4/18/2024

Yesterday saw a rebound in our commodity-oriented, non-US equity and fixed income positions, essentially resulting in a resumption of the recent trend where our core allocation notably outperforms the broad US equity averages. That said, and to be clear, this week’s comments in that regard should not be taken as me suggesting that equities are a benchmark that we strive to match or beat, they’re not, it’s simply an observation, given that our industry indeed scores itself relative to equity markets, which, in my view, is a potentially dangerous distraction from the task of responsibly managing (and risk-managing) client portfolios.

4/17/2024

Yesterday saw the S&P and NDQ 100 down just slightly, while the commodity complex, along with most non-US markets, took quite the drubbing… The culprits being yields and the dollar as Powell had no choice but to tone down his of-late dovishness (the market’s now pricing in only .4% worth of rate cuts this year)… I.e., the latest data simply don’t allow the Fed to credibly talk up the odds of 3 rate cuts this year, the first coming as early as June.

That said, and ironically, the odds that the latest employment and inflation data actually represent a peak in both are indeed not-small right here – the looming driving season (potentially higher gas prices) notwithstanding.

I.e., it would not surprise me in the least to see rate cuts put right back on the table over, let’s say, the next couple of months, which would be short-term bullish for equities (globally), and for the commodity plays that took such a beating yesterday as well… However, if the leading employment indicators that have me thinking peak right here take longer to play out, and if inflation remains stickier for longer, that 5% to 15% pullback in equities I’m seeing in the charts will have little problem playing out – which, in and of itself, would likely take the Fed right back to talking up rate cut odds sooner than later.

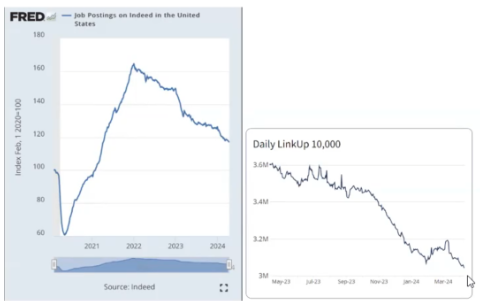

Speaking of leading employment indicators (Indeed and LinkUp job postings):

4/16/2024

After quite the run for our core allocation relative to equities, outperforming the S&P by 3% since March 1st, the components of our core portfolio that largely explain recent performance – ag futures and commodity producing regions’ equities – took quite the drubbing today… With regard to ag, we’ve been anticipating, at a minimum, an overbought pullback in our ag etf, as it’s now largest position, cocoa futures (up 160% year to date), is hugely overbought right here… Hence it plunged over 8% today, taking PDBA and DBA down nearly 3% in the process.

We did recently cut the position, albeit slightly, along with gold (which also looks overbought right here).

Here’s from our core allocation notes:

4/1/2024

Rebalanced GLD and PDBA/DBA to target.And here’s Bloomberg on today’s cocoa action:

Both gold and ag have had impressive runs (ag in particular, up 20%) year-to-date. And while we’re bullish on both themes long-term, near-term dynamics (for gold in particular), and the technicals, suggest that this is a good time to trim both positions, albeit modestly, back to their respective targets.

“...cocoa futures in New York slumped as much as 8.1% to trade at $9,699 a ton, snapping a seven-session advance that had brought prices to a fresh record. The fall eased the most-active contract out of overbought territory.4/15/24

But the plunge “is just breaking the rally that we’ve had here the last few days” and could be short-lived, especially if processing figures due Thursday are stronger than expected, said Jack Scoville, vice president at Price Futures Group.

Read More: Cocoa Scarcity Distorts Grinding Data’s Role as Guide of Demand

“I’m just sitting around waiting around for the top to show itself and so far it’s not showing itself,” Scoville said.”

This on retail sales by P. Boockvar is worth copying and pasting:

"Core retail sales rose 1.1% m/o/m in March, well better than the estimate of up .4% and February was revised up by 3 tenths to a .3% gain. Gasoline sales, not included in the core, were up 2.1% m/o/m. Food/beverage sales (includes supermarkets) grew by .5% m/o/m and 3.5%. Health/personal care sales were higher by .4% m/o/m.4/15/24

Notwithstanding the seemingly strong figure, the internals were VERY mixed. Sales for furniture, electronics, clothing, sporting goods and department stores all fell m/o/m. For autos, not included in the core, sales were down by .7%. On the flip side, most of the sales gains was driven by a 2.7% jump in online retailing and the miscellaneous category which includes convenience stores and pet stores among others. Restaurant and bar sales were up by .4% m/o/m and 6.8% y/o/y and continues to also be a bright spot.

Bottom line, if one just looks at the headline data one would say sales were strong but as stated, they were much more mixed internally with online leading the way but also the needs, more so than wants as food/beverage and health/personal care also saw gains."

As it turned out, or at least as it appeared, equities did have a real problem with the hot retail print after all… Bonds stayed slammed from the open, and stocks rolled over during the session to close down more than 1%... Interestingly, gold reversed again and closed up 1.7% – the media narrative being that middle east tensions remain high, sustaining a bid under gold: Implying that gold indeed sold off on the retail news, but woke back up to the present geopolitical setup… Plus, Goldman today raised its year-end target to 2,700 an ounce.

4/15/24

Bonds are falling and stocks are rising in the aftermath of the most telegraphed sneak attack in history.

Hot retail sales released this morning didn’t see an initial reaction (would’ve expected selling, given the Fed policy implications of strong retail sales), however, as I type (45 minutes after the release) equities are well off their earlier levels… Gold and bonds are making sense, given the retail sales print, both lower (with gold outright reversing earlier gains).

4/13/24

Japan just saw the biggest one-month wage increase in 30 years (2.2%)... That’s the kind of data that’ll eventually put a serious bid under the incredibly underpriced, and over-shorted, yen… A weakening US economy, which has not-small odds going forward, won’t hurt the yen either.

The UK economy, after seeing growth in January and February, is technically out of recession… Our recently-added position in UK stocks is up 3% since we entered it.

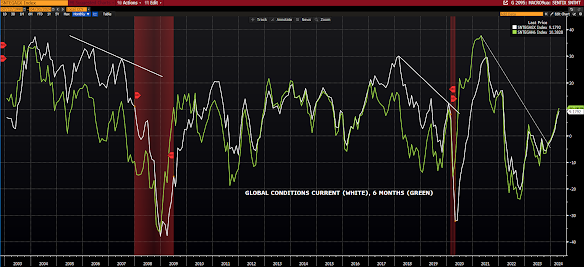

While I maintain that it’s not at all unusual to see an upside economic headfake just before recession ensues (evidenced even in the Sentix graph below), I can’t deny the fact that globally things are – in a number of spots – indeed looking up… Which, on a relative basis, given our current global reach, bodes potentially well for our core allocation…

Here’s from Sentix’s April 8 report:

“Will there finally be a sustainable economic upturn? At least the economic recovery in the eurozone and world-wide is continuing. We are measuring the sixth consecutive rise in the overall index for the eurozone. The index rises to -5.9 points. Expectations for the eurozone have even risen for the seventh time and, at +5 points, are at their highest level since February 2022. The economic signals are also stabilising internationally. Only Austria is an exception here with a completely divergent development.”And here’s our chart of the current Sentix view (from their survey) – current conditions and 6-month expectations – of the global setup:

4/13/24

Bob Elliot has a thesis that says the current expansion is very different than anything we’ve experienced in the past several decades… It’s essentially a sustainable “income-financed” expansion.. As opposed to credit driven/financed expansions, that are inherently/ultimately destined to crash and burn as debt levels become eventually untenable…

I.e., in his view, income-driven expansions are, by their nature, sustainable… To the extent that one person’s spending is another person’s income, and that income-driven growth doesn’t leave the wake of debt the way a credit-driven expansion does… So, in the present case, balance sheets are actually improving as incomes are rising, vs the opposite in a credit-driven expansion.

I like it, it’s thoughtful, it makes some sense…

However, I would add that another major driver of the current expansion is simply the sentiment spawning from the wealth-effect (rising asset prices) that have been, to no small degree, artificially supported by government and central bank policy (guidance, as opposed to money creation, with regard to the latter playing a major role of late).

Should markets ultimately tumble under the weight of extreme valuations, financial market leverage (read derivatives) and, at best, a slowing pace of economic growth, reflexivity (a pulling in) among the cohort (the upper half of the income ladder) who owns assets and who are now doing the heavy lifting on spending could essentially be the straw that breaks the economic camel's back before it’s all said and done.

My take, in terms of what may catalyze the next recession (a reflexive response to a serious enough hit to asset prices), is actually not in conflict with how Bob ultimately sees the next downturn playing out… In his view though it’ll require higher interest rates than current, which will hit asset prices, suppress demand and bring on the next recession.

4/13/24

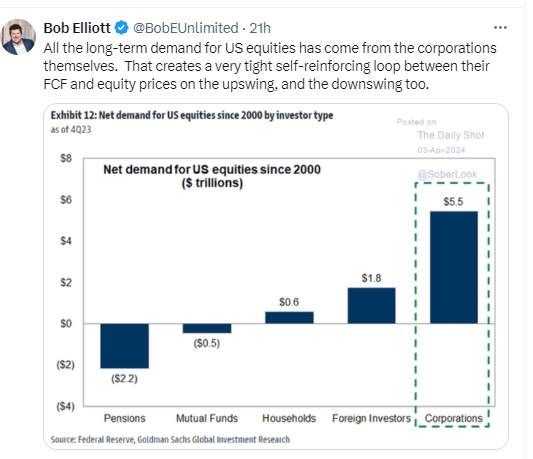

Bob Elliot makes a compelling point regarding the impact of share buybacks on the market, and the pressure on stocks that would therefore occur if/when free cash flow takes a hit (i.e., during recession):

No comments:

Post a Comment