Believe it or not, in a feeble attempt at brevity, I cut a ton out... So, clients, if you'd like more color on any of the below, or anything else that went on in global markets/economics this past week (even if it's not featured below, there's a good chance I commented on it internally), please feel free to reach out.

Last Thursday, 4/25 -- GDP

Although I can't say that (while not overly alarming just yet) the details around consumer spending (other than perhaps imports) reflect a necessarily strong economy.

From the report:

"The increase in consumer spending reflected an increase in services that was partly offset by a decrease in goods. Within services, the increase primarily reflected increases in health care as well as financial services and insurance.

Within goods, the decrease primarily reflected decreases in motor vehicles and parts as well as gasoline and other energy goods.

Within residential fixed investment, the increase was led by brokers’ commissions and other ownership transfer costs as well as new single-family housing construction.

The increase in nonresidential fixed investment mainly reflected an increase in intellectual property products. The increase in state and local government spending reflected an increase in compensation of state and local government employees.

The decrease in inventory investment primarily reflected decreases in wholesale trade and manufacturing.

Within imports, the increase reflected increases in both goods and services."Equities are taking a pretty good across-the-board hit as I type.

As for fixed income: With regard to the prevailing sentiment around bonds (as evidenced in the prevailing trading action), I think the market’s ultimately getting it all wrong.

I.e., bonds tanking (yields spiking) on stubborn inflation and a less-accommodative Fed, entirely misses the odds that this is indeed the sort of late cycle phenomenon that tends to precede, if not bring on, recession… Essentially, the bond market is likely in the early stages of delivering up a historic buying opportunity… We won’t rush there just yet, but if this keeps up, we’ll be buying duration in a not-small way very soon.

This Monday 4/29 -- Same Fed Setup

The Fed has very little headline macro data that would support any sort of a dovish message this week… Although that’s what I thought heading into the last meeting, and Powell pretty much quelled any market fear around rate cuts not occurring this year.

So, same setup this week, although it does appear that other “doves” on the committee are feeling a bit hawkish right here.

If Powell leans hawkish, the dollar will rally and stocks and bonds will likely suffer… Caveats to assets falling would be earnings announcements and the treasury’s quarterly refunding announcement.

Friday’s jobs number won’t be small either.

Cocoa is taking a hit today – down 10% this morning (up 140% ytd) – which is having a not-small impact on our not-small DBA/PDBA position (down 3% as I type).

All things considered, it seems prudent to take a bit more off the table right here… I.e.,, It’s been a great position for us of late, realizing some profits amid such elevated cocoa, coffee and hog prices makes sense… That said, about half of the represented crops in the fund are flat to down year to date; so it’s not that the entirety of the fund is over-extended, it’s just that the phenomenal move in cocoa, for example, makes it too concentrated for comfort (at present position size) for the time being.

This Monday 4/29 -- Dollar Bulls

FX futures traders’ positioning presently shows speculators leaning in favor of a near-term higher dollar.

Clearly, they’re anticipating a hawkish message from the Fed this week, and data releases that support that view… Anything (the Fed and/or the data) coming in soft could easily see a knee jerk dollar selloff… All else equal, that would be bullish for equities and commodities.

This Tuesday 4/30 -- Labor Costs

The US Employment Cost Index (ECI) came in hot this morning, doing a pretty good number on global equities, although US tech holding up better (down notably less than the broader market)... Long-term treasuries are off .60%... Gold’s off 1%, the commodity complex (DBC) is taking a bigger hit (-1.5%), ag (DBA) is off 1.3%... Miners (-1.5%), and commodity producing regions of the world (Brazil -1.5%) are suffering this morning as well… The dollar is up .30%.

As for our core allocation, recent adjustments move XLV (healthcare) to our 3rd largest individual position, which – bucking the trend this morning (+0.51%) – is in effect mitigating a bit of the commodity hit this morning.

This is of course the kind of data (as lagging as employment data tends to be) that further rejects the notion that a rate cut cycle is ready to begin.

Tomorrow’s Fed statement and Powell presser should be somewhat (short-term) telling.

Our recent cuts to our commodity exposures appear prescient at the moment.

This Tuesday 4/30 -- Consumers Less Confident

The Conference Board Consumer Confidence Index was released this morning, which coupled with the ECI, delivered a double whammy to markets (Dow’s down 400 pts, SPX down 1%, Nasdaq down 1.2%, smallcaps down 1.6%, yada yada, as I type)… Our core portfolio isn’t doing much better (just marginally better), since commodities are taking a pretty good hit this morning as well.

The consumer survey confirms the lagging nature of the latest hot employment data, as folks aren’t feeling good about the present state of the labor market (their job prospects going forward, in general)... Plus, they are suffering under the weight of inflation and don’t see any light at the end of that particular tunnel going forward.

Quite the conundrum for the Fed.

While, indeed, the latest data – in terms of what it means for the Fed – support a pullback in equities right here, the charts, as I pointed out at the recent peak, were already signaling high odds of what I anticipated to be a 5-15% correction coming off of that level.

So, the QRA (treasury quarterly refunding announcement), in terms of projected Q2 borrowing, did not come in as many expected, nor as I intuitively thought would be signaled… Apparently, per Peter Boockvar below, tax receipts came in surprisingly lower than forecast:

“...the US Treasury said yesterday in the announcement that they needed to borrow more than expected in Q2, "The borrowing estimate is $41 billion higher than announced in January 2024, largely due to lower cash receipts, partially offset by a higher beginning of quarter cash balance." The bold is mine as with an unemployment rate still below 4% and the economy supposedly 'strong', why are tax receipts coming in less than expected?”

The ECB (European Central Bank) isn’t making it easy on itself.. Lagarde was too confident during the last policy meeting in signaling rate cuts soon to come… Since then the data is simply not cooperating.

Indeed, such data, all else equal, would be net-bullish the Euro, especially if we see the latest pickup in US inflation come off the boil sooner… Which would also be net-bullish US equities and, in particular, gold – again, all else equal.

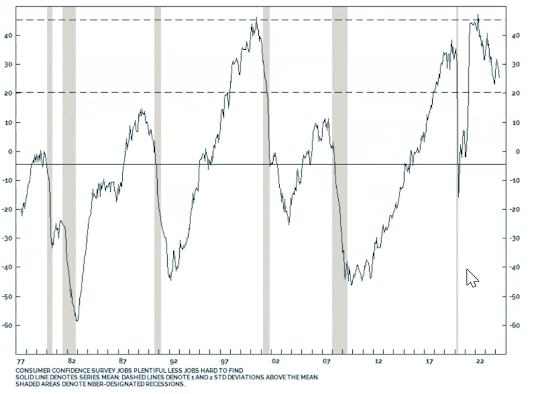

Today, Wednesday 5/1 -- Consumer's Not Feeling the Job Mkt

The “net jobs plentiful” component of yesterday’s Conference Board Consumer Confidence Index jibes with our view that weakness in the labor market is brewing beneath the surface, and that such brewing is typically problematic for the economy (shaded areas are recessions):

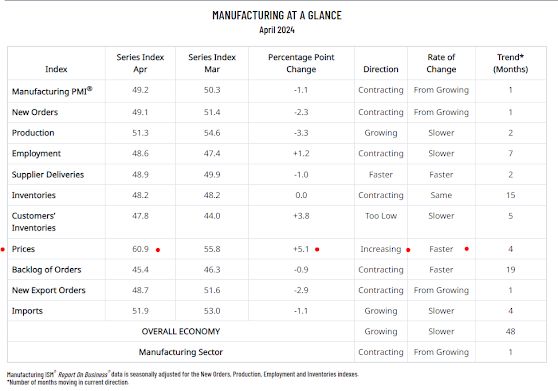

Today, Wednesday 5/1 -- Manufacturing Sentiment Rolls Back Over

The ISM Manufacturing Index’s move into expansion territory, for now, has been very short lived…After ending a 16-month stint in contraction last month, it has abruptly turned back below 50 (the contraction/expansion dividing line), to 49.2, for April.

Per the following, it was certainly not a horrible report by any stretch:

“Demand remains at the early stages of recovery, with continuing signs of improving conditions. Production execution continued to expand in March, but at a slower rate of growth than in prior months. Suppliers continue to have capacity but work to improve lead times, due to their raw material supply chain disruptions. Thirty-four percent of manufacturing gross domestic product (GDP) contracted in April, up from 30 percent in March. More importantly, the share of sector GDP registering a composite PMI® calculation at or below 45 percent — a good barometer of overall manufacturing weakness — was 4 percent in April, higher than the 1-percent figure in March, but an indication of better health than the 27 percent recorded in January. Among the top six industries by contribution to manufacturing GDP in April, none had a PMI® at or below 45 percent,” says Fiore.

The nine manufacturing industries reporting growth in April — in order — are: Nonmetallic Mineral Products; Printing & Related Support Activities; Primary Metals; Textile Mills; Electrical Equipment, Appliances & Components; Petroleum & Coal Products; Transportation Equipment; Chemical Products; and Plastics & Rubber Products. The seven industries reporting contraction in April — in the following order — are: Miscellaneous Manufacturing; Machinery; Furniture & Related Products; Wood Products; Food, Beverage & Tobacco Products; Fabricated Metal Products; and Paper Products."However, per the read across all components, the prices input has to be troubling to the Fed:

Today, Wednesday 5/1 -- More on Treasury Borrowing Plans

Part 2 of the Treasury Quarterly Refunding Announcement (QRA) occurred this morning, and, to my, and many pundits’, surprise – on top of there being more issuance to come (reported Monday) than expected – there remains plenty of issuance of the coupon variety (along the curve), which is definitely NOT the boost to markets I anticipated from Yellen… In fact, it risks precisely the opposite.

Powell can either quell the inherent near-term market risk presented by the QRA with some dovishness during today’s presser, or he can exacerbate it with a hawkish message… The S&P is down .31% as I type, the Nasdaq is off .75%... Long-term treasuries are actually catching a slight bid so far this morning (interesting!).

Today, Wednesday 5/1 -- Powell Wants A Reason To Cut

My comment in our internal chat channel during Powell’s press conference:

“He said they'll cut if they see weakness in the labor market, independent of inflation (in essence)... I absolutely do see weakness in the labor market coming… Until recession is obvious that's going to be bullish for equities! There's still some not-small risk embedded in the current setup, but, say, on a 5-6 month horizon, upside risk is probably pretty high…”Today, Wednesday 5/1 -- Powell Worries Over Markets

If there was ever any doubt that Powell has a laser focus on the equity market, his utter refusal to answer the “did you guys discuss rate hikes” question, should entirely dispel that doubt.

Today, Wednesday 5/1 -- Job Weakness Coming

One of our best performing core positions this year – ag futures (DBA/PDBA) while still up nicely, has abruptly taken an about face:

YTD

The biggest contributor to the gains has been cocoa, which has been the biggest culprit amid the sell off.

We recently cut the position twice, 25% each time, the first cut coming just off the top, the second yesterday (the position’s down another 3% today).

With regard to what’s bringing cocoa a bit down to earth, it’s clearly not a reversal of the upside drivers, other than liquidity, that is.

Per Bloomberg yesterday:

- Cocoa Prices Swing Wildly as Liquidity Overshadows Supply Issues

- Fewer companies can afford rising costs to back their trades

- Market is still beset by shortage due to issues in West Africa

Today, Wednesday 5/1 -- Market Reaction to the Fed

While the abrupt failure of today’s impressive Powell-presser-equity-market-rally toward the close was no doubt a shock to those desperate to see an end to the pain of what amounted to a pretty ugly April -

Intraday SP500 today:

April:

- at the end of the day, it made essence… Traders were right to buy when Powell made it clear that he still cares about the equity market, and they were right to sell when the presser curtain closed, considering that the latest data more or less tie his hands, for the moment.

In a nutshell, as long as the data (inflation and jobs, that is) remain relatively hot (next up Friday’s jobs report), look out below… However, the moment the jobs market, in particular, softens, look out above – as Powell and company swoop in.

Longer-term, if a weakening jobs market morphs into recession, as it historically tends to, then look out below, one last time, for what will at last become a fundamentally-compelling moment to buy (the right stuff) with both fists.

No comments:

Post a Comment