Dear Clients, per my last note, you'll be receiving fewer blog notifications going forward, as we're now summarizing for you the key global economic and market signals, trends, etc., that we record in our internal log each week... Be sure and peruse all the way to the end, as we highlight a broad range of topics.

Resulting in stocks down, oil, gold and bonds up in early Friday trading.

Here are some key bullet points from this week's log (clarification added parenthetically): Have a nice weekend!

Here are some key bullet points from this week's log (clarification added parenthetically): Have a nice weekend!

- In a nutshell, market expectations are for 2-3% GDP growth this year, 3% inflation and 2-3 rate cuts... The odds of that scenario playing out are substantially low... (i.e., those growth and inflation expectations wouldn't generally allow for market-pumping rate cuts from the Fed)

- The ECB (European Central Bank) held steady, while sending a message that rate cuts are very much on the near-term horizon (which would be bearish the Euro, bullish the dollar)... Also making a statement that they’re in no way waiting for the Fed to move first... All the while economic expectations for the region have improved… Considering the above, and relative valuations, European equities are looking more interesting right here.

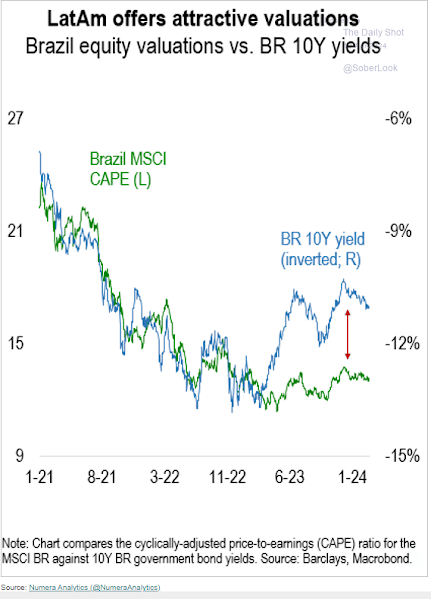

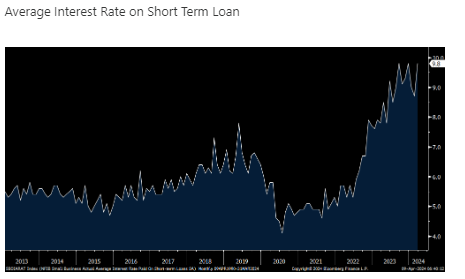

- Brazil inflation hit a 9-month low (3.9%)... There’s lots of room for monetary policy to ease going forward… That, by itself, is bullish for Brazilian equities and fixed income.

The overall setup for Brazil remains very long-term compelling… Aside from the macro dynamics, there’s the massive gap that separates interest rates from equity market valuations.

Charting that disconnect:

In fact, the Lat Am region in general, remains very long-term compelling right here:

- South Korean exports (AI chips) are surging.

- Philippine exports are improving (up 16% over last year).

- EM (emerging market) bonds are heavily shorted right here… I.e., the market anticipates higher inflation going forward.

- While pockets of weakness indeed remain, global economic indicators are, on net, improving… Head-fake risk remains elevated, however.

(Global PMI [purchasing managers index] up to 52.3 [above 50 denotes expansion]):

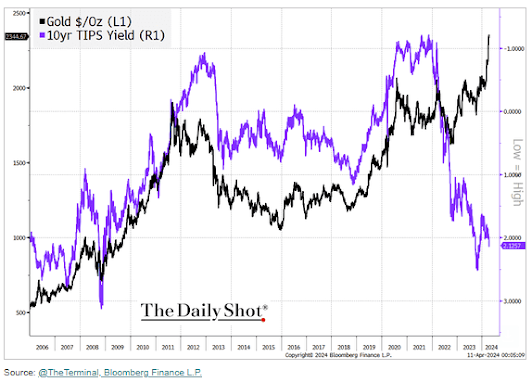

- Gold’s correlation to real rates has completely broken down – clearly it’s trading on other factors:

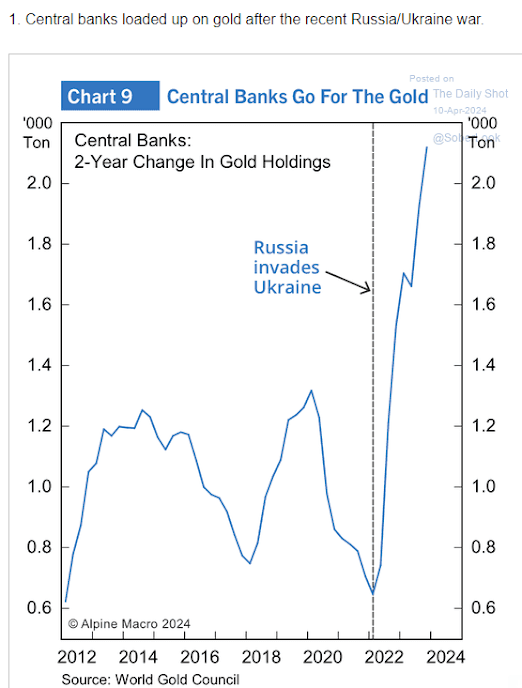

- As we suspected, Central Banks have been a driving force for gold of late:

Additionally, I do believe that gold is discounting ultimately declining interest rates as the economy slows over the coming months, while, historically-speaking, inflation – while it’ll cool – will remain stubbornly sticky relative to past economic downturns. I.e., the odds of stagflation going forward are not small.

All that said, the technicals point to the potential for some healthy corrective action, in the near-term.

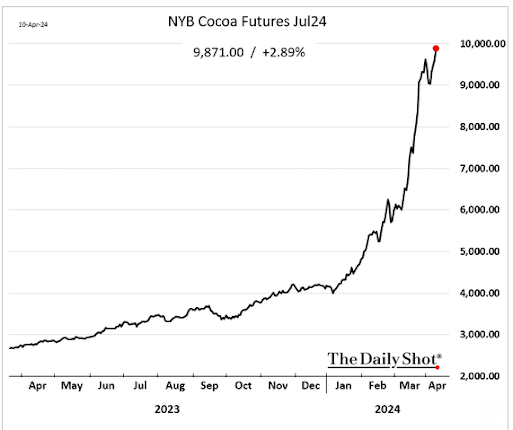

- Cocoa continues to scream higher... That, along with coffee and hogs, is making our ag play very special so far this year -- while corn, wheat and beans have been a drag… The dynamics where cocoa grows (weather, politics) suggest that a crash may not be imminent… Although the chart looks technically scary to me right here:

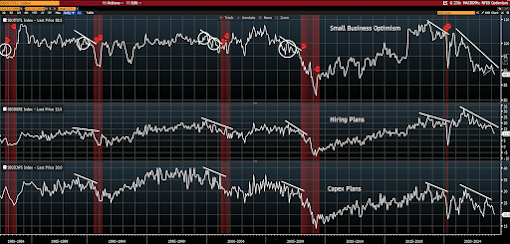

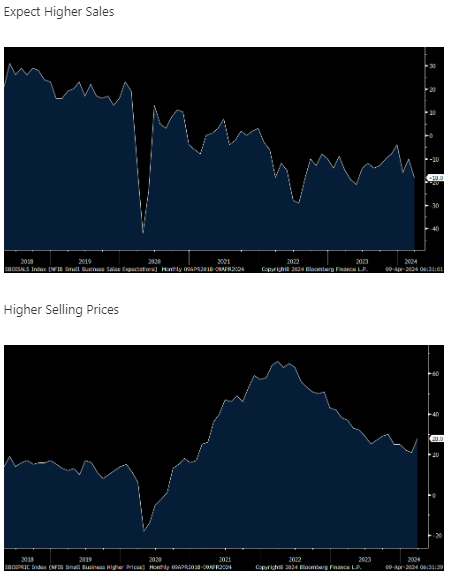

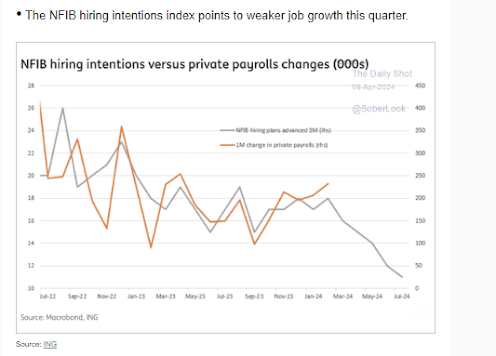

- The latest NFIB (small business) survey is a mess:

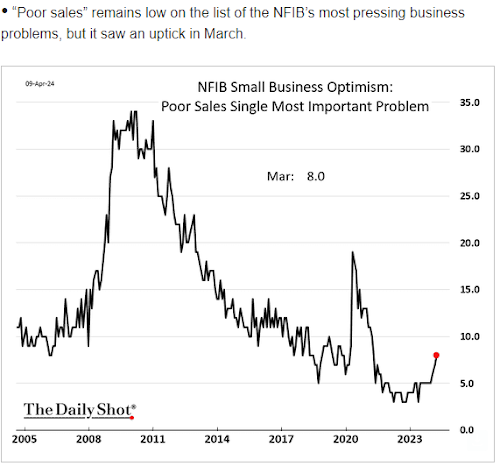

And here’s a look at the relationship between a poor sales outlook and the unemployment rate.

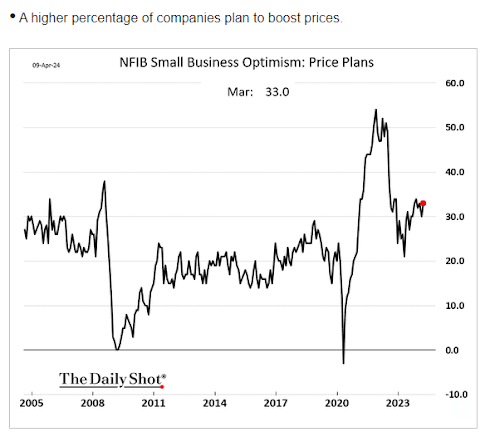

And, to add insult to injury, small businesses plan to raise their prices:

- CPI came in hotter than expected... Fed funds futures quickly slashed rate cut expectations from 3 to 2 for this year.

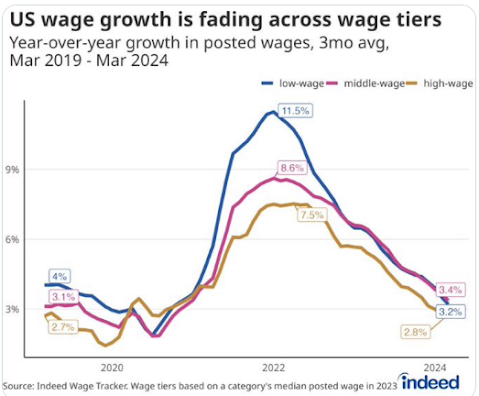

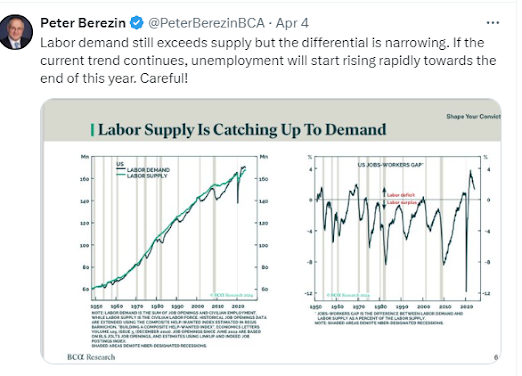

Despite our long-term structural inflation thesis, leading employment dynamics suggest that, like the recent uptick in manufacturing activity, this could very well become a last-gasp headfake for those betting that inflation will embark on a new surge higher from here… I.e., odds indeed favor a cooling of inflation as the balance of this year unfolds.

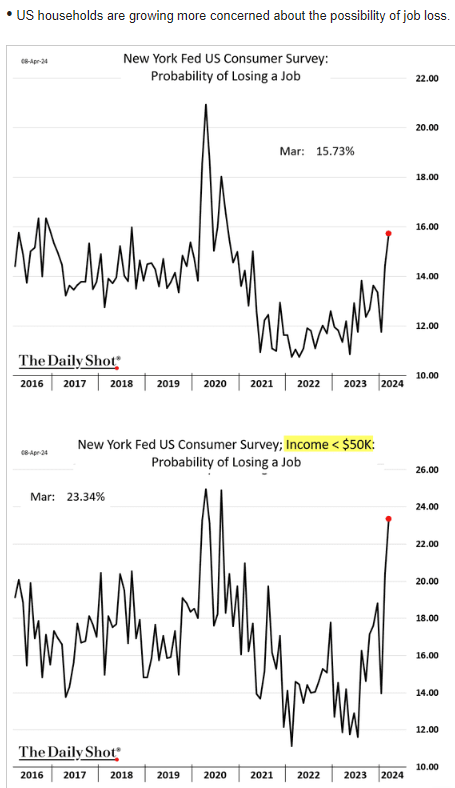

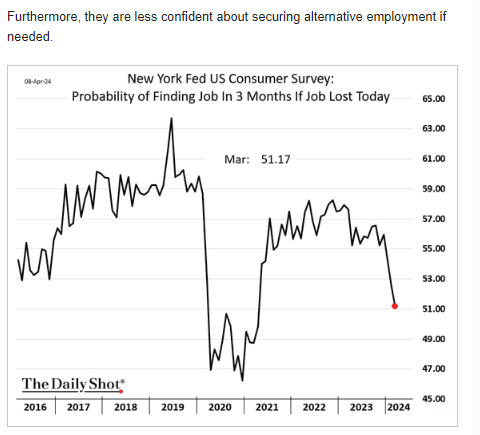

Also, despite the notable improvement in our general conditions index, I think the leading employment data – along with the latest consumer and small business sentiment readings – makes a still somewhat compelling case that indeed recession odds remain relatively high on a 6 to 12 month outlook.

As for US equities, I look for a potentially sharp rally (all the more sharper if preceded by a sharp correction [which the charts presently threaten]) once weaker inflation begins to get priced in over the coming months… But then giving way, potentially bigly, to the downside as the underlying reason for that weaker inflation (recession) captures the prevailing narrative, as well as corporate earnings expectations.

- “Tight supply and somewhat improving global PMIs are boosting copper of late. In China, in particular, copper demand is up 10-12% this year.” A popular narrative presently.

Oil, gold, silver are all rising, even as bond yields rise – essentially reflecting late-cycle inflationary dynamics.

The dynamic that conflicts with copper’s run is plunging iron ore and steel prices. Implying that copper is idiosyncratic specifically to China’s massive investment in renewable energy (solar panels and wind turbine production up 100% over the past year).

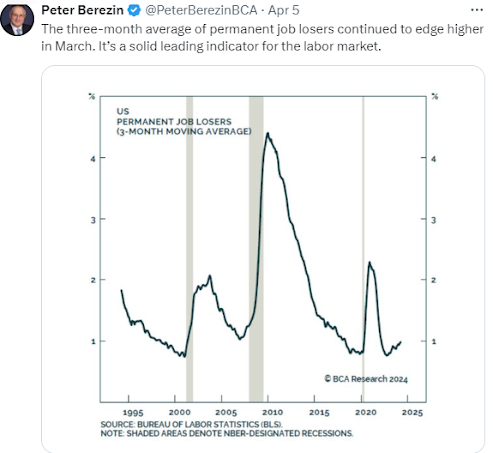

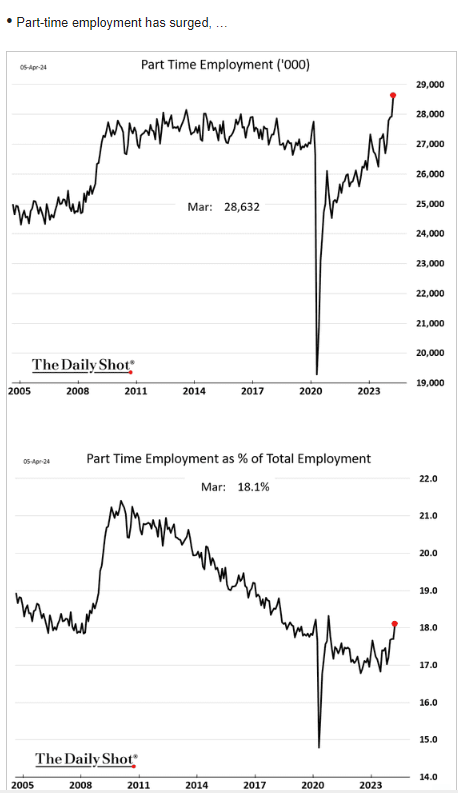

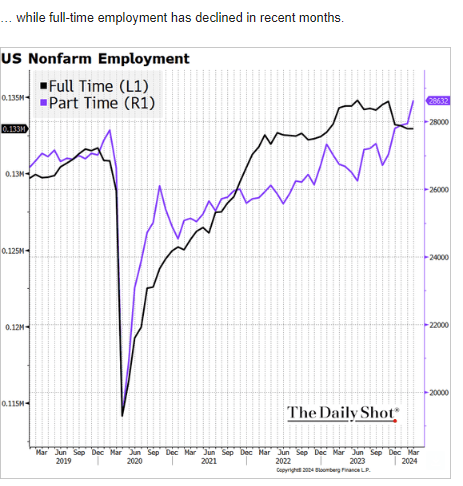

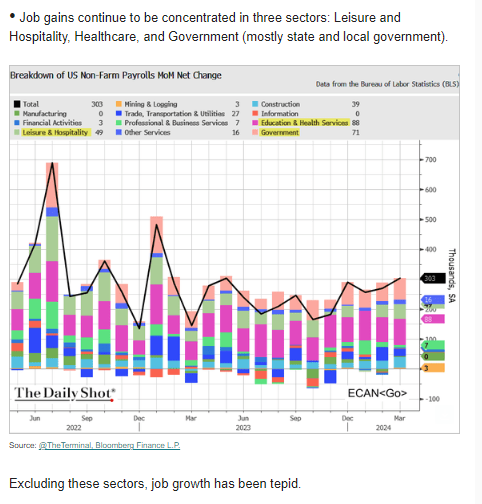

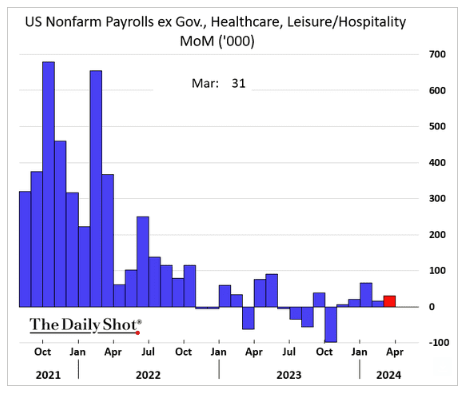

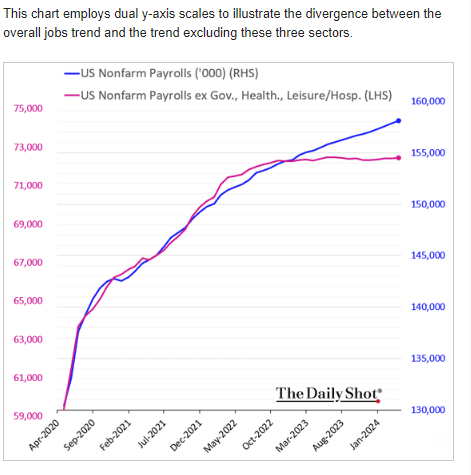

- Last week’s headline jobs number impressed, however a plethora of leading employment indicators imply weakness is likely on the near-term horizon… Ironically, just as the world seems to be abandoning last year’s overwhelmingly recessionary thesis, it may very well see it occurring over the coming (6-12) months.

Slowing, or contacting, employment will see inflation expectations decline and, likely, the dollar along with it… We could therefore see a bit more upside in US equities initially before they give way to recessionary forces... However, the most likely beneficiary of these short-term dynamics will be emerging mkts.

No comments:

Post a Comment