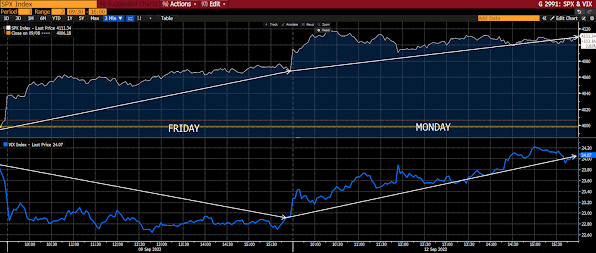

Yesterday's action was interesting from the get go... Not so much the follow-through from Friday's rally, but the fact that the VIX (tracks the implied volatility price in SP500 options) stayed notably bid start to finish.

Let's compare yesterday's action in the VIX (bottom panel, SP500 on top) to Friday's...

Honestly, I was expecting the SP500 to succumb by the end of the day, if indeed the VIX were to remain elevated throughout the session -- but that's clearly not how it played out. The bulls remained undeterred in the face of that relentless pricing up of volatility (via put buying).

Now, if yesterday's bulls indeed got it right, and the market rallies today on the August CPI number, yesterday's hedgers have essentially set the stage for the upside move to maybe catch some extra oomph, as the sellers of those puts (the dealers) will be covering their own hedges (they short the underlying to hedge their own exposure)... I.e., they'll be buying the stuff they shorted to cover their butts.

If, on the other hand, the market doesn't like what it sees, a decent enough selloff would have options dealers having to increase their hedging (their shorting), which would serve to exacerbate the downside action.

As we've been painstakingly pointing out of late, underlying positioning/hedging can have a not-small impact on a market's day to day moves, regardless of what the underlying fundamental setup might otherwise dictate.

Speaking of underlying setups, we keep stumbling across data that support our present mild-recession thesis:

"Consumer spending was robust last month, according to data from BofA. That helps back the view any potential slowdown may be mild, and the Fed has a shot at a soft landing. BofA has also concluded that August retail sales (due mid-month) were probably strong too, while vacation-goers squeezing in a Labor Day holiday probably spent on things like lodging and restaurants."

That’s in keeping with remarks from American Express CFO Jeff Campbell, who also said the US consumer still looks very strong. Commercial travel and entertainment spending ticked up. In fact, Campbell said that as of today, Sept. 12, there were no significant signs of weakness anywhere in the slice of the economy American Express covers."" --Bloomberg

Of course none of that serves the Fed's goal of curbing inflation by curbing demand... (I bolded that line for a reason!)

And, via BCA Research, evidence that supports our long-term bullish metals narrative: emphasis mine...

"Bottom Line: The IRA (Inflation Reduction Act) incentivizes investment in clean energy, pollution reduction and GHG remediation, and employment in the energy-supply market writ large. The next year likely will be taken up writing the actual regulations implementing the IRA. If it succeeds in significantly boosting renewable energy investment and EV sales, it will stoke already-tight base metals markets and drive costs higher. By incentivizing the development of carbon-capture and hydrogen technologies, it would extend the life of traditional hydrocarbon energy."

And, not to mention, our constructive long-term view on ag commodities:

"Bottom Line: A remarkable confluence of exogenous weather shocks and supply constraints in commodity markets will push food and energy prices higher, and raise inflation expectations." --BCAI.e., on a 5-year+ time horizon, I very much like our prospects. On a 5-day, 5-week or 5-month horizon, however, it's a tossup (with, we're thinking, lower lows for stocks somewhere along the way)…

Well, as I type, the market doesn't like what it saw in this morning's CPI report -- August inflation came in notably hotter than economists anticipated!

Perhaps yesterday's put buyers had it right after all...

Asian equities rallied overnight, with all but 14 of the 19 markets we track closing higher (although all of that is being taken back in the futures market this morning).

Europe's reeling (US dollar rallying) over this morning's US inflation print, with 18 of the 19 bourses we follow trading down as I type.

US stocks are feeling pain to start the session: Dow down 559 points (1.73%), SP500 down 2.09%, SP500 Equal Weight down 2.05%, Nasdaq 100 down 2.89%, Nasdaq Comp down 2.92%, Russell 2000 down 2.43%.

The VIX sits at 24.77, up 4.13%.

Oil futures are up 0.66%, gold's down 1.26%, silver's down 0.99%, copper futures are down 0.97% and the ag complex (DBA) is down 0.50%.

The 10-year treasury is down (yield up) and the dollar is up a big 0.96%.

Among our 35 core positions (excluding options hedges, cash and short-term bond ETF), only 1 -- base metals futures -- is in the green so far this morning. The losers are being led lower by AMD, uranium miners, Dutch Bros, our semiconductor ETF and communications stocks.

Have a great day!

Marty

Asian equities rallied overnight, with all but 14 of the 19 markets we track closing higher (although all of that is being taken back in the futures market this morning).

Europe's reeling (US dollar rallying) over this morning's US inflation print, with 18 of the 19 bourses we follow trading down as I type.

US stocks are feeling pain to start the session: Dow down 559 points (1.73%), SP500 down 2.09%, SP500 Equal Weight down 2.05%, Nasdaq 100 down 2.89%, Nasdaq Comp down 2.92%, Russell 2000 down 2.43%.

The VIX sits at 24.77, up 4.13%.

Oil futures are up 0.66%, gold's down 1.26%, silver's down 0.99%, copper futures are down 0.97% and the ag complex (DBA) is down 0.50%.

The 10-year treasury is down (yield up) and the dollar is up a big 0.96%.

Among our 35 core positions (excluding options hedges, cash and short-term bond ETF), only 1 -- base metals futures -- is in the green so far this morning. The losers are being led lower by AMD, uranium miners, Dutch Bros, our semiconductor ETF and communications stocks.

"Americans' chronic failure to grasp the seasonality of history explains why the consensus forecasts about the national direction usually turn out so wrong."

--Strauss, William; Howe, Neil. The Fourth Turning

Have a great day!

Marty

No comments:

Post a Comment