While we get the market narrative that big tech is "long duration," and, therefore, amenable to declining interest rates, and that AI is long-term special, I think "the market" is forgetting that, at the end of the day, big tech is ultimately tethered to the economic cycle.

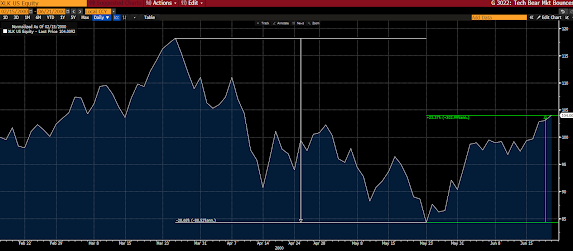

Here's the tech sector action throughout the current bear market:

Emphasis mine...

Walmart, “After a strong start, sales growth moderated as the quarter progressed…At the headline level, consumer spending has proven resilient. But below the surface, we continue to see signs that customers remain choiceful, particularly in discretionary categories.”And

Target, “Within the quarter, total sales were strongest in February, began decelerating in March, and softened further near the end of April…Strength in frequency businesses (Beauty, Food & Beverage and Household Essentials) offset continued softness in discretionary categories.”

Home Depot, “As we looked beyond weather and lumber deflation, our underlying performance in the quarter was mixed. We saw more pressure across the business compared to what we observed when we reported fourth quarter results a few months ago. While there was relative strength in project related categories like building materials, plumbing, and hardware, we had many departments with negative comps in the quarter and continued to see pressure in a number of big ticket discretionary categories.”

Foot Locker, “since our Investor Day, in the face of increasing macro headwinds, our sales trends have slowed significantly just in the past month and a half, which will have an impact on our near-term results…the recent softness has resulted in us taking a more aggressive promotional stance to drive demand and to effectively manage our inventory, and we’re reducing our guidance for the year to reflect that.”

From the NY Fed’s household debt report: “The share of current debt becoming delinquent increased for most debt types. The delinquency transition for credit cards and auto loans increased by .6 and .2 percentage points, respectively approaching or surpassing their pre-pandemic levels.” While mortgage debt levels are down a lot over the past 15 years as a % of GDP, non housing debt as a % of GDP as of Q1 is at the same level seen in Q1 2008.

One more -- just in from Lowes this morning:

"(Bloomberg) -- Lowe’s Cos. cut its sales outlook for the year a week after rival Home Depot Inc., citing a slowdown in consumer spending.

The company now expects comparable sales to drop as much as 4% this fiscal year, it said in a statement. In March, Lowe’s predicted sales by that measure might be flat or decline as much as 2%.

Lowe’s blamed falling lumber prices, unfavorable weather and lower consumer spending on DIY and other discretionary items for the forecast change. Home Depot last week cut its full-year outlook and noted a “broad-based pullback” in consumer spending."

Stay tuned...

Asian stocks were mostly red overnight, with 10 of the 16 markets we track closing lower.

Same for Europe so far this morning, with all but 14 of the 19 bourses we follow trading down so far this morning.

US equity averages are, save for small caps, a bit lower to start the session: Dow down 40 points (0.12%), SP500 down 0.23%, SP500 Equal Weight down 0.14%, Nasdaq 100 down 0.26%, Nasdaq Comp down 0.12%, Russell 2000 up 0.54%.

As for yesterday's session, US equity averages were mixed: Dow down 0.4%, SP500 up 0.1%, SP500 Equal Weight down 0.3%, Nasdaq 100 up 0.3%, Nasdaq Comp up 0.5%, Russell 2000 up 1.2%.

This morning the VIX sits at 17.79, up 3.37%.

Oil futures are up 1.89%, gold's up 0.02%, silver's down 0.14%, copper futures are down 1.23% and the ag complex (DBA) is up 0.34%.

The 10-year treasury is down (yield up) and the dollar is up 0.18%.

Among our 34 core positions (excluding options hedges, cash and money market funds), 9 -- led by Albemarle, XLE (energy stocks), MP Materials, Dutch Bros, OIH (oil services stocks) and DBA (ag futures) -- are in the green so far this morning... The losers are being led lower by DBB (base metals futures), AT&T, FEZ (Eurozone equities), VPL (Asia Pac equities) and XLB (materials stocks).

"The curious task of economics is to demonstrate to men how little they really know about what they imagine they can design." --F. A. Hayek

Have a great day!

Marty

No comments:

Post a Comment