52%, copper futures are down 3.71% and the ag complex (DBA) is down 1.09%.

The 10-year treasury is up (yield down) and the dollar is up 0.65%.

Among our 37 core positions (excluding options hedges, cash and money market funds), 7 -- Albemarle, Amazon, AMD, TLT (long-term treasuries), XLC (communication stocks), VGIT (intermediate term treasuries) and EMB (emerging market bonds) -- are in the green so far this morning... The losers are being led lower by Disney, EZU (South African Equities), SLV (silver), OIH (oil services stocks) and DBB (base metals futures).

Have a great day!

Marty

Oil futures are down 1.65%, gold's down 0.98%, silver's down 4.52%, copper futures are down 3.71% and the ag complex (DBA) is down 1.09%.

The 10-year treasury is up (yield down) and the dollar is up 0.65%.

Among our 37 core positions (excluding options hedges, cash and money market funds), 7 -- Albemarle, Amazon, AMD, TLT (long-term treasuries), XLC (communication stocks), VGIT (intermediate term treasuries) and EMB (emerging market bonds) -- are in the green so far this morning... The losers are being led lower by Disney, EZU (South African Equities), SLV (silver), OIH (oil services stocks) and DBB (base metals futures).

"The game I play for handling both my life and my career is to try to figure out how the world works, develop principles for dealing with it well, and then place my bets."

--Ray Dalio

Have a great day!

Marty

No comments:

Post a Comment