Be sure and read start to finish, as we cover lots of important ground over the course of a week.

Clients, if you'd like more color on any of the below, or anything else that went on in global markets/economics this past week (even if it's not featured below, there's a good chance I commented on it internally), please feel free to reach out.

Last Friday 5/24/24:

Per some of our recent tactical adjustments, we’re anticipating a decoupling among global economies… Europe, in spots, for example, had been in recession while the US continued to chug right along… Recent data suggest that Europe has bottomed, while we believe the US – despite yesterday’s positive PMIs – is in the process of peaking, if it hasn’t already peaked.

So, question being, can the rest of the world (we’ve seen some stabilization in China, for example, as well) sustain a new growth cycle, if/when the US slows markedly?

While I remain skeptical on a 6 to 12 month horizon, over the next few months I expect this pending divergence to actually embolden the soft-landing crowd, and to result in a potentially notable outperformance of non-US equities over US.

The narrative being: The US is naturally slowing, and the Fed will naturally loosen, keeping the US afloat… The rest of the world will carefully (in a manner that’ll not bring inflation roaring back) accommodate its nascent recovery… I.e., disinflationary forces coming from a US slowdown will essentially aid the rest of the world in their efforts to nudge their economies along.

It’s ambitious, and, frankly, it’s not entirely implausible.

Yet it remains anything but a given that such a Goldilocks scenario will play itself out, amid a weakening of the world’s largest economy, elevated geo-political strains (China, for just one example, is likely to, very soon, issue retaliatory tariffs on the US and Europe), excessive US equity market valuations (a recession-induced US bear market could reflexively hit global markets/economies), and so on.

With regard to markets, yesterday’s selloff (Dow down 600+ points), was not about news of US weakness, in fact it was quite the opposite.

Like I said recently:

“...we lean slightly constructive on equities and bonds in the very short-term, as we believe they’ll rally in the face of continued weakness (and the attendant accommodative Fed guidance) – with that (continued weakness) being our present base economic case.”

“The risk to our short-term view is if inflation does not continue to abate from here and that the labor market, etc., remains stronger than we currently anticipate over coming months… Such a scenario will not allow for the Fed to ease, which (the anticipation of such easing) is, in our view, very much what keeps markets buoyed right here.”I.e., again, yesterday’s selloff was all about evidence of strength, not weakness, in the US economy… Although nothing in yesterday’s data was compelling enough to suggest that a weakening is not on the horizon… Thus, we remain constructive on equities in the short run (non-US in particular) and cautious on an intermediate-term basis.

Also last Friday:

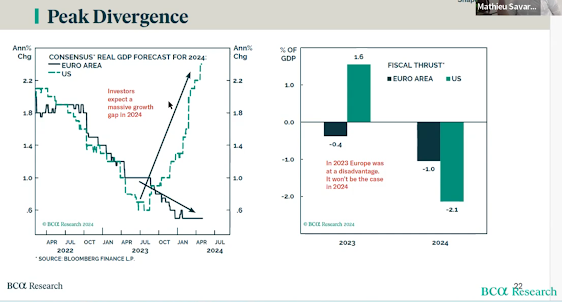

To understand the notable decoupling of the US and Europe (left chart) – and the rest of the world, for that matter – we need to look no further than to the massive fiscal stimulus (first set of bars on right hand chart) by the US in 2023 – compared to virtually all other nations… But note the abrupt turnaround (from fiscal thrust to fiscal drag) for the US this year (second set of bars on right hand chart):

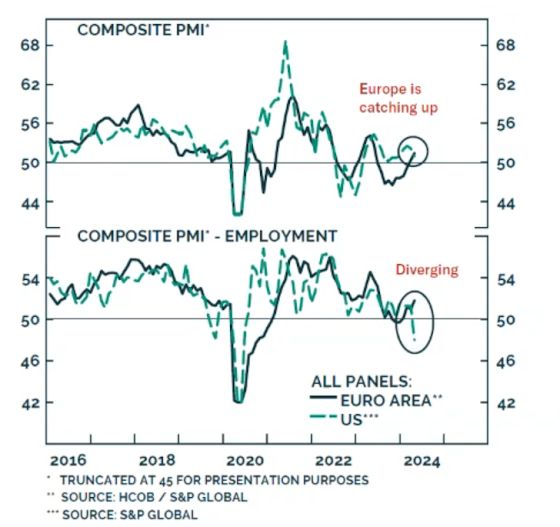

And here’s the latest PMI data showing the US rolling over (composite, and employment) while Europe’s turning up.

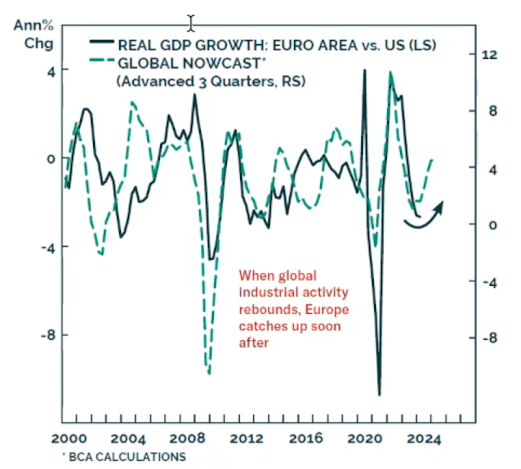

BCA’s “Global Nowcast” and Euro Area vs US real GDP:

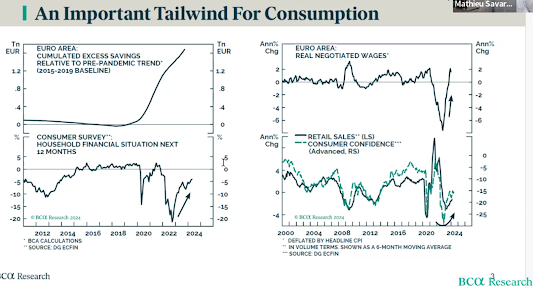

Euro Area consumer data looking up as well:

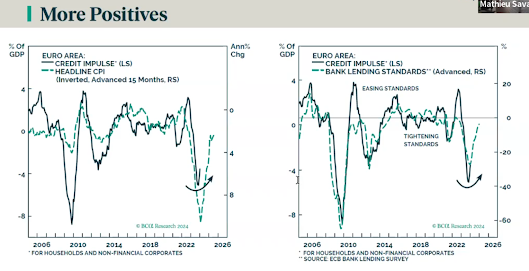

The Euro Zone credit impulse is also looking up

Lastly, I can’t emphasize enough – as I’ve illustrated herein – how history shows that a brief acceleration in growth is not at all unusual just before we head into recession… I.e., we have to be cognizant of the head-fake risk right here.

Today, Tuesday 5/27/24

The soft-landing narrative is anything but implausible, nor is it unprecedented, indeed, we had one in the mid 1990s, and that is what Wall Street is unabashedly counting on.

Thing is, while not unprecedented, it is anything but the norm following a fed tightening cycle and amid the resolution of an inverted yield curve – to name just two present-day dynamics.

BCA’s Peter Berezin did a nice job last Friday laying out what, in his team’s view, it’ll take to achieve the elusive soft landing.

In a nutshell, per the below, to stick an overall soft landing, soft landings will have to occur in the labor market, in discretionary (personal and business) spending, in the credit markets and with regard to inflation… Plus growth needs to improve (or keep improving) outside the US.

As for our view, we in essence concur, as our main barometer consisting of 46 inputs (PWA Index) presently scores a -26, with 20% of our inputs scoring positive, 46% negative, 34% neutral… So, yes, in our view odds favor recession over continued expansion going forward.

When I break down the key areas BCA highlights, our concern over labor market dynamics is that, while, at the moment, the labor market remains healthy, some leading indicators – while still not at recession levels – have reversed direction at a rate of change that has our attention.

As for discretionary spending, while most indications are that those in, say, the upper half of incomes and who hold assets are still spending at an economically-supportive pace, those who live paycheck to paycheck, who carry credit card balances and who don’t hold significant assets are indeed suffering; as evidenced by rising credit card and auto loan delinquency rates…

Granted, more of the nation’s consumption happens in that upper half of incomes, the latter dynamic, however, can be viewed as a potential warning (or pre-recession) sign of what’s to come in the broader economy.

As for credit markets, spreads, for example, remain at comfortably low levels… Although, at the lower end of the credit quality spectrum stress is beginning to build… Same, as above, can be said with regard to potential early warning signs.

With regard to inflation, we do see it declining as the economy weakens, which we believe will embolden equity market bulls – i.e., we’re not short-term bearish on stocks… However, as the economy weakens further, we indeed see equities giving way, amid disappointing corporate earnings and historically-high valuations.

With regard to global growth improving: Indeed we’re seeing it in economic surprise indices and in emerging data coming from a number of venues, the Euro Zone in particular… Question being, is it sustainable, or is it a head fake? While of course it remains to be seen, and while we’re open to the notion that it is sustainable, pre-recession head fakes are not at all unusual, historically-speaking.

A further note on inflation: While we see it dissipating as the economy weakens, we believe it comes quickly back to the fore as we emerge from the next recession… Structural forces virtually ensure that the next cycle will be characterized by notably higher inflation than folks have grown accustomed to the past few decades… Which, frankly, makes for a very rich global macro investment environment… Just have to get through the present cycle first.

And, lastly/importantly, while we see the above as a solid thesis, we have to remain open to the, albeit slim, chance that indeed we are seeing a mid-90s repeat… Which keeps us invested (gaining for the time being), while remaining hedged, and relatively liquid.

Today, Tuesday 5/27/24

The soft-landing narrative is anything but implausible, nor is it unprecedented, indeed, we had one in the mid 1990s, and that is what Wall Street is unabashedly counting on.

Thing is, while not unprecedented, it is anything but the norm following a fed tightening cycle and amid the resolution of an inverted yield curve – to name just two present-day dynamics.

BCA’s Peter Berezin did a nice job last Friday laying out what, in his team’s view, it’ll take to achieve the elusive soft landing.

In a nutshell, per the below, to stick an overall soft landing, soft landings will have to occur in the labor market, in discretionary (personal and business) spending, in the credit markets and with regard to inflation… Plus growth needs to improve (or keep improving) outside the US.

“Many things need to go right to avert a recession: The labor market needs to rebalance, cyclical spending needs to stabilize, loan delinquency rates need to stop rising, inflation needs to fall back to target, and growth in the rest of the world needs to improve.”I like the way they’ve distinguished key areas of focus… In sum, they give a soft landing 20% odds… In other words, they assign an 80% chance that we see recession in the not-too-distant offing.

As for our view, we in essence concur, as our main barometer consisting of 46 inputs (PWA Index) presently scores a -26, with 20% of our inputs scoring positive, 46% negative, 34% neutral… So, yes, in our view odds favor recession over continued expansion going forward.

When I break down the key areas BCA highlights, our concern over labor market dynamics is that, while, at the moment, the labor market remains healthy, some leading indicators – while still not at recession levels – have reversed direction at a rate of change that has our attention.

As for discretionary spending, while most indications are that those in, say, the upper half of incomes and who hold assets are still spending at an economically-supportive pace, those who live paycheck to paycheck, who carry credit card balances and who don’t hold significant assets are indeed suffering; as evidenced by rising credit card and auto loan delinquency rates…

Granted, more of the nation’s consumption happens in that upper half of incomes, the latter dynamic, however, can be viewed as a potential warning (or pre-recession) sign of what’s to come in the broader economy.

As for credit markets, spreads, for example, remain at comfortably low levels… Although, at the lower end of the credit quality spectrum stress is beginning to build… Same, as above, can be said with regard to potential early warning signs.

With regard to inflation, we do see it declining as the economy weakens, which we believe will embolden equity market bulls – i.e., we’re not short-term bearish on stocks… However, as the economy weakens further, we indeed see equities giving way, amid disappointing corporate earnings and historically-high valuations.

With regard to global growth improving: Indeed we’re seeing it in economic surprise indices and in emerging data coming from a number of venues, the Euro Zone in particular… Question being, is it sustainable, or is it a head fake? While of course it remains to be seen, and while we’re open to the notion that it is sustainable, pre-recession head fakes are not at all unusual, historically-speaking.

A further note on inflation: While we see it dissipating as the economy weakens, we believe it comes quickly back to the fore as we emerge from the next recession… Structural forces virtually ensure that the next cycle will be characterized by notably higher inflation than folks have grown accustomed to the past few decades… Which, frankly, makes for a very rich global macro investment environment… Just have to get through the present cycle first.

And, lastly/importantly, while we see the above as a solid thesis, we have to remain open to the, albeit slim, chance that indeed we are seeing a mid-90s repeat… Which keeps us invested (gaining for the time being), while remaining hedged, and relatively liquid.

No comments:

Post a Comment