Here are the highlights:

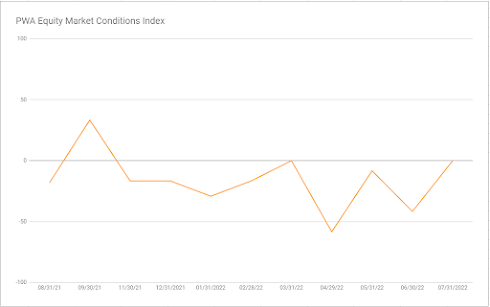

07/29/2022 PWA EQUITY MARKET CONDITIONS (EMCI) INDEX: 0

(from -41.67 on 6/30/2022)

Our EMCI’s advance from -42 to end June to 0 at the end of July is substantial -- reflecting measurable improvement in general equity market conditions over the past few weeks.

Inputs that showed improvement:

Interest Rates (positive from neutral)

Sector Leadership (positive from negative)

SPX Technical Trend (neutral from negative)

Breadth (positive from neutral)

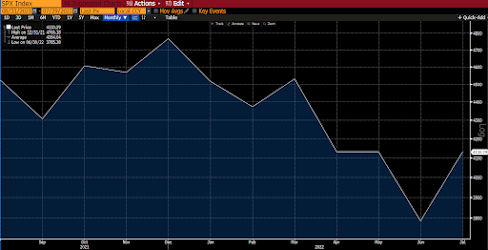

SP500 since EMCI inception:

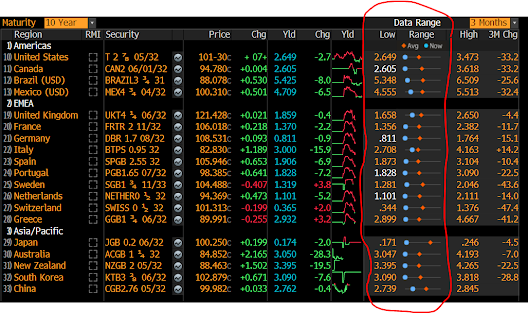

The 10-year treasury yield currently looks to be failing its recent breakout above a very long-term down trend:

Global sovereign 10-year yields are falling in unison:

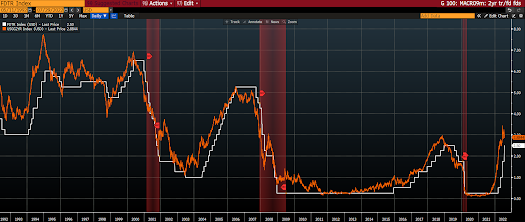

The 2yr treasury/Fed Funds spread is collapsing (market anticipating a softer Fed going forward):

Asian equities were positive overnight, with 14 of the 16 markets we track closing higher.

Europe's a bit off so far this morning, with 10 of the 19 bourses we follow trading down as I type.

US stocks are weak to start the session: Dow down 178 points (0.54%), SP500 down 0.79%, SP500 Equal Weight down 1.00%, Nasdaq 100 down 0.74%, Nasdaq Comp down 0.81%, Russell 2000 down 1.19%.

The VIX sits at 22.80, up 6.84%.

Oil futures are down 5.35%, gold's up 0.45%, silver's flat, copper futures are down 1.33% and the ag complex (DBA) is down 1.56%.

The 10-year treasury is up (yield down) and the dollar is down 0.41%.

Among our 35 core positions (excluding options hedges, cash and short-term bond ETF), 10 -- led by carbon credits, treasury bonds, Dutch Bros, Nokia, gold and consumer staples stocks -- are in the green so far this morning. The losers are being led lower by energy stocks, uranium miners, base metals miners, Sweden equities and Disney.

Marty

07/29/2022 PWA EQUITY MARKET CONDITIONS (EMCI) INDEX: 0

(from -41.67 on 6/30/2022)

Our EMCI’s advance from -42 to end June to 0 at the end of July is substantial -- reflecting measurable improvement in general equity market conditions over the past few weeks.

Inputs that showed improvement:

Interest Rates (positive from neutral)

Sector Leadership (positive from negative)

SPX Technical Trend (neutral from negative)

Breadth (positive from neutral)

Inputs that deteriorated:

none

Inputs that remained bullish:

Dollar

Sentiment

Inputs that remained bearish:

Fed Policy

Valuation

Economic Conditions

Geopolitics

Credit Market Conditions

none

Inputs that remained bullish:

Dollar

Sentiment

Inputs that remained bearish:

Fed Policy

Valuation

Economic Conditions

Geopolitics

Credit Market Conditions

Inputs that remained neutral:

Fiscal Policy

EMCI inception (8/21/2021):

Fiscal Policy

EMCI inception (8/21/2021):

SP500 since EMCI inception:

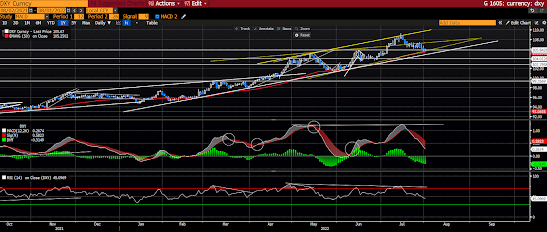

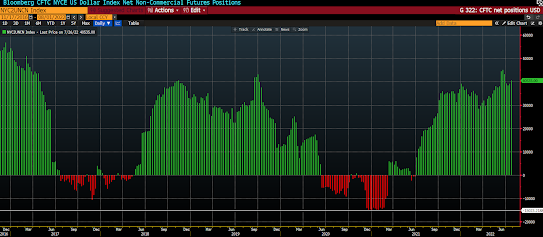

We recognize that our take on the present setups for the dollar and for interest rates may be out of consensus (for the dollar in particular).

Here's why:

The Dollar: We view a weakening dollar as bullish for global equities going forward. Thing is, the dollar sits just off of multi-year highs. So what might have us thinking it'll be weaker going forward?

Well, technically-speaking, negative divergences are forming against a price that is presently testing trendline support and a flattening 50-day moving average... Futures traders sit near a multi-year high net bullish reading... I.e., the dollar trade looks crowded right here, and any one of a number of potential events, including (globally-speaking) shifts in fiscal and/or central bank policy(s), could call its bullish underpinnings into question...

Dollar Index daily chart:

Dollar Index Futures Commitment of Traders Report:

Interest Rates: With inflation at multi-decade highs and a Fed that vows to get it back to their 2% target, what would have us presently scoring our interest rate component positively?

Here's from our internal notes:

The 10-year treasury yield currently looks to be failing its recent breakout above a very long-term down trend:

Global sovereign 10-year yields are falling in unison:

The 2yr treasury/Fed Funds spread is collapsing (market anticipating a softer Fed going forward):

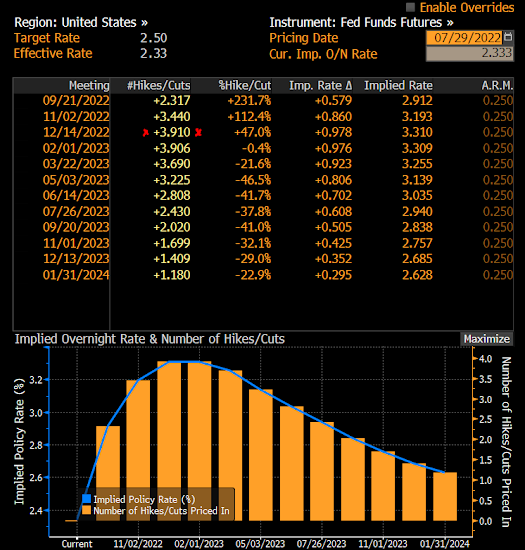

Fed Funds Futures pricing in 4 hikes by the end of 2022 (3 fewer than last month), then cuts beginning March 2023:

Now, keep in mind, while a jump from -42 to 0 is bigly positive, it only moves present conditions from bearish to neutral -- not bullish, mind you, at this juncture... I.e., this is no time to get cute, or to try to be a hero, as serious underlying risks -- atypical of bull market conditions -- remain.

Asian equities were positive overnight, with 14 of the 16 markets we track closing higher.

Europe's a bit off so far this morning, with 10 of the 19 bourses we follow trading down as I type.

US stocks are weak to start the session: Dow down 178 points (0.54%), SP500 down 0.79%, SP500 Equal Weight down 1.00%, Nasdaq 100 down 0.74%, Nasdaq Comp down 0.81%, Russell 2000 down 1.19%.

The VIX sits at 22.80, up 6.84%.

Oil futures are down 5.35%, gold's up 0.45%, silver's flat, copper futures are down 1.33% and the ag complex (DBA) is down 1.56%.

The 10-year treasury is up (yield down) and the dollar is down 0.41%.

Among our 35 core positions (excluding options hedges, cash and short-term bond ETF), 10 -- led by carbon credits, treasury bonds, Dutch Bros, Nokia, gold and consumer staples stocks -- are in the green so far this morning. The losers are being led lower by energy stocks, uranium miners, base metals miners, Sweden equities and Disney.

"What most people and their countries want most is wealth and power, and money and credit are the biggest influences on how wealth and power rise and decline. If you don’t understand how money and credit work, you can’t understand how the system works, and if you don’t understand how the system works, you can’t understand what’s coming at you."

--Dalio, Ray. Principles for Dealing with the Changing World Order

Marty

Marty: Thanks for the market updates!

ReplyDeleteAlways my pleasure Sam!

ReplyDelete