But first a quote:

“The only way to make money in the markets is to be patient, disciplined and informed. You have to have the confidence to make decisions based on sound analysis and rational thought.” --David Shaw

While I believe we're less-sanguine on the economy right here than is Bob Elliott, I find his analysis to be spot on... I.e., the conditions priced into US equities are virtually untenable in the foreseeable future.

@BobEUnlimited

US stocks don't have an earnings problem, they have an expectations problem. With expectations of 3% real gdp in 2H24, earnings growth to reach 16% y/y by end of '25, and an AI boom ahead driving 21x multiples, such lofty expectations are a setup for disappointment.

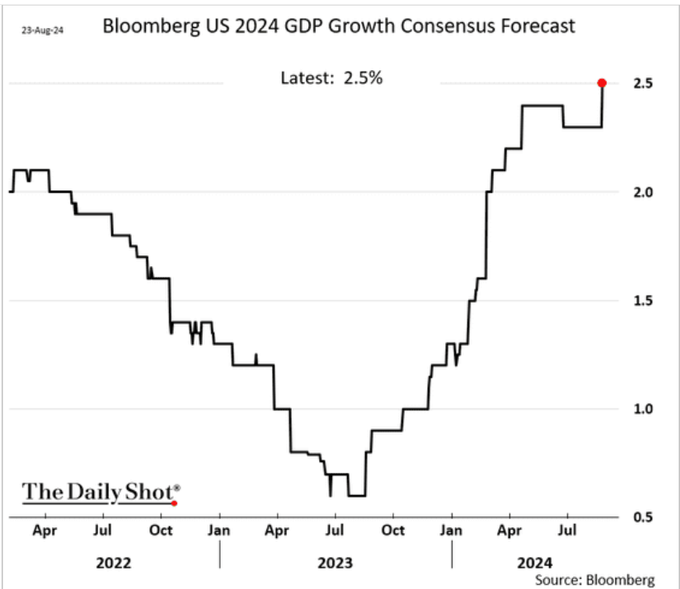

In the short-term, growth expectations in the US economy remain very strong through the end of the year.

Achieving 2.5% growth over the full year given ~2% prints in 1Q & 2Q requires a near 3% growth in the 2H24, which is very strong.

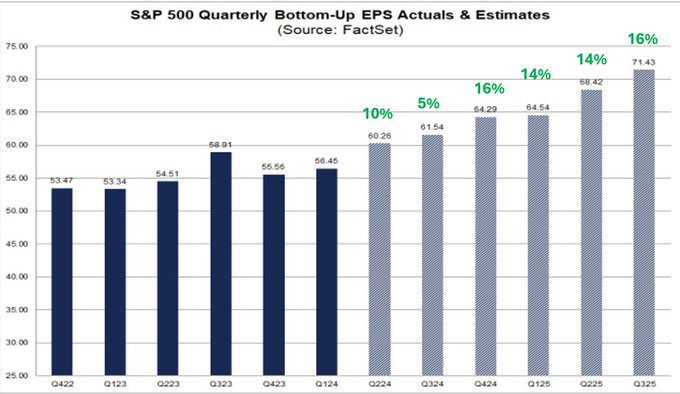

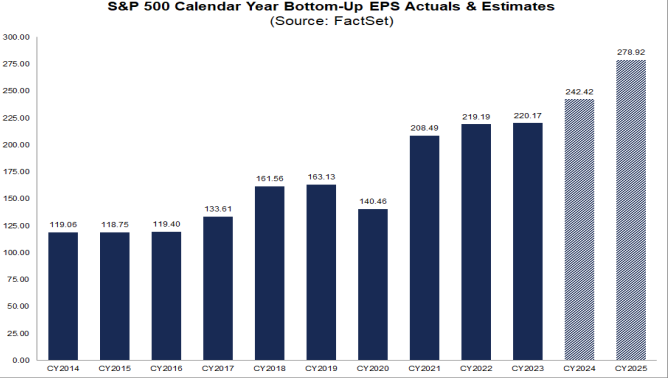

Earnings expectations are elevated in the medium-term as well. This quarter's earnings represented the first meaningful positive earnings growth in awhile, but after a brief pause next quarter, earnings are expected to grow rapidly thru the end of '25.

With revenue growth expected at roughly 5-6% thru the end of '25 (not too far off of US nominal GDP today so indicating no slowdown in growth), getting 15%+ earnings growth is going to require a surge in margins to secular highs by the end of '25.

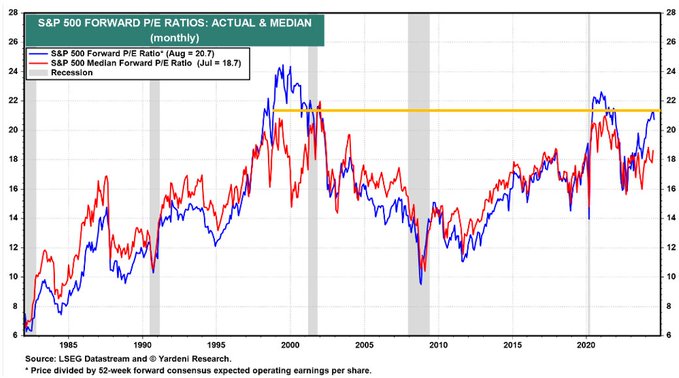

But its not just earnings growth expectations over the medium-term, US equity markets are pricing in extraordinary growth over the longer-term as well, with PEs today running just off of all time highs.

Techno-optimists argue that this elevated long-term valuation is often rationalized by making the case that AI is likely to have a revolutionary impact on companies and bring about a totally new wave of productivity growth and investment.

But as I've noted before, even an AI investment boom and extraordinary productivity isn't close to enough to justify this AI-optimism pricing.

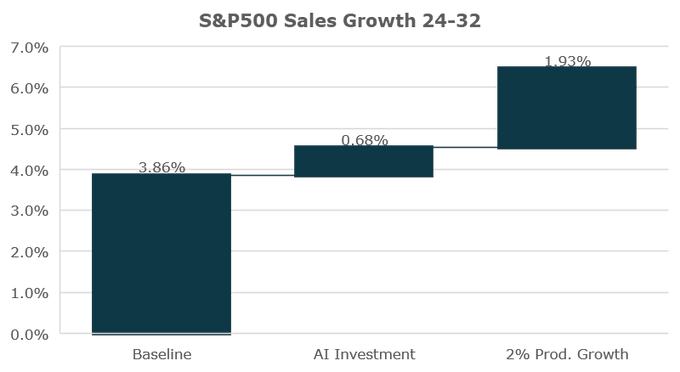

Taking those pieces together would lead to S&P500 companies revenue growth going from about 4% to about 6.5%. Certainly impactful over a near decade long timeframe, but not game changing.

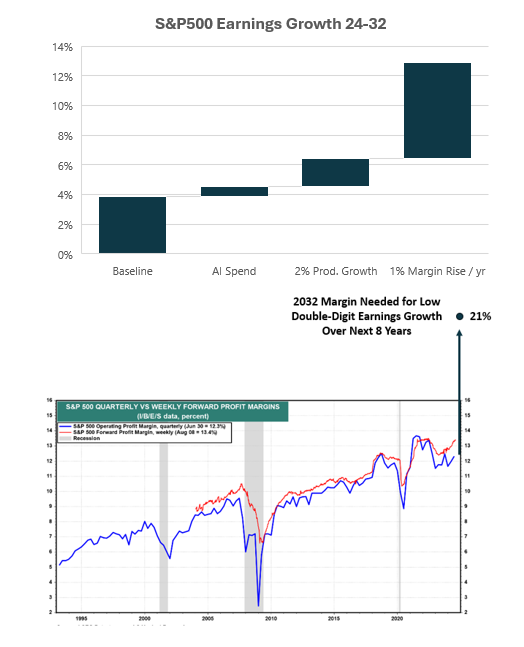

In order to get close to the double digit earnings rises often promoted by the techno-optimists over the next decade or so, not just an investment and productivity boom, but an expansion in margins at a pace multiples of what we've ever seen in history.

The challenge with this that the techno-optimists almost always don't have a good answer to is that because companies margin expansion means less income for labor, this type of jump would require some other sector to shift their rate of dissaving by ~6% of GDP /yr *forever*.

8/26/2024

@BobEUnlimited

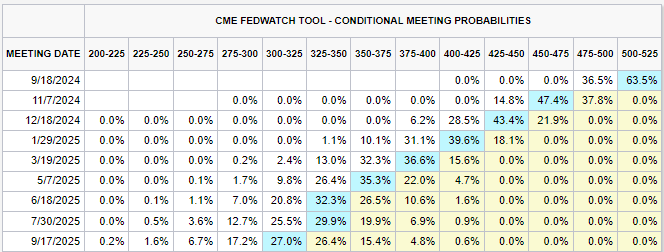

Markets pricing and pundit euphoria about a soft landing reached a fevered pitch following JP's JH speech on Friday. While a cut is the next step, it is very unlikely that 200bps of cuts and mid-double digit earnings growth will come together in the next 12m.

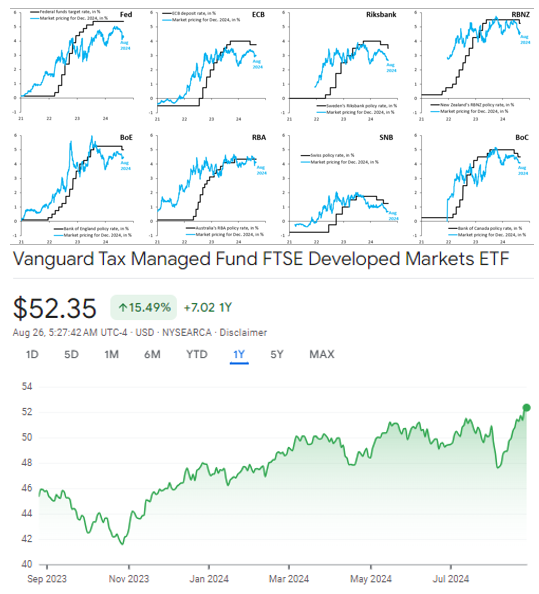

At this point the short-rate markets are pricing in an aggressive cutting cycle, with a 2/3 probability of 50bps on Sept, more than 100bps thru year end, and 200bps of cuts in under a year.

And the US 2yr note is back at levels seen in the fall of 2022, when for context the target rate was at 2.5%.

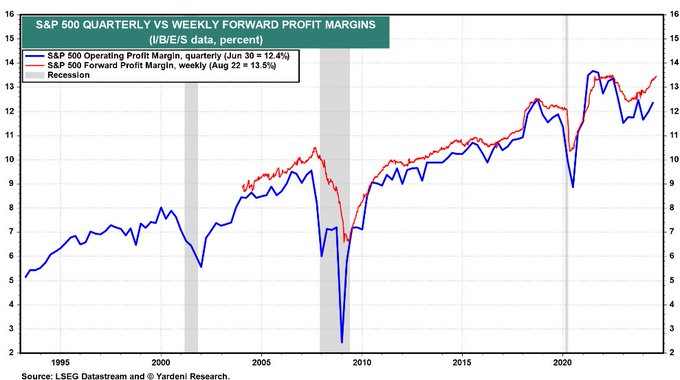

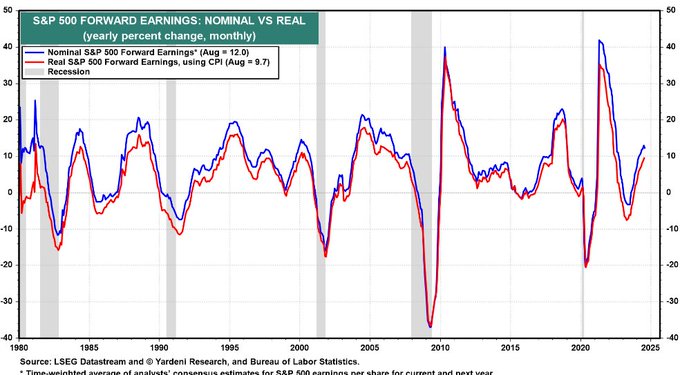

At the same time nominal forward earnings are expected to grow at roughly 12% over the next 12m. With nominal sales growth expected to run at around 5-6% for the foreseeable future, this requires margins pushing well above all time highs.

And calendar year '25 earnings are expected to grow at 15%.

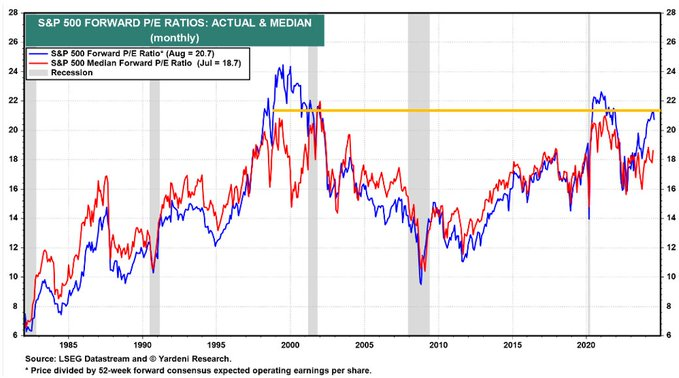

On top of that, investors are paying 21.1x those already elevated expectations of forward earnings. Only meaningfully eclipsed by the most extreme bubble period when PEs reached 24.

While the US is the most extreme case, the broad brush strokes across most developed markets are the same. With significant cuts priced in everywhere thru the end of the year and beyond while stocks push to new highs.

While soft landing pricing has been broadly in place for many months now, the last few weeks have been particularly notable b/c stocks are back to highs but the expectations of cuts increased dramatically. We are above the early July highs *and* 2yrs have fallen almost 100bps.

While the next move is almost certainly a shift to cuts pretty much for every developed central bank (ex-BoJ), the magnitude of the cuts that are going to come are by no means clear at this point. Nearly all claim to be data dependent rather than setting out a clear pace.

8/24/2024

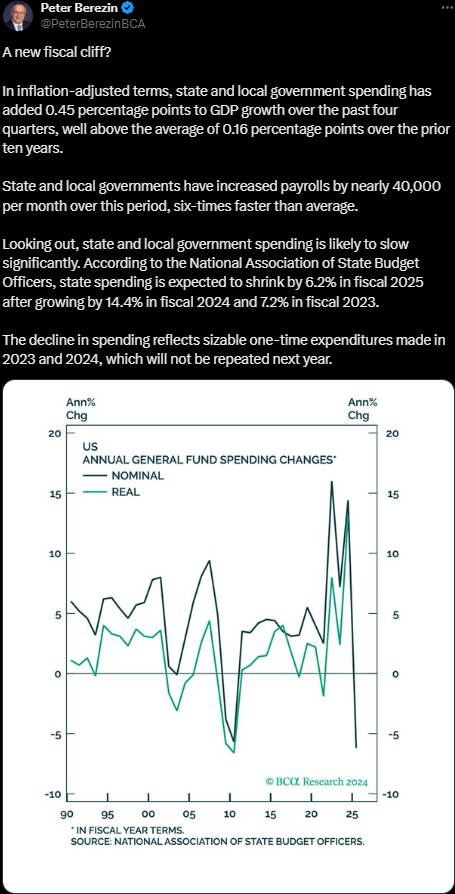

State and local governments will be very hard-pressed to maintain present pace:

8/23/2024

As we've state ad nauseum of late, rate cuts -- if recession ensues -- are typically not bullish for equities:

8/22/2024

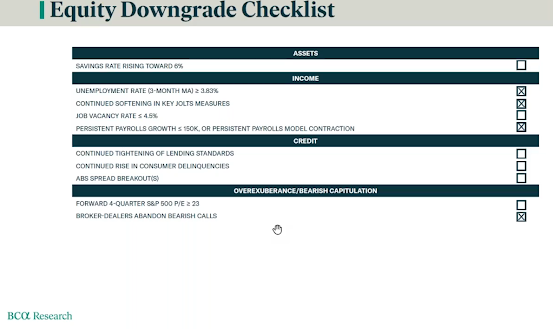

BCA's US Equity team, after nailing it last year, have turned bearish:

8/21/2024

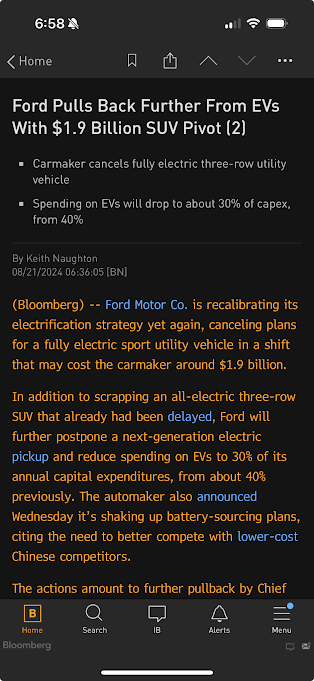

Ford's latest jibes with our palladium position:

8/21/2024

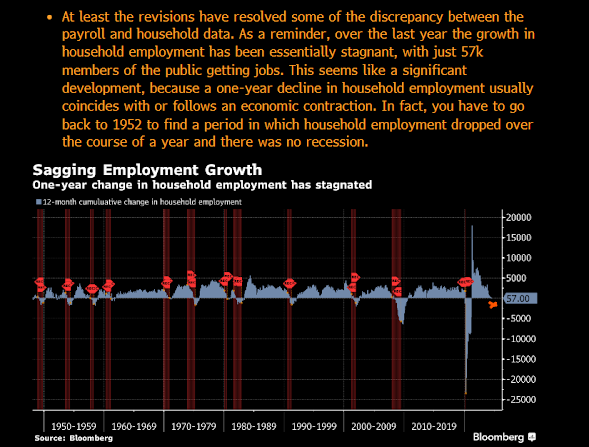

Re; payroll revision:

No comments:

Post a Comment