In the meantime, here are the visuals I had loaded up for this week, with some commentary:

Housing data say we’re not out of the woods, despite Wall Street's insistence.

Yesterday’s homebuilder sentiment reading (at 39 [under 50 = contraction]) was, let's say, not optimistic!

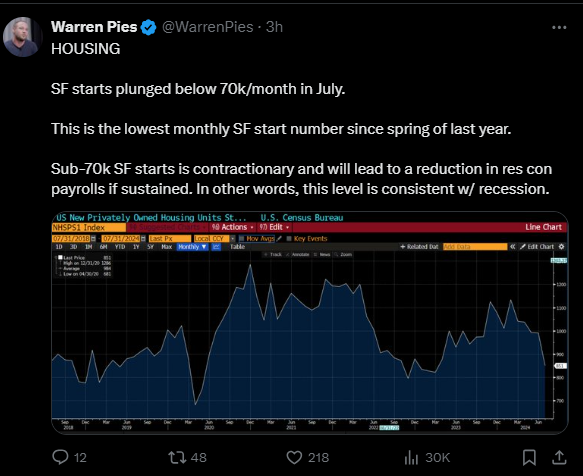

Plus:

Which typically (“if sustained”) spells recession:

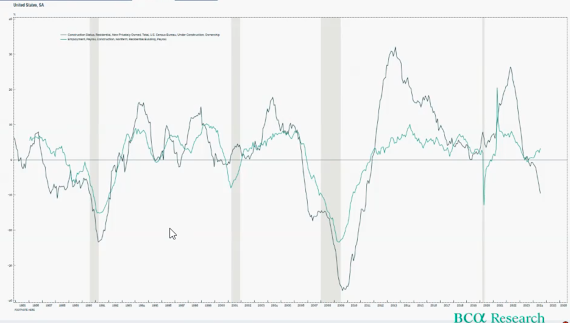

Here’s BCA this morning pointing to that historic link between units under construction and construction employment… Suggesting that the green line (employment) is at risk of heading lower going forward (grey areas highlight recessions):

The lumber chart agrees:

July retail sales were better than expected... And while the year-on-year number was nothing to throw a party over, this data simply doesn't spell recession looming (although, per the yellow circles below, a last-breath surge right before recession is kind of the norm), which was loved by traders who recently went from panic to fomo (fear of missing out) mode:

Initial jobless claims came in lower than expected, the market loved that too, but the trend remains a serious warning sign:

Industrial production rolled back over, as the manufacturing space remains in recession:

Factory capacity utilization:

Factory capacity utilization:

Commercial and Industrial loans are back to contracting:

Caterpillar global sales are concerning (save for in Latin America):

Caterpillar global sales are concerning (save for in Latin America):

Economic Surprise Indices reflect what we've seen of late.

US:

Global:

Inflation (CPI) came in below expectations:

Copper's bucked the downtrend (a bit) of late, but remains in a notably bearish trend:

US:

Global:

Inflation (CPI) came in below expectations:

Copper's bucked the downtrend (a bit) of late, but remains in a notably bearish trend:

The stock/bond ratio utterly plummeted over the past month (concerning!):

Stocks just finished their best week of the year, yet there's still a notably bearish setup displayed by the SP500 weekly chart:

Bottom line, on net, economic risk remains quite elevated right here.

As for the equity market, per last Monday's video, the snapback rally should be of no surprise to anybody... And, indeed, testing, if not recapturing, the recently-established all time high is a distinct possibility.

Bottom line, on net, economic risk remains quite elevated right here.

As for the equity market, per last Monday's video, the snapback rally should be of no surprise to anybody... And, indeed, testing, if not recapturing, the recently-established all time high is a distinct possibility.

So what about the bull market’s durability from here, given current valuation levels and macro dynamics?

Well, not so much.

Stay tuned...

Well, not so much.

Stay tuned...

No comments:

Post a Comment