We'll begin our commentary during this holiday-shortened week with some key insights from our latest messaging:

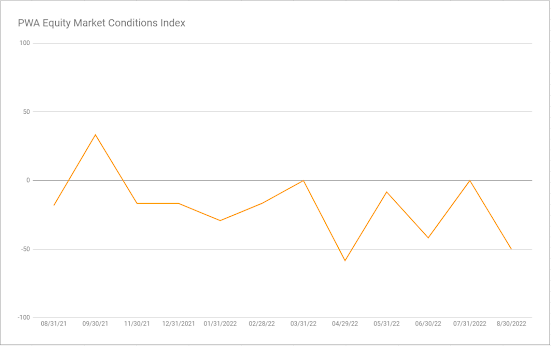

Here's the rundown of our latest monthly scoring of our PWA Equity Market Conditions Index (EMCI).

In a word, Oof!!

09/01//2022 PWA EQUITY MARKET CONDITIONS INDEX (EMCI): -50 (from 0 on 7/27/2022)

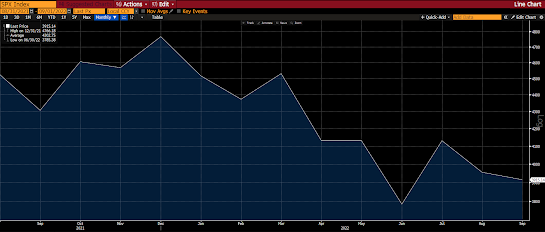

SP500 past 30 days -5.77%:

Our EMCI’s decline to -50, from 0 to end July, is substantial; reflecting notable deterioration in general equity market conditions over the past few weeks.

Inputs that showed improvement:

None

Inputs that deteriorated:

Interest Rates (from neutral to negative)

Sector Leadership (from positive to neutral)

SPX Technical Trend (from neutral to negative)

Breadth (from positive to negative)

Inputs that remained bullish:

US Dollar

Sentiment (bearish/high fear… i.e., contrarian indicator)

Inputs that remained bearish:

Fed Policy

Valuation

Economic Conditions

Geopolitics

Credit Market Conditions

Areas that remained neutral:

Fiscal Policy

EMCI since inception:

SP500 since EMCI inception:

The one input that I suspect the more tutored reader might object to (in terms of how we score it) would be the dollar. I.e., it's been an utter wrecking ball this year (rising) and, go figure, we currently score it a positive.Here's a short and sweet snippet from our internal narrative:US DOLLAR: +1 (n/c)

Bearish macd/rsi divergences remain as price is presently breaking out to new highs:I.e., our assessment for our EMCI's purposes is entirely technical... And it says the dollar's in risk of weakening right here... Which, by itself (just by itself mind you), would present a tailwind for equities... but, alas, a tailwind for inflation as well -- which would be a headwind for equities... Hence our present rock-and-a-hard-place narrative...

During our daily portfolio and macro session yesterday morning, Nick and I discussed the dynamics around the 2008 "Great Financial Crisis" and the milder early-00s (tech bubble) recession, and acknowledged the adage "generals are always fighting the last battle."

I.e., the powers-that-be are forever reacting to and regulating conditions past in their efforts to influence conditions present and future. Inevitably engendering what becomes your proverbial finger in the dike metaphor:

Yep, while there is indeed a serious structural inflation regime shift in play, make no mistake, the bailouts, the money printing, the financial repression (holding interest rates down), have been no small contributors to the inflation that has to this point overwhelmed all the Fed's fingers and toes.

Hence, on a virtually daily basis of late, we're hearing Fedhead commentary such as the following (yesterday):

"My current view is that it will be necessary to move the fed funds rate up to somewhat above 4% by early next year and hold it there."

"I do not anticipate the Fed cutting the fed funds rate next year."

"Even if the economy were to go into a recession, we have to get inflation down."

--Cleveland Fed President Loretta Mester

Sticking with our recent rock-and-a-hard-place theme, here's Bloomberg macro analyst Cameron Crise yesterday on the earnings risk stocks presently face:"...it is likely to be earnings, rather than the trajectory of interest rates, that hold the key to the next big moves in the stock market.Thus far, the deterioration in expectations has been relatively modest... but it’s nevertheless been notable relative to the trends of the last couple of years.It’s one thing to navigate a hawkish Fed when nominal earnings expectations are still rising, but quite another when your profit forecasts start to fall.Buckle up, because things could be about to get pretty spicy again."That said, and, by the way, we agree, keep in mind that we remain fairly sanguine in terms of the severity of the coming (we think) recession.

From our August 9th morning note:

"...given that present Fed policy, amid a generally weakening macro backdrop, remains in tightening mode (with QT set to double next month) — odds that the latest (short-covering and gamma-hedging) rally will fail and give way to, at a minimum, a test of the bear market lows remain elevated.

But what if we don’t actually enter recession? Won’t corporate earnings indeed hold up, supporting a new bull market trend going forward?

Well, yes, in terms of earnings. However, a no-recession scenario, with its attendant animal spirits, will likely keep inflation elevated to the point that has the Fed maintaining its tighter stance far longer than markets are presently discounting. Which would provide a potentially serious headwind for equity multiples going forward.

In fact, equities don’t look to me like they’re remotely discounting the inevitable earnings decline that would occur should we enter recession…"

"...any evidence that inflation is seriously coming off the boil will surely inspire rallies in global equities. But, again, rallies in equities are essentially a loosening of financial conditions. I.e., such rallies will likely turn out to be the short-lived victims of fed quashings."

We've spent a lot of time herein over recent weeks on positioning dynamics under the market's surface that help explain how a rally in stocks can gain some serious steam directly in the face of some serious fundamental headwinds.

In particular, we talked about options dealers’ positioning as well as what has been a high degree of short interest in S&P 500 futures contracts (bets that the market's going to fall).

Yesterday's Wall Street Journal featured an article touching on the latter.

Snippets: emphasis mine...

"Net short positions against S&P 500 futures have grown in the past couple months, reaching levels not seen in two years. That means traders are increasing their bets that the index will fall, or at least hedging against that risk."

"Short positioning in the market can help participants gauge sentiment and can influence the magnitude of stock moves, investors and strategists say. If stocks rally, short sellers may be squeezed to cover positions, which could accelerate the market’s upward move."That last sentence is what we've been talking about.

However, like I said in a last Friday video, the shorts could indeed ultimately have it right, and, thus, get handsomely rewarded for their bearish bets. Like last Friday! As opposed to forever having to cover in a rising market...

Asian equities leaned green overnight, with 9 of the 16 markets we track closing higher.

Europe's mostly green so far this morning as well, with 14 of the 19 bourses we follow trading up as I type.

US stocks are tilting to the positive to start the session: Dow up 129 points (0.41%), SP500 up 0.28%, SP500 Equal Weight up 0.29%, Nasdaq 100 up 0.20%, Nasdaq Comp up 0.16%, Russell 2000 up 0.04%

The VIX sits at 25.91 up 1.88%.

Oil futures are up 0.66%, gold's down 0.09%, silver's up 0.60%, copper futures are up 0.17% and the ag complex (DBA) is up 0.02%.

The 10-year treasury is down (yield up) and the dollar is down 0.10%.

Among our 35 core positions (excluding options hedges, cash and short-term bond ETF), 22 -- led by uranium miners, Albemarle, base metals miners, silver and oil services stocks -- are in the green so far this morning. The losers are being led lower by Dutch Bros, Brazil equities, treasury bonds, Asia-Pac equities and AMD.

"...while madness is rare in individuals, the philosopher Nietzsche, among others, taught us that it becomes the norm in groups. People go mad in crowds and crowds form because uncertainty, or unquantifiable risk, being the dominant feature of financial markets, forces us to fall back on rules of thumb and consensual thinking.Crowds with money are particularly unstable and they go a long way to explain the roller-coaster swings of financial markets between the extremes of greed and fear. Therefore, we argue that, contrary to the textbooks, investment is fundamentally about risk, return and liquidity."

--Howell, Michael J.. Capital Wars

Have a great day!

Marty

Thanks Marty!

ReplyDeleteYou be Sam!

Delete