In June 2017, after decades of parsing volumes of economic data, constructing our attendant views and applying them, we decided to create our own index and formally track the data we felt were most telling in terms of giving an on-the-ground, real-time assessment of general conditions.

We then ran it back a ways to determine how revealing it would have been over the past couple of cycles.

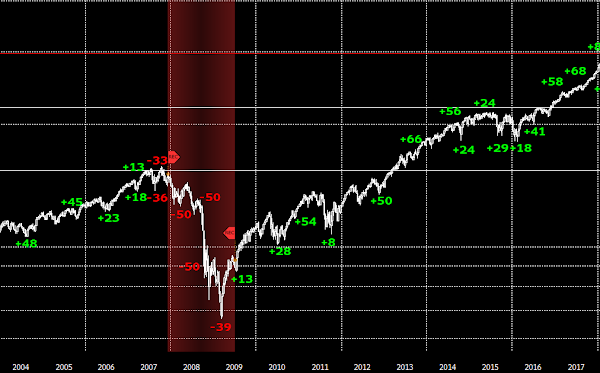

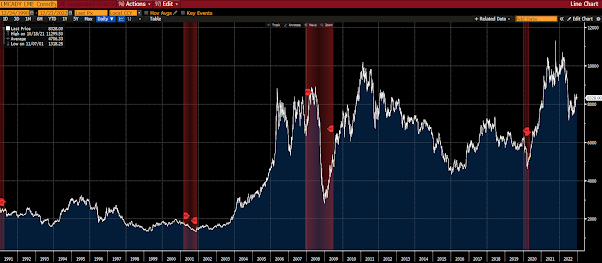

The white line in the graph below represents the S&P 500 Stock Index, the numbers plotted along the line represent the PWA Index's score at the time, the red shaded areas represent recessions:

Let's zoom in.

Here's February 1998 through December 2003:

Here's January 2004 through December 2017:

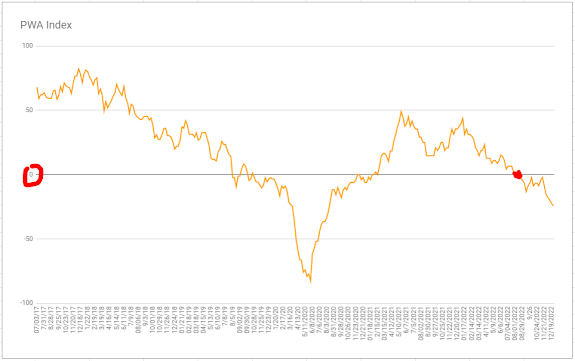

Here's January 2018 to present:

As you can see, our index went into the red ahead of each of the previous 3 recessions and "official" bear markets in stocks (the covid bear market, frankly, as I've explained in video commentaries, didn't satisfy our bear market criteria).

In our most recent experience, our index was not signaling recession ahead of the current bear market, which is why, as it got underway, we -- per the technical analysis I shared on multiple videos during the spring and since -- established ~3,500 as our downside bear market target.

As it turns out, so far, that looks to have been a good call (bounced hard off of 3492 intraday on October 13th and hasn't looked back):

Like I said, "our index was not signaling recession" when we established that downside target for equities... So I was, thus, very careful at the time to provide the caveat that, should our economic assessment deteriorate to the point where recession odds trump further expansion odds going forward, our downside target would, in all likelihood not hold... Here's from our June 17th blog post:

"While our 3,500 S&P 500 downside target continues to make sense to us, suffice to say that global macro conditions are waning to the point that could have us seriously re-thinking that scenario over the coming weeks/months..."

Well, alas, within 2 months, our assessment indeed deteriorated to that point:

Therefore, odds in our view now favor a somewhat lower low before this bear market ultimately plays itself out... I, given the technicals, and our mild recession thesis, flagged 3,200ish on the S&P in a recent video... It sits at 3844 as I type.

If, on the other hand, we're wrong in our go-forward economic assessment, then the worst may indeed already be over... We remain open to all possibilities!

Let's take a quick run through our index's components... I'll highlight according to their respective signals (as we [subjectively] see them) and note where we have a constructive view of a given component... This will have you understanding where we're coming from:

Brick and Mortar Retail Sales:

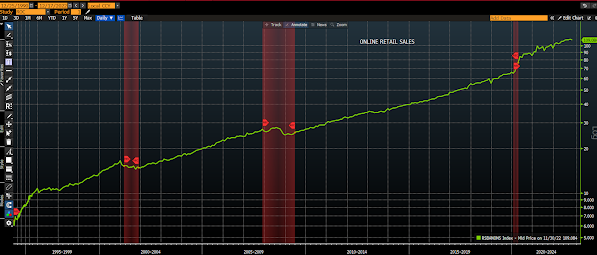

Online Retail Sales:

Auto Sales -- the higher lows since June are encouraging:

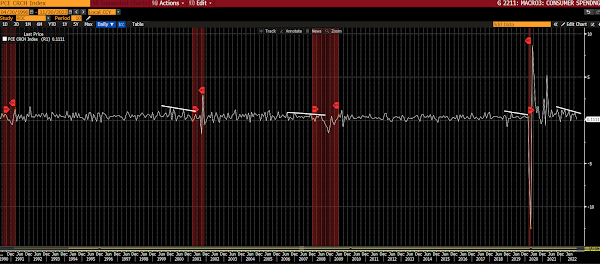

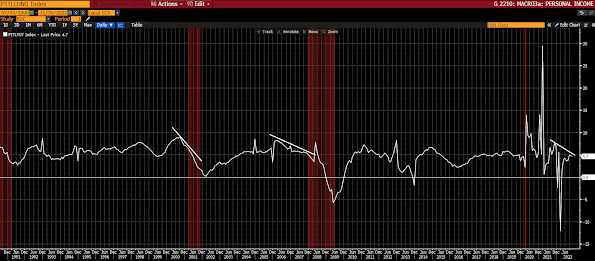

Consumer Spending:

Personal Income:

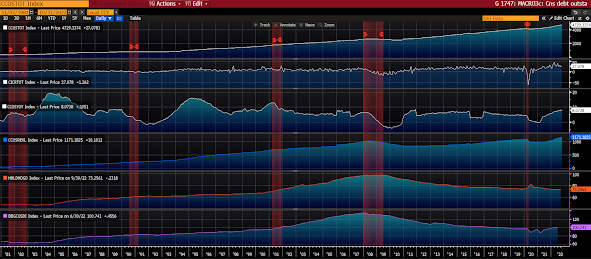

Various Consumer Debt Metrics:

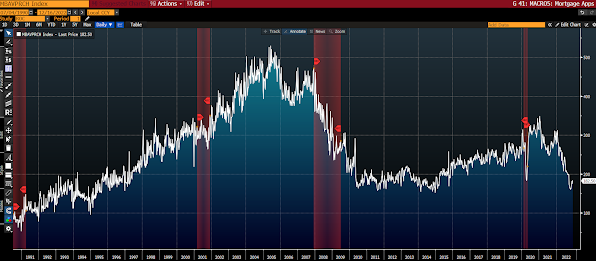

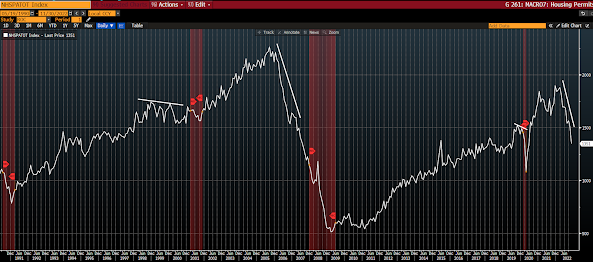

Mortgage Purchase Applications:

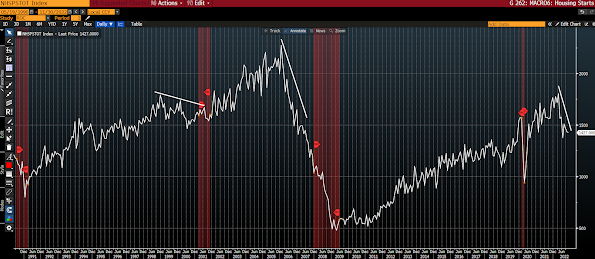

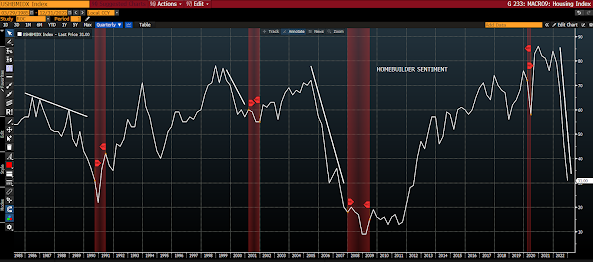

Housing Starts:

Weekly Unemployment Claims -- remain encouraging:

Various Other Employment Metrics -- not signaling recession right here:

Consumer Confidence -- showing marginal improvement of late:

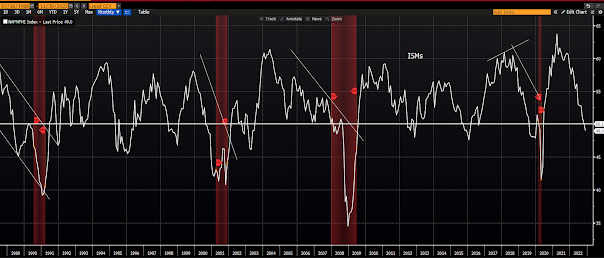

ISM Manufacturing Index:

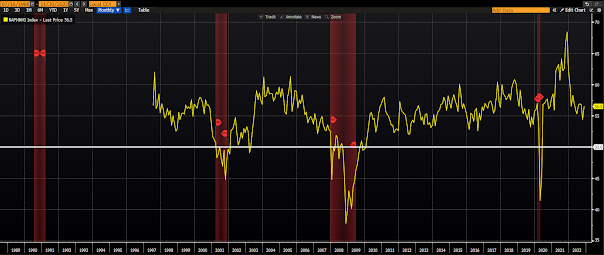

ISM Services Index -- above 50 says continued expansion:

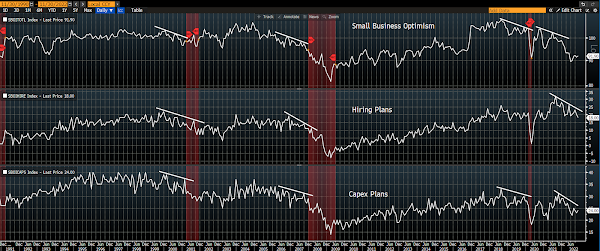

Small Business Sentiment:

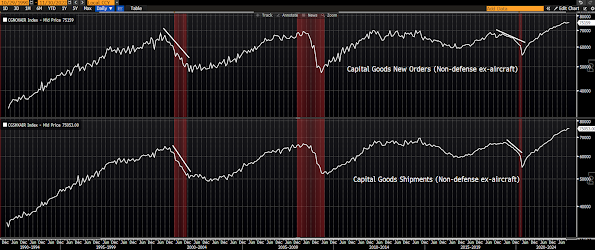

Durable Goods Orders:

Capital Expenditures -- hanging in:

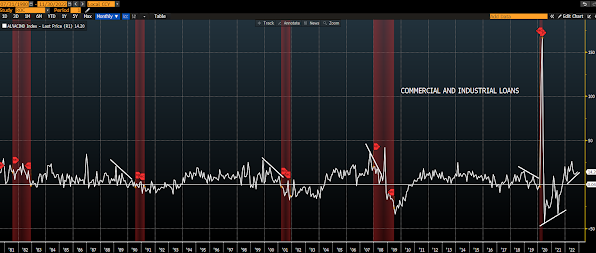

Commercial and Industrial Loans -- constructive:

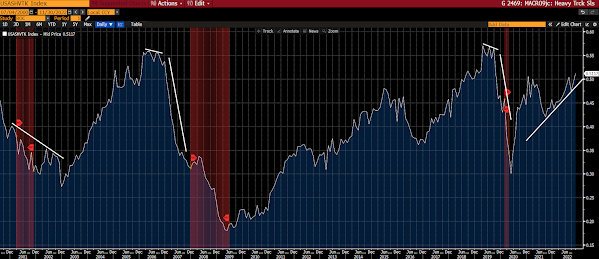

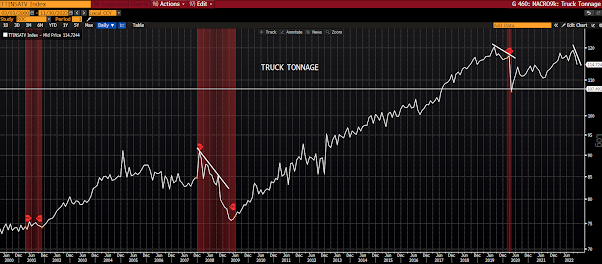

Truck Tonnage:

Cass Freight Index:

Caterpillar Global Sales -- seeing slight growth after declining in Q2:

Global Purchasing Managers Index:

Leading Economic Indicator/Coincident Economic Indicator Ratio:

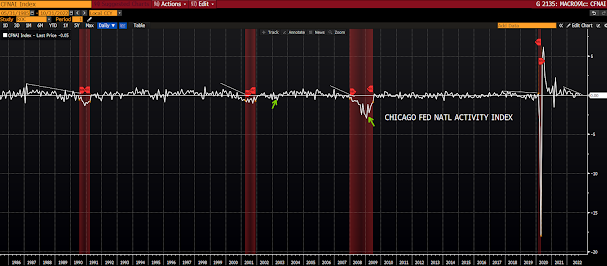

Chicago Fed National Activity Index:

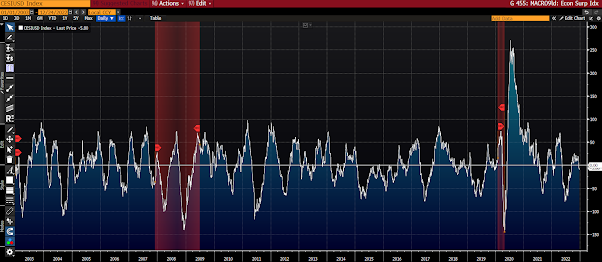

Citigroup US Economic Surprise Index:

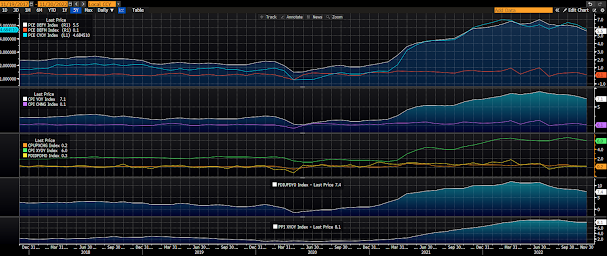

Various Inflation Metrics:

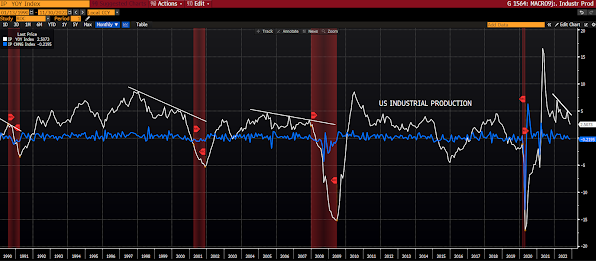

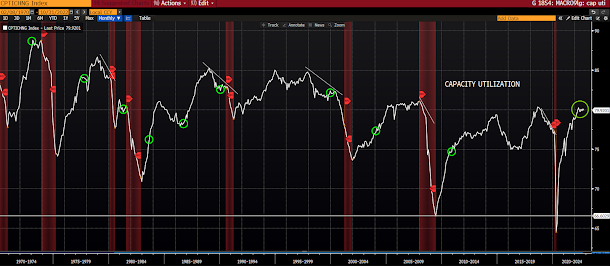

Capacity Utilization -- constructive:

Inflation Swaps:

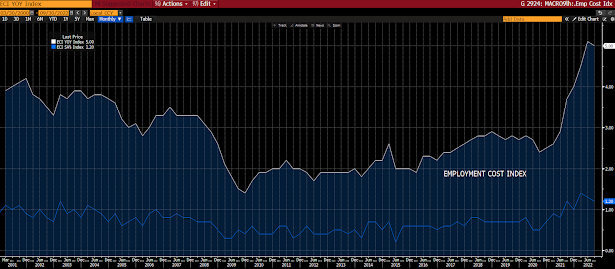

Employment Cost Index:

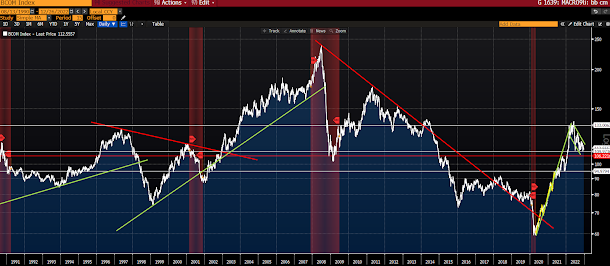

Bloomberg Commodity Index:

CRB Raw Industrials Index:

Copper Price -- constructive, of late:

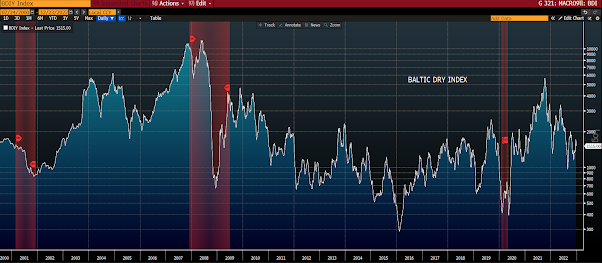

Baltic Dry Index:

1-Month Sector/SP500 Ratios.

Tech:

Financials:

Consumer Discretionary:

Materials -- constructive:

Energy -- constructive:

Industrials -- constructive:

Consumer Staples (economically-defensive sector):

Utilities (economically-defensive sector):

Healthcare (economically-defensive sector):

Consumer Staples Stocks/Consumer Discretionary Stocks

Ratio:

SP500/Long-term Treasury Bond Ratio -- trend remains constructive, although rolling over hard since 10/25:

So, definitely not all bad, and, as you can see, one could cling to, say, the employment data and predict no recession on the foreseeable horizon... When we take it all in, however, we actually see the pre-conditions for a measurable weakening of the jobs picture as we meander into 2023.

For the moment, while we indeed see recession on the horizon, we don't see anything like the 2008 experience... Our own financial stress index, for example, while elevated, does not signal the kind of systemic risk that existed back then... But we're definitely paying attention, and, like I keep saying, we remain open to all possibilities.

In part 3 we'll dig into our long-term thesis via our argument as to why the proverbial four most dangerous words in investing, "this time is different," is indeed how we see things going forward.

Thanks for all the charts Marty! S&P higher or lower will depend in my opinion on corporate earnings. Nike earning came out not too long ago and was better than expected because they deeply discounted their products in order to sell all the old inventories. On the flip side, history shows that there is always a recession following the Fed interest rate increase.

ReplyDeleteA Bloomberg's article came out two (2) days ago; the headline said "World Economy Is Headed for a Recession in 2023, Researcher Says". Two key points from the article:

1. "High interest rates take a toll as inflation remains a threat"

2. "China not forecast to pass US as largest economy until 2036"

For today's economy, it is very different from the ones before. We will see how it plays out next year (I expect more volatility).