4/19/2024

Equity futures, bonds, currencies, commodities all reacted aggressively to the initial news of Israel’s attack on a military base in Iran… As the dust settled it became clear that the attack was limited in scope – i.e., tit for tat – and, therefore, for the moment, not a market event… As I type, 7:04am, the S&P is flat, the Nasdaq’s off 56 bps, yields are down a bit, gold’s up 25 bps, the dollar’s down 21 bps and oil’s flat.

4/19/2024

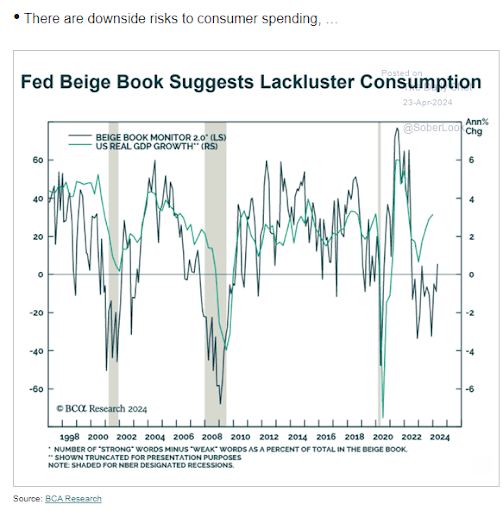

The latest Fed Beige Book release (a view from each of the 12 districts) points to an economy that continues to expand, albeit at a snail's pace at this point, and a consumer who is, on balance, becoming more cautious on spending… Inflation signals are mixed, but, on balance, somewhat problematic for businesses as their pricing power now seems to be fleeting.

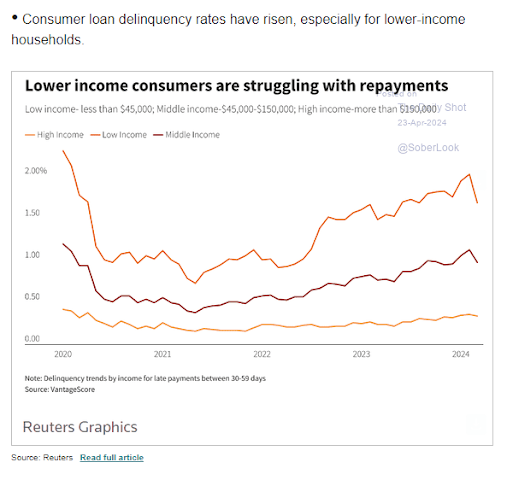

Wall Street's narrative, on the other hand, is that the US economy is on very firm footing, the labor market remains very strong, inflation will abate over the coming months, and corporate profits will hold up nicely… I more or less agree on the inflation front (although there’s real risk in that belief), however, leading employment indicators point to notable deterioration in the labor market setup in the months to come… With regard to profits, falling overall inflation along with a growingly timid consumer (read diminished pricing power) amid higher wage bases makes for some real go-forward risk to that narrative.

4/19/2024

I continue to see signs of net improvement in manufacturing, pretty much globally… I know the industry is hopeful that what amounted to a 2-year recession in the space is finally coming to a close.

I’m concerned that when I factor in a consumer who looks to be finally growing wary, and who already loaded up big-time on manufactured goods amid the whole covid phenomenon – hence the manufacturing recession as goods spending slowed to a crawl – that the latest optimism swirling around manufacturing will ultimately turn out to be one of those pre-recession head fakes I’ve charted in recent video commentaries… Time will tell.

4/21/2024

Gold and Ag:

Clearly, central banks have been the big buyers of gold, as it moves further into all-time-high territory… I imagine trend-following CTA’s aren’t hurting the bid either… Interesting thing is that GLD (gold etf) has seen notable net outflows this year (I suspect those folks are trading on “normal” correlations between gold, the dollar and interest rates), suggesting that the longer this lasts the higher the likelihood of capitulation among those sellers, as the pain of being left behind would have them pouring back into the ETF…

What (as I just alluded to) is also interesting is the fact that gold has ramped up alongside a rising dollar, and rising yields… Should indeed the dollar and interest rates give way anytime soon, that could also inspire those who’ve been avoiding gold to now join the party.

All that said, the recent rally has gold way out over its skis – technically overbought – so a noticeable pullback right about now would be no surprise whatsoever.

Another core position that continues to be a major focus of ours is ag futures (DBA/PDBA)... The run so far this year has been nothing short of remarkable (up 28% ytd), predominantly the result of cocoa’s massive 183% rise so far this year… Hogs (up 42%) and coffee (up 24%) haven’t hurt either… This has our chosen ETF position looking largely overbought, and, as we experienced 1 day last week (a 3% decline), subject to potentially swift and notable downside corrective action.

On the other hand, 5 (corn, wheat, soybeans, sugar and cotton) of PDBA’s 10 crop positions are actually down so far this year… Thus, the potential exists for rebounds in depressed crops to provide for a potential offset to the downside risk of presently overbought positions… Of course the dynamics around commodity correlations, trading and price action in no way assure that such a “rotation” is necessarily likely to develop.

4/22/2024

Sure enough, gold opened 2+% lower this morning (silver’s off over 4%)… Technically it’s notably overextended right here… The commodity complex in general is selling off as well…

Stocks, the major averages that is, after 6 straight down days, are catching a bit of a bid… Although commodity stocks (materials, energy, miners) and regions are taking a hit.

The near-term market setup is not all that conducive to further gains in commodities in my view… While they’ve impressively bucked the higher dollar and interest rate trends of late, I don’t see that as a sustainable relationship going forward… I.e., commodities are presently vulnerable to a decent pullback, unless the data, yields and the dollar begin to soften notably in the near-term (which is certainly not outside the realm of possibilities right here).

4/23/2024

On balance, global PMIs are improving, and when we think about the prospects for, let’s say, stabilization outside the US (as dubious as those prospects may be at the moment), amid a peaking of activity in the US, there’s a case to be made for some short-term dollar weakness… Which could be net-bullish (short-term) for US equities and commodities in general… If, however, we see strong US GDP and sticky PCE this week, that would be net-bullish for the dollar, and, thus, odds would favor equities plumbing the lower edges of that 5 to 15% pullback we recently flagged in the charts.

That said, of course Q1 earnings results could get in the way of any short-term equity market narrative.

4/23/2024

Our ag position, gold, silver materials, energy, and commodity producing regions are continuing lower this morning. Gold miners, interestingly, are bucking the trend (up 1%).

While the above are key to exploiting how we see the world unfolding in coming months/years, they are all extended right here, and, save for gold, vulnerable to a potentially slowing economic backdrop… Although a weaker dollar, initially – should a counter-trend move materialize – could serve to mitigate some of the potential downside.

Cutting and/or hedging our commodity exposure is beginning to feel prudent right here.

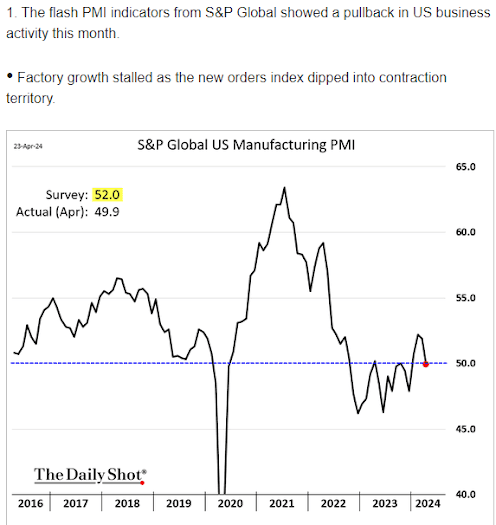

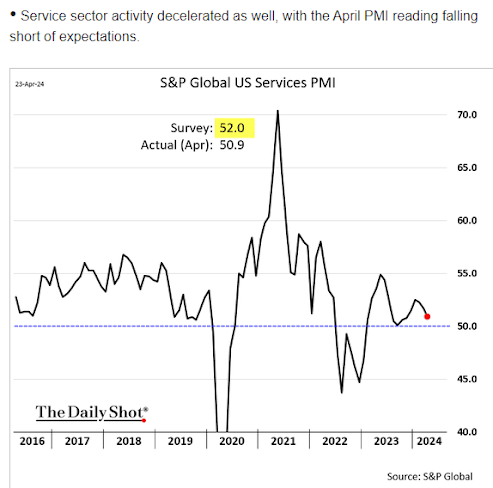

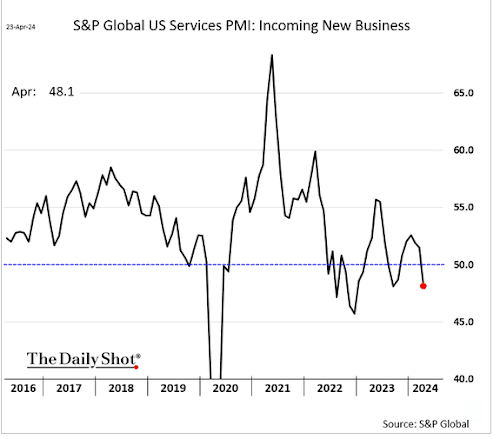

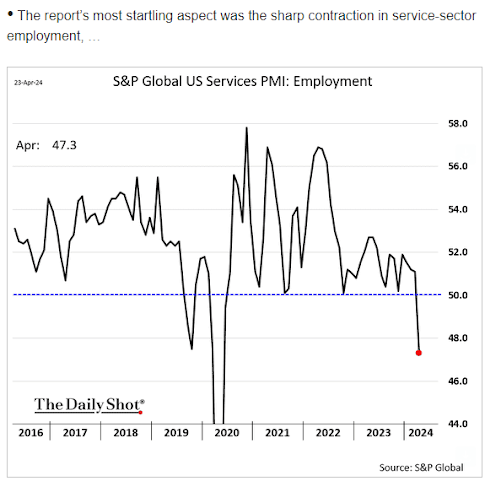

4/24/2024

Consistent with the notion that the US economy may be peaking, while others may be stabilizing (and that recent strength in manufacturing may ultimately prove to be a head fake), were this week’s US flash PMIs (preliminary purchasing manager survey results):

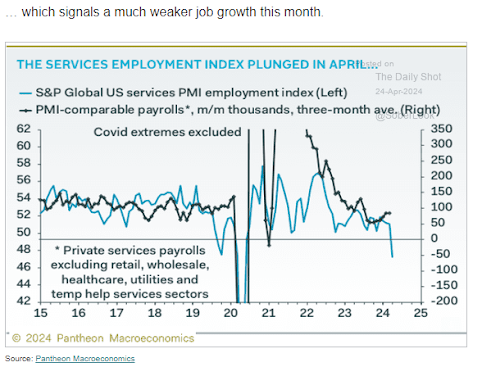

And supporting our view that weakness in the US labor market is in the offing:

4/24/2024

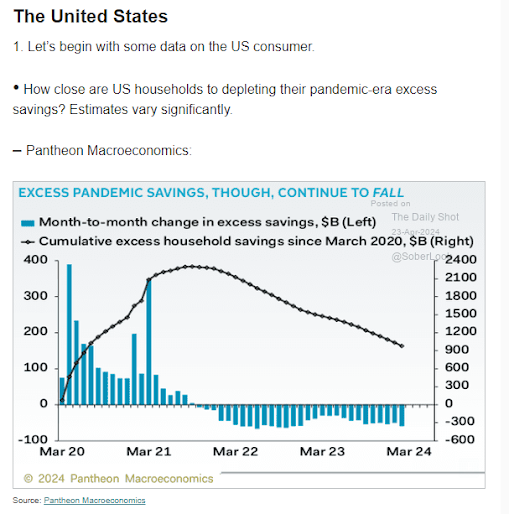

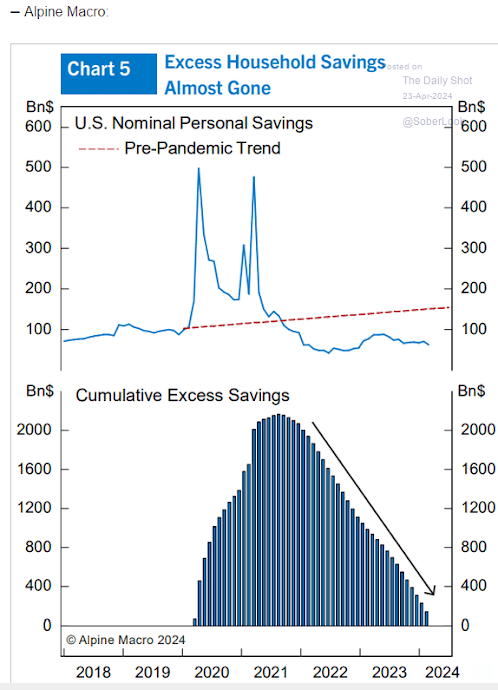

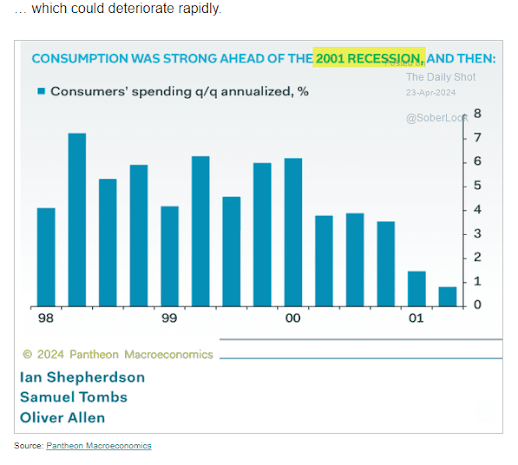

Yesterday’s Daily Shot featured estimates on the ever-elusive “pandemic savings” calculation, and other evidence, some already featured herein, that consumer oomph for the economy is likely to fade over the coming months – validating our still-heightened-recession-risk PWA Index score:

No comments:

Post a Comment