This morning's August jobs report came in close enough to expectations (which, btw, is consistent with our ultimately mild recession narrative) to not roil markets -- at least, given the pre-market reaction, initially. In fact, equity futures actually rallied as the details came through. My guess would be that the drop in hourly earnings, the .2% rise in the unemployment rate, and the rise in the labor force participation rate -- all being potentially disinflationary -- are the factors that have the market celebrating, at least on the announcement...

It'll be interesting to see if Fedheads don't hit the airwaves with some pushback against rising stock prices -- as they've been prone to do of late...

In a word, Oof!!

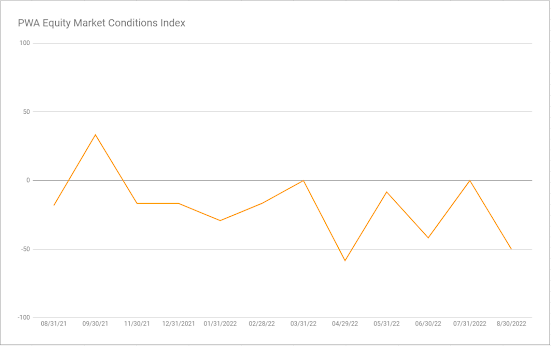

09/01//2022 PWA EQUITY MARKET CONDITIONS INDEX (EMCI): -50 (from 0 on 7/27/2022)

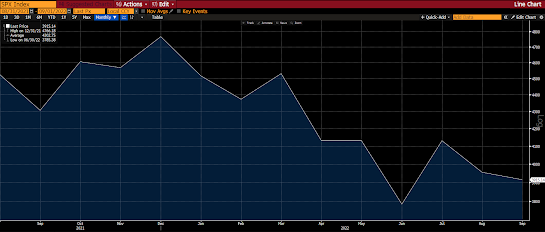

SP500 past 30 days -5.77%:

Our EMCI’s decline to -50, from 0 to end July, is substantial; reflecting notable deterioration in general equity market conditions over the past few weeks.

Inputs that showed improvement:

None

Inputs that deteriorated:

Interest Rates (from neutral to negative)

Sector Leadership (from positive to neutral)

SPX Technical Trend (from neutral to negative)

Breadth (from positive to negative)

Inputs that remained bullish:

US Dollar

Sentiment (bearish/high fear… i.e., contrarian indicator)

Inputs that remained bearish:

Fed Policy

Valuation

Economic Conditions

Geopolitics

Credit Market Conditions

Areas that remained neutral:

Fiscal Policy

EMCI since inception:

SP500 since EMCI inception:

The one input that I suspect the more tutored reader might object to (in terms of how we score it) would be the dollar. I.e., it's been an utter wrecking ball this year (rising) and, go figure, we currently score it a positive.

Here's a short and sweet snippet from our internal narrative:

Asian equities leaned red overnight, with 10 of the 16 markets we track closing lower.

Europe's in rally mode so far this morning, with all of the 19 bourses we follow trading up as I type.

US stocks are clinging to those pre-market gains to start today's cash session: Dow up 143 points (0.46%), SP500 up 0.64%, SP500 Equal Weight up 0.67%, Nasdaq 100 up 0.51%, Nasdaq Comp up 0.60%, Russell 2000 up 0.14%

The VIX sits at 24.02, down 6.03%.

Oil futures are up 2.49%, gold's up 0.67%, silver's up 0.59%, copper futures are down 0.04% and the ag complex (DBA) is up 0.57%.

The 10-year treasury is up (yield down) and the dollar is down 0.38%.

Among our 35 core positions (excluding options hedges, cash and short-term bond ETF), only 28 -- led by energy stocks, uranium miners, Sweden equities, metals miners and Eurozone equities -- are in the green so far this morning. The losers are being led lower by base metals futures, Dutch Bros, AMD, Disney and emerging market equities.

Marty

US DOLLAR: +1 (n/c)

Bearish macd/rsi divergences remain as price is presently breaking out to new highs:

I.e., our assessment for our EMCI's purposes is entirely technical... And it says the dollar's in risk of weakening right here... Which, by itself (just by itself mind you), would present a tailwind for equities... but, alas, a tailwind for inflation as well -- which would be a headwind for equities... Hence our present rock-and-a-hard-place narrative...

Asian equities leaned red overnight, with 10 of the 16 markets we track closing lower.

Europe's in rally mode so far this morning, with all of the 19 bourses we follow trading up as I type.

US stocks are clinging to those pre-market gains to start today's cash session: Dow up 143 points (0.46%), SP500 up 0.64%, SP500 Equal Weight up 0.67%, Nasdaq 100 up 0.51%, Nasdaq Comp up 0.60%, Russell 2000 up 0.14%

The VIX sits at 24.02, down 6.03%.

Oil futures are up 2.49%, gold's up 0.67%, silver's up 0.59%, copper futures are down 0.04% and the ag complex (DBA) is up 0.57%.

The 10-year treasury is up (yield down) and the dollar is down 0.38%.

Among our 35 core positions (excluding options hedges, cash and short-term bond ETF), only 28 -- led by energy stocks, uranium miners, Sweden equities, metals miners and Eurozone equities -- are in the green so far this morning. The losers are being led lower by base metals futures, Dutch Bros, AMD, Disney and emerging market equities.

Clients and regular readers know that we are uber-bullish copper (long-term) going forward. Here's one big reason why:

"The Anglo American CEO said we will need about 17 million metric tons of additional copper for the energy transition into EV and other sectors. That’s like 60 more of their new Quelleveco copper mines, “nobody has started any of those 20 year projects.”"

Marty

Thanks for the market updates. Take care. Have a good weekend! Have a happy labor day!

ReplyDeleteHey thanks Sam! Same to you and yours!

Delete