But first, a quote:

“Acting in excessive reliance on the fact that something ‘should happen’ can kill you when it doesn’t. That’s why I always remind people about the 6-foot-tall man who drowned crossing the stream that was 5 feet deep on average. You have to be able to get through the low points. And the success of your investment actions shouldn’t depend on normal outcomes prevailing; instead, you must allow for outliers.” —Howard Marks8/6/2024

Today’s big snapback rally made perfect sense, if only technically.

US equity futures were in the red this evening, until the BOJ’s Uchida chimed in with “we won’t raise rates when market is unstable.” Which, given the narrative around the recent selloff (yen carry trade unwinds), sent global equity markets (US futures included) sharply into the green, and the yen notably into the red.

Bloomberg’s Mark Cranfield (below) believes the market celebration will be short-lived as traders wake up to the fact that a dovish BOJ gives an even greener light (as if they needed one) for the Fed to cut come September.

“Japanese equities are higher, the yen is lower and JGBs a touch firmer on dovish comments from BOJ’s Uchida. Investors are taking this to signal the BOJ is on hold for a while, but there was never much chance of a hike in September anyway. If there is going to be another increase it was always more likely in the fourth quarter and there is plenty of time for markets to stabilize before then.”I get it, and it’s the kind of phenomenon that could indeed break something, but, in my view, the go-forward (next several months) serious risk to equities is a US recession… Under no scenario are US stocks priced for that risk right here.

“USD/JPY is climbing on a view the Bank of Japan may go into a holding pattern on interest rates, which shifts the swing factor to the Federal Reserve. For now the Fed is near certain to cut rates, possibly with a jumbo move next month to avoid making changes too close to the US elections.

As traders digest all of that, it could mean a reversal for USD/JPY’s early gain.” --Mark Cranfield

8/5/2024

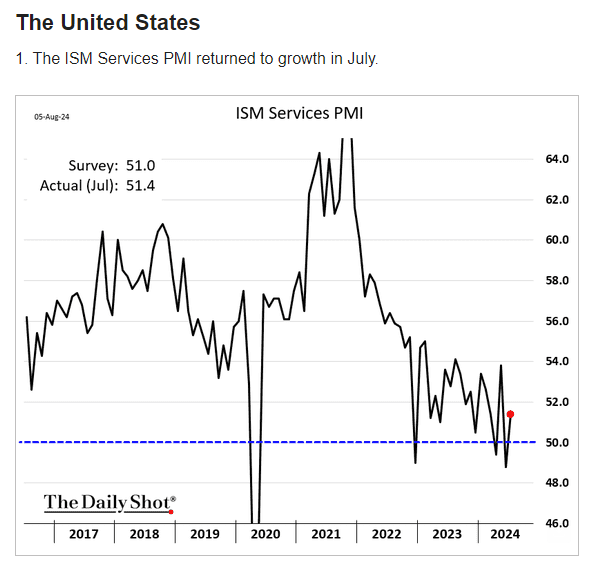

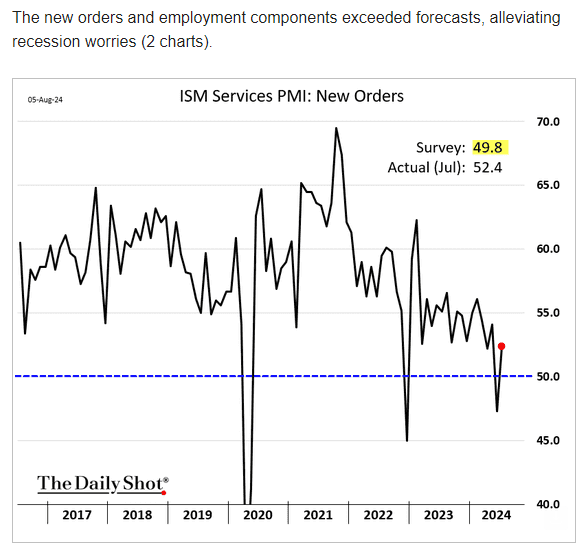

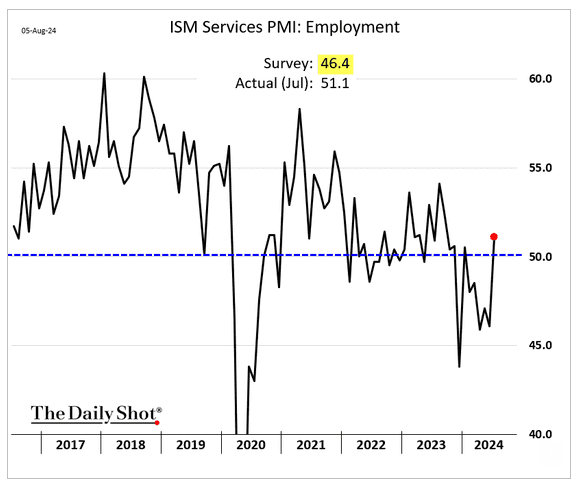

July’s ISM Services Sector Survey took a bit of the sting off of the recession narrative, somewhat countering last week’s weak manufacturing survey:

However, with just 10 of the 18 sectors reporting growth, and considering the following from the ISM Chair, the report – while, again, a net-positive signal – wasn’t hugely inspiring.

“The increase in the composite index in July is a result of an average increase of 5 percentage points for the Business Activity, New Orders, and Employment indexes, offset by the 4.6-point drop in the Supplier Deliveries Index. The last time Supplier Deliveries was in contraction (faster) territory while the other three indexes registered expansion was in November 2023.

Survey respondents again reported that increased costs are impacting their businesses, with generally positive commentary on business activity being flat or expanding gradually. Comments continued to express a wait-and-see attitude regarding the upcoming presidential election, with one respondent expressing concern over potential increases in tariffs. Many panelists noted a return to more stable supply chain performance, albeit with higher costs.”

8/4/2024

Just finished scoring our Equity Market Conditions Index (EMCI) as of 7/31… It scored a -66.67, which means conditions reflect a notably unfavorable risk/reward setup right here.

Here’s my brief narrative from the report:

July was quite the month for equity markets… The overwhelming theme being a massive broadening out rotation, where the laggards on the year played serious catchup to the handful of tech stocks that were previously doing all of the heavy lifting.

Of course the question now being, are we seeing a sustainable rotation amid an ongoing expansion (as the bulls suggest), or is this a bull-trap-head-fake, the likes of which are typical of topping markets?

Our base case – given our current macro view – is the latter.

And here’s how the components lined up:

Inputs that showed improvement:

Breadth (from negative to neutral)

Inputs that deteriorated:

US Dollar (positive to neutral)

Interest Rates, Liquidity and Overall Financial Conditions (from positive to negative)

Inputs that remained bullish:

None

Inputs that remained bearish:

Valuation

Sector Leadership

Economic Conditions

SPX Technical Trends

Sentiment

Inputs that remained neutral:

Fiscal Policy

8/4/2024

Buffett's cash level says something:

8/3/2024

BREAKING NEWS: WARREN BUFFETT SOLD A LOT OF APPLE DURING Q2

Warren Buffett and Berkshire Hathaway $BRK.B currently own ~$84.2 Billion worth of Apple $AAPL as of the end of Q2 down from $135.4B worth as of the end of Q1

8/3/2024

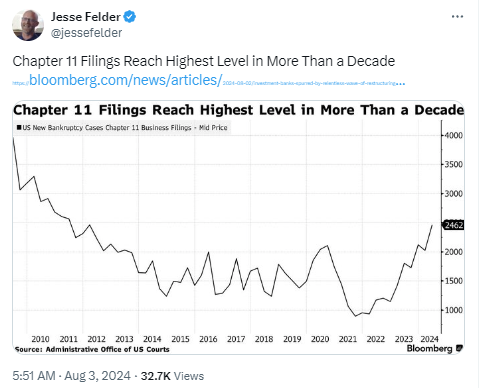

BK filings jibe with our present economic concerns:

8/2/2024

As I suggested yesterday, today’s jobs report would be telling in terms of whether sentiment has indeed shifted to a bad-news-is-bad-news scenario, in which case recession – as opposed to soft landing – is becoming the market’s base case.

As I type, the Dow is off the morning lows, but still down 800 points, SPX -2.2%, NDX -2.6%.

So, yes, at least for the moment, the market shift reflects the reality that valuations, and earnings expectations, are simply way too stretched in a recession scenario.

Wall Street banks are out this morning – as we’d expect – telling the market to expect 100 bps in Fed cuts by November… Which no doubt explains the slight bounce off the morning lows.

In the coming weeks we’ll very likely see more such volatility in both directions (yes, we’ll see some rip your face off rallies [like Wednesday] – as is virtually always the case at cycle tops) as the market adjusts to fundamental reality.

Also, as we anticipated, the yen is, far and away, acting as the currency of choice as the global economy, and markets, weaken.

8/1/2024

Much of the action of late has suggested that market sentiment may be shifting to what we ultimately expect as the rest of the current cycle plays itself out… Specifically, that bad economic news is indeed bad news for stocks, as recessionary conditions will dramatically re-rate earnings expectations and, therefore, stocks would see quite the downside adjustment.

Yesterday’s action, however, bucked that developing trend… I.e., stocks rallied hard as yields declined notably… Suggesting that a weak economy is, at the moment, good news for stocks, as it would for certain have the Fed cutting interest rates.

This morning’s action, on the other hand, and in pronounced fashion, goes back to suggesting that we may indeed be crossing into the fundamentally-valid sentiment that bad economic news is bad news for corporate earnings, and that present stock valuations do not remotely reflect anything but rising earnings ad infinitum.

In essence, the labor data is indeed showing cracks, particularly in the PMIs… Sending those telltale signals that recession risk is definitely not-small going forward… And, thus, as history suggests, markets understand that, in that scenario, Fed rate cuts tend not to keep markets from properly discounting fundamental reality.

Stocks (the major averages) are down notably as I type – Dow by 500 pts, SPX by 1.2%, NDX by 1.9%... While treasury bonds, US utility, healthcare and staples stocks are all green on the morning (that’s a sector performance mix that reflects weak economic sentiment).

Suffice to say that, while AMD’s earnings certainly didn’t hurt, yesterday’s rally was pretty much about Fed speak that virtually assured a September rate cut is coming, without considering the actual reasons why they’d be cutting.

The featured respondents’ commentary in the July ISM Manufacturing survey tells the story:

“Business is relatively flat — the same volume, but smaller orders.” [Chemical Products]

“Demand continued to soften into the second half of the year. Supply chain pipelines and inventories remain full, reducing the need for overtime. Geopolitical issues between China and Taiwan as well as the election in November remain weighing concerns.” [Transportation Equipment]

“Even though we are used to a seasonal reduction in business over the summer, consumer behavior is changing more than normal. Sales are lighter, and customer orders are coming in under forecasts. It seems consumers are starting to pull back on spending.” [Food, Beverage & Tobacco Products]

“Availability of parts is good, with small exceptions of missing materials here and there. Ordering is still well below typical levels as we continue to burn down inventory of raw goods, with ‘normal’ ordering trends expected to return sometime in the second half of 2024.” [Computer & Electronic Products]

“It seems that the economy is slowing down significantly. The number of sales calls received from new suppliers is increasing significantly. Our own order backlog is also diminishing. We are hoping for an increase in customer demand, or we will possibly need to make organizational changes.” [Machinery]

“Unfortunately, our business is experiencing the sharpest decline in order levels in a year. We were well below our budget target in June; as a result, it was the first month this year that we had negative net income.” [Fabricated Metal Products]

“Business is slowing, and we are taking cost actions.” [Electrical Equipment, Appliances & Components]

“Some markets that are usually unwavering are showing weakness. Weather is the common factor, but only so much.” [Nonmetallic Mineral Products]

“Our sales forecast for July and August are slow, but we’re making every attempt to remedy that situation. Our medical end-user customers continue to meet their forecasts, which is promising.” [Textile Mills]

“Elevated financing costs have dampened demand for residential investment. This has reduced our need for component products and inventory.” [Wood Products]

Here’s Peter Boockvar with more on the jobs front:

Initial jobless claims rose to 249k from 235k, the highest one week print since August 2023 and that was 13k more than expected. This brings the 4 week average to 238k from 236k and that is just below the highest since last summer. Continuing claims rose to 1.877mm, the most since November 2021 and up from 1.844mm in the week before.

Bottom line, the US labor market continues to soften.

Also out and confirming this, the Challenger report saw a drop in job cuts m/o/m but a rise by 9% y/o/y. Also, the announced hirings fell to the lowest monthly total since December 2023 and it is the slowest July since they started calculating hirings in 2009. They said, “The job market is indeed cooling, with hiring at the lowest point in over a decade. While we are seeing increased cuts in manufacturing sectors, both consumer and industrial, most industries are cutting below last year’s levels.” Tech continues to lead the pace of job cuts but has slowed by half from what was seen in 2023. So while there has been a rise in initial jobless claims, there still seems to be a desire to stick with ones employees as much as they can.

‘Why are Companies Cutting?’ asks Challenger, “Cost cutting is the leading cause for job cuts in July.” Don’t blame AI, “Companies have not cited technology, with AI directly or due to ‘technological’ update for any job cuts since April.”

How markets respond to tomorrow’s jobs report will be telling.

No comments:

Post a Comment