This is the finale to our 2024 year-end message. Please definitely take this one in. Feel free to skip to the summary video at the end. Thanks so much!!

Before we get to the dollar, I'd like to touch on what I'll call the "December Mess" of a market for stocks by quoting derivatives market specialist, and co-host of the uber-popular Market Huddle Podcast, Patrick Ceresna, as he charted the US equity market sector-by-sector during last week's episode:

In this year's year-end message Part 1 we touched on three investing rules to live by.

Essentially:

1. Control risk

2. Buy value

3. Be patient

So, while controlling risk may be accomplished in a number of ways, it's generally-speaking pretty easy, but it ain't free.

If we're talking diversification, cost comes by way of missing out on concentrated returns when a particular asset class, or, say, a small group of stocks realize outsized upside relative to the rest (à la recently, in record fashion!)... If we're talking insuring against massive declines in a given asset class, security or group of securities, there's the options premium we pay.

As for #2, buying value is easy enough, when you can find it, andof course you have to know how to measure it.

#3, patience, depending on who you are, can far and away be the most difficult rule to follow! Particularly when you see a given tech stock or, say, crypto currency, rocketing -- without you -- to the proverbial moon... Or, on the other hand, when it feels like the world is melting down all around you, and panic begins to grip your decision making process.

Ideally, if we satisfy #1 well enough, we can keep panic-driven reactions at bay... As they, along with greed-driven decisions, are inevitably the worst decisions investors make!

Here, in Part 3, we're going to focus primarily on rule # 2, buying value.

Just FYI for you daily stock market-watchers... As I keep preaching, breadth (massive divergence[s]) in December doesn't paint the rosiest of pictures.

In the chart below:

SP500 white (largest market caps have the most influence): -1.38% SP500 equal weight green (all the same stocks with equal representation): -6.02%

Dear clients, just FYI, for those of you who watch your accounts on a daily basis, today is a day when a large number of your ETF positions trade without their December dividend payout. Therefore, the price trades without the amount of the dividend per share. Artificially lessening the upside move or exacerbating the downside move, whichever occurs today.

In a few days (the pay date) the dividend will be paid to your account, causing the opposite -- exacerbating an upside day, or limiting the move on a downside day.

On another note, all of us here at PWA wish you and yours a very Merry Christmas and the Happiest of New Years!

Dear Clients, this morning's commentary is VERY important to take in... start to finish... Thanks!

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Dear Clients, please take a few minutes and take in today's brief video commentary.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Staying with the topic of US stocks for the moment: We can assume, with confidence, that the durability of the current bull market is largely due to the overwhelming consensus among investors that an economic "soft landing," and, with it, ever-rising corporate profits is essentially at hand.

A soft landing for stocks would presumably mean continued higher prices amid declining bond yields -- the proverbial best of both worlds, or, let's say, the ideal Goldilocks scenario.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Inflation I suppose is a different thing to different people...

At the end of the day, or, let’s say, in reality, while politicians, and financial markets, may celebrate a calming of inflation’s go-forward rate-of-change (purple line), consumers – particularly those in the lower 40% of income earners – continue to suffer (some, devastatingly) from inflation’s 4-year cumulative effect (blue line).

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Attention Clients, this is an important post to take in... Thanks for reading!

The following are excerpts from the latest entries to our internal market log.

In summary.

1. Since the election:

6 of the US major equity sectors are up, 5 are down.

The US is the only major regional equity market in the green... The others featured are notably in the red.

Among the major industrial commodities we track, all have sold off significantly, save for natural gas.

Among the ag commodities we track, 8 are up, 6 are down.

US Treasuries have taken quite the hit (as interest rates popped higher), Investment grade corporate bonds are flat, junk bonds are up slightly.

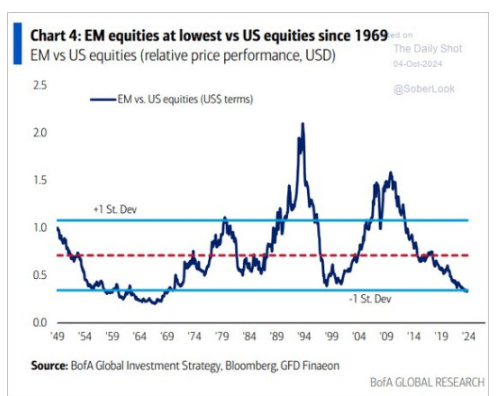

2. Foreign equities are all-time cheap relative to the US.

3. US equities are, by themselves, at (or near) all-time expensive valuations.

3. Zip Recruiter warns about the state of the labor market and, therefore, the economy.

4. Me (via an email with a friend) on the prospects for commodities going forward, the nat'l debt, and the history of the early stages of world-changing technologies.

Bottom line, the rip-roaring rally of the past week has been the definition of concentrated. I.e., not so great for balanced portfolios that diversify across asset classes, sectors and regions... But, make no mistake, the setup, as we ultimately move into the next cycle, offers many historically-attractive opportunities for macro-centric portfolios.

Dear Clients, please be sure and give this one a watch/listen when you have a few minutes.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Of course this should go without saying, but given the season I'm compelled to remind clients that politics have unequivocally zero influence on our asset allocation decisions (and I'm certain you'd have it no other way)... Policy, on the other hand, is indeed something we need be cognizant of with regard to its longer-term economic and market (global as well as domestic) ramifications.

Clients, be sure and take a few minutes when you can and take this one in.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

As I've been pointing out in nearly every video commentary of late, the data, on balance, have indeed improved; lessening the risk of imminent recession... I've also pointed out (charted for viewers), however, the counterintuitive fact that much of the data we measure have historically-tended to see a last-gasp ramp just before the onset of recession... Hmm...

So, while, indeed, such macro improvement has us considering where to adjust allocations to take full advantage of a potentially-improving setup, history says we nevertheless need to -- at the same time -- remain on our toes, at least for the time being.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Suffice to say that gold resting at all time highs amid rising long-term treasury yields, and, not to mention, a strengthening dollar isn’t what you’d call intuitive.

Currently testing some new video software, and don't quite have it where we want it just yet... I expect next week we'll be back at it with your end-of-week message delivered via video.

In the meantime, the following consists of a few highlights from our latest internal notes along with commentary I'll add for clarity and context... I'll close with some compelling (BCA) arguments against the growing notion that we're out of the woods just yet:

10/12/2024

The technical setup for the dollar (bullish) that we flagged a couple weeks ago has played out to a T:

The reopening of Chinese markets, after “Golden Week”, was met with some serious profit taking. Headlines suggest that it's due to a press conference held by the National Development and Reform Commission (NDRC) that did not unveil any details around the fiscal stimulus measures that the market got so euphoric over the past couple of weeks... Thing is, the NDRC would not have offered up such detail, as that’s not necessarily (particularly from an immediate-term perspective) within the purview of that particular entity.

Delivering this week’s update to you in written form.

The following is the long and the short of the latest on the economy, and on financial markets.

Our PWA Index (measures overall general conditions) rose markedly for a third straight week -- moving closer to the neutral line -- denoting improved conditions (i.e., recession risk remains elevated, but notably less-so of late):

Despite the notable improvement in our own macro index, the global liquidity setup (see below), etc. (i.e., recession risk has indeed abated abit of late), we need to be very cognizant – as I’ve illustrated in recent video commentaries – of the fact that it is the norm to get a positive spike in the data just before recession ensues.

Totem Macro’s Whitney Baker (she’s an exceptional analyst, btw) pointed that out last week, along with the factors that she sees pointing to recession.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Yesterday’s move in our core allocation may turn out to have been more (near-term) timely (i.e., lucky) than we anticipated.

From our internal supporting narrative:

“Reducing our exposure to US staples and healthcare reflects marginally better odds of a soft-landing based on the Fed’s aggressive start to the easing cycle, and recent improvement in the PWA Index… However, our base case remains that recession odds are better than 50/50 on a 6-12 month horizon… Therefore, despite the cuts, staples and healthcare remain top weightings, as do cash (t-bills) and gold.

Increasing our emerging mkt equity exposure reflects the improved prospects for a near-term weaker-trending dollar, as well as China’s historically-weak valuations and the likelihood of Chinese policymakers to be forced to step up the stimulus over the next 12 months.”

Well, I guess I should've said next 12 hours... They stepped up last night… Here are the details (HT P. Boockvar):

While, based on the headline data of late, one might indeed criticize the Fed over its 50 bp cut, particularly considering how Powell cheer-leaded the “strong” economy (i.e., then why the double-cut??), our view (despite the recent less-bad reading from our own index) remains that the under-the-surface indicators point to not-small odds of recession in the not-too-distant future. So, frankly, I have no problem with the double-cut.

Noting that higher-income/asset-holding folks have been doing virtually all of the heavy-lifting for months, here’s yet another sign that we may be onto something:

Attention Clients, please consider this one a must-watch video...

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

A little bonus content that I felt compelled to share this morning.

From our internal log:

9/17/2024

While the bulls will cite what retail sales say about the strength of the consumer, when you look at them in real (inflation-adjusted) terms…. well:

“While Retail Sales are up 2.1% y/y, it still isn’t enough to keep up with the impact of inflation. Once you take that into account, Retail Sales have been negative on a y/y basis for seven of the last eight months and 17 of the last 22 months.” –Bespoke

---------------

The following got me thinking about just how unusual and unintuitive the current investment setup is.

Since this week will be mostly about the Fed, I can keep the written post very brief and to the point.

Here's from our internal Monday morning note:

9/16/2024

Nick T’s WSJ article effectively moved the needle to a 50 bps cut on Wednesday… Since the article, odds have spiked to 64% (in fed funds futures)... If that’s the case, the US central bank is clearly the most dovish among the majors, per the below:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Attention clients, this one's important to take in when you have a few minutes.

While I concede that Wall Street’s soft landing narrative – while, in my humble opinion, relying entirely on the Fed – has merit, there’s simply far too much uncertainty yet emerging from the data (not to mention where we are in the cycle, equity market valuations [very high), yada yada] to have us adding risk to client portfolios right here.

While our work sees a global macro setup fraught with risk-asset risk, today I want to consider what I see as some key points in the present bullish narrative; the narrative that says this is, in fact, an ideal moment to be adding to risk assets (read stocks).

Dear Clients, this week's video commentary is an important one to take in when you have a few minutes... 😎

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

“The only way to make money in the markets is to be patient, disciplined and informed. You have to have the confidence to make decisions based on sound analysis and rational thought.” --David Shaw

8/27/2024

While I believe we're less-sanguine on the economy right here than is Bob Elliott, I find his analysis to be spot on... I.e., the conditions priced into US equities are virtually untenable in the foreseeable future.

US stocks don't have an earnings problem, they have an expectations problem. With expectations of 3% real gdp in 2H24, earnings growth to reach 16% y/y by end of '25, and an AI boom ahead driving 21x multiples, such lofty expectations are a setup for disappointment.

In this week's written post, I said the following with regard to professional traders:

"...despite the present ever-rising risk, today’s trader believes that, in pure self-interest/preservation, they must continue to rock to the infamous 2007 tune played by ex-Citi CEO Chuck Prince:

“... as long as the music’s playing you gotta get up and dance.”"

So, I'm sitting here this morning listening to the latest Market Huddle podcast, and I hear this week's guest, Louis-Vincent Gave, say the following:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

The latest action in equities has me thinking a lot about how to properly characterize the aggregate personality of the market at this moment.

I’m thinking about the institutional trader, the hedge fund manager, yada yada, and how they live and die by their running P&L… Those who are experienced, thoughtful and objective know that we are late-cycle, that valuations are extended, and that a potentially consequential repricing of stocks is likely in the not-too-distant offing… Nevertheless, we’re not there yet, the dips continue to get bought, and – as evidenced by the Bank of Japan’s jawboning reaction to recent hemorrhaging, and likely by this week’s Fed Jackson Hole meeting – the powers that wield policy have little stomach for downward volatility.

Well, once again, we're having technical difficulties with our video software... Apparently our new "updated" version didn't correct the issue after all... We'll get with the vendor and be ready to go next week.

In the meantime, here are the visuals I had loaded up for this week, with some commentary:

Housing data say we’re not out of the woods, despite Wall Street's insistence.

Yesterday’s homebuilder sentiment reading (at 39 [under 50 = contraction]) was, let's say, not optimistic!

As I type, stocks are rallying nicely in response to a cooler than expected Producer Price Index… The S&P, at 5398, is about to test what I, in last weekend’s video, suggested was a pretty compelling area of potential resistance (5,400)… Wednesday’s CPI print, followed by Thursday’s retail sales number will of course be key determinants as to whether stocks fold at that key technical level, or whether they blow right through it and try to recapture the S&P’s all-important 50-day moving average (currently 5450), and, not to mention, a few other technical barriers between here and the recent high.

Now, beyond all this short-term, largely technical, stuff, we have to focus on what, at this stage of the cycle – and at these equity market valuations – is the ultimate question:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Dear Clients, the following, from our internal log, is important stuff!

But first, a quote:

“Acting in excessive reliance on the fact that something ‘should happen’ can kill you when it doesn’t. That’s why I always remind people about the 6-foot-tall man who drowned crossing the stream that was 5 feet deep on average. You have to be able to get through the low points. And the success of your investment actions shouldn’t depend on normal outcomes prevailing; instead, you must allow for outliers.” —Howard Marks

Just a few thoughts on the latest action in equity markets.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

While those who don’t see recession looming (looking out 6-12 months) will cite the fact that the upper half of income earners are still spending quite healthily, and that their spending represents the lion’s share of US consumption, we should nevertheless take the latest credit data seriously.

I.e., while the below may indeed reflect the pain among those not in the upper 50% of income earners, it nevertheless speaks to the evolving state of the economy, and, in our view, should be viewed as a serious warning sign:

Well, alas, technical difficulties did not allow me to post this week's video commentary, so I'll just give you the highlights.

But first, a quote:

“Whoever wishes to foresee the future must consult the past.”

Niccolò Machiavell

Starting with the technicals, here's the 1-year daily chart for the S&P 500... Like I said last week, we'll see some nice rallies off of technical support.

Update: The following content was posted yesterday for today's distribution... In the meantime, here's an entry to our internal log this morning:

Google (Alphabet) stock is getting slammed this morning on earnings comments that very much jibe with our concerns over the AI hype… They implied that patience will be needed when it comes to justifying the massive spending they and others are devoting to AI.

Like I said yesterday:

“With regard to AI, so far it’s all about companies competing to see who can spend the most on it, while seeing virtually zero offsetting profitability gains yet emerging… They’ll likely come, but there’s little evidence that said profitability will emerge to offset the bottom line hits – which tend to roil perfectly-priced markets – that’ll show up amid the heavy AI spenders in coming quarterly earnings reports.”

Context

I can't emphasize enough how all the hoopla over all-time highs in US stocks needs some serious context.

Essentially, the extent to which a mere handful of stocks have done all the lifting is historic (and, by the way, historically-unhealthy).

Here's from the 2021 peak, nearly 3 years ago... Note that while the S&P 500 and Nasdaq 100 cap-weighted indices (white and purple) have done okay since then (well, actually, since last December), the same stocks equal-weighted have produced just barely positive results for the S&P (green) and slightly negative results for the Nasdaq (yellow):

Adjust those for inflation and of course it's much worse.

Now, could, as some expect, the many ultimately catch up to the few, and thus extend the cap-weighted indices up trend far into the future?

Absolutely!

Should we, in the present late-cycle setup, bet the farm on it?

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

The action over the past week in the equity market has been extraordinary… Well, okay, I’ll just say it’s been unusual (at least seemingly, until you scroll further), to put it mildly.

It certainly bolsters the bull’s narrative that this historically-bifurcated market (the 10 biggest SP500 stocks doing ~80% of the year-to-date heavy lifting, the remainder utterly languishing) will be remedied via the rest of the market playing catch up.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Dear Clients, here's another very important update on overall conditions to take in when you have a few minutes!

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Among the many things that have that tech bubble smell, the present valuation gap between US equities and the rest of the world is like nothing we've seen since then.

US (SP500) price to sales ratio in white, Developed Foreign Markets orange, Emerging Markets blue... Red arrow at the tech bubble peak:

And here's the actual performance for each from the tech bubble peak to the real estate bubble peak (US stocks returned essentially zero during that period):

Dear clients, here's a quick & easy one, but a very important one, to take in -- start to finish.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Dear clients, here are another set of comments we'd like all of you to take in, start to finish.

The following are key highlights from our latest internal log entries (with our latest [important] video commentary at the bottom):

After whatever correction the next few days or weeks delivers (if any), I expect the data to weaken as we move further into Q3, with stocks possibly rallying on the prospects for a September Fed rate cut...

However, by the time we hit Q4 and/or Q1+ next year, the reality of recession likely sinks in, and -- while anything's possible -- we likely get our last leg down... I like that we're hedged to year-end.

Of course seasonality has to be mentioned, as a Q3 rally would be bucking the long-term worse-quarter-of-the-year trend.

Hussman sees potential for classic bubble-bursting bear market results:

I mentioned in our last video commentary the degree to which John Hussman sees stocks declining (to reach reasonable value) from present levels… While, as I explain in the video, that, in terms of magnitude, is not our base case, per the below it’s a view that demands our respect, and our attention.

And, perhaps a touch contrary to my own short-term view mentioned above, he thinks we may have already seen, or are very close to seeing, the cycle peak in stock prices.

Dear ALL Clients, this is for sure the one to watch, start to finish! Thanks so much for obliging, Marty 😎

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Dear Clients, despite the Nasdaq sitting at, and the S&P 500 near, all time highs, this week's highlights from our internal log will not inspire confidence in the go-forward setup for stocks... Which, by the way, in no way means that the next bear market is imminent... It simply means that the risk is historically high right here, and that liquidity, diversification, and, in our view, hedging here and there with options is these days more than warranted.

In our candid view, prudent long-term investing is all about knowing when, and when not, to add risk... Suffice to say that today's overall setup is not the sort that you find at the early stages of a sustainable equity bull market... One could argue quite the opposite, in fact.

Note, in this week’s video I mentioned gold’s Friday decline and suggested that it was likely a reaction to the May employment report… And while the notable selloff in treasuries perhaps lends credence to that view, I had missed the fact that China’s central bank announced last night that it did not add gold to its reserves in May… Not doubt that was a not-small contributor to Friday’s action.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Dear Clients, there'll be no written post next week, as I'll be on my annual Montana excursion, which once again has me offering up the link to an old blogpost that I believe has our all time highest hit rate.

Ironically, it has nothing to do with markets, so only take it in if you're in the mood for something touchy-feely.

Here's the link to the 2020 version (disregard the days off mentioned, this time it's Tuesday - Saturday):

Now before we get to the highlights I wanted to share what I believe may ultimately turn out to be a timely quote.

At the end of Larry Montgomery's latest book, How to Listen When Markets Speak, he offered up the following message, which to a not-small degree concurs with our longer-term go-forward view:

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Here are some selected highlights of key global economic and market data, signals, trends, etc., from our internal log over the past few days.

Be sure and read start to finish, as we cover lots of important ground over the course of a week.

Clients, if you'd like more color on any of the below, or anything else that went on in global markets/economics this past week (even if it's not featured below, there's a good chance I commented on it internally), please feel free to reach out. Last Friday 5/24/24:

Per some of our recent tactical adjustments, we’re anticipating a decoupling among global economies… Europe, in spots, for example, had been in recession while the US continued to chug right along… Recent data suggest that Europe has bottomed, while we believe the US – despite yesterday’s positive PMIs – is in the process of peaking, if it hasn’t already peaked.

So, question being, can the rest of the world (we’ve seen some stabilization in China, for example, as well) sustain a new growth cycle, if/when the US slows markedly?

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Here are some selected highlights of key global economic and market data, signals, trends, etc., from our internal log over the past few days.

Be sure and read start to finish, as we cover lots of important ground over the course of a week.

Clients, if you'd like more color on any of the below, or anything else that went on in global markets/economics this past week (even if it's not featured below, there's a good chance I commented on it internally), please feel free to reach out.

Last Wednesday 5/15

CPI came in a bit softer than expected, core pretty much in line… Markets, bonds in particular, are, as expected (on soft data), rallying on the news…

Weaker than expected retail sales for April didn’t hurt markets either – as weak news is good news presently (all eyes on the Fed); which, alas, tends to be the making of greater market pain if indeed weak news ultimately becomes recession news.

A September rate cut is now priced into fed funds futures, if data continue to weaken that’ll get moved up in a hurry; right now there’s a 30% chance of a cut in July.

Europe, whose equities we’ve been adding to lately, has a June rate cut presently priced in.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Here are some selected highlights of key global economic and market data, signals, trends, etc., from our internal log over the past few days.

Clients, if you'd like more color on any of the below, or anything else that went on in global markets/economics this past week (even if it's not featured below, there's a good chance I commented on it internally), please feel free to reach out.

Last Wednesday 5/8

BCA’s US Equity Strategy Team’s remarkably accurate model is the most bearish it’s been since I’ve been following it… Chief strategist Peter Berezin, however, sees potential near-term upside should data begin to weaken soon, as the market will likely rally on the notion that the Fed will, thus, become measurably accommodative... Which is my current base case as well.

Last Wednesday 5/8

Despite it being down slightly since we put on our small starter position, I’m liking the longer-term setup for the yen right here.

My view from the get-go is far more basic than the rantings of those who see a currency crisis in the making… I.e., it’s simply a matter of macro cycle timing and interest rate differentials.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Here are some selected highlights of key global economic and market data, signals, trends, etc., from our internal log over the past few days.

Clients, if you'd like more color on any of the below, or anything else that went on in global markets/economics this past week (even if it's not featured below, there's a good chance I commented on it internally), please feel free to reach out.

Last Thursday 5/2 Generally speaking, it’s pretty clear that the market (equity mkt in particular) is pricing in a soft landing and strong go-forward corporate earnings growth.

Given that there are sufficient leading indicators to cause concern, the soft landing thesis continues to stand on shaky ground, which of course conflicts with that forward earnings bullishness.

Ironically, while my stated concern ultimately leads to consequently-lower equity prices, along the way to a harder-than-priced-in-landing, a notable rally in equities (classic “blowoff top” perhaps) is very much on the cards – as the economy/inflation cools.

Bottom line, the likely equity market transition for the no-soft-landing scenario sees stocks flat to down as long as inflation remains elevated… Then stocks rally as the economy and, thus, inflation cools… Then stocks finally rollover when recession becomes reality… Then a fundamentally-sound buying opportunity presents itself.

Clients, please be sure and take this one in when you have a few minutes.

Have a nice weekend!

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Here are some selected highlights of key global economic and market data, signals, trends, etc., from our internal log this past week.

Believe it or not, in a feeble attempt at brevity, I cut a ton out... So, clients, if you'd like more color on any of the below, or anything else that went on in global markets/economics this past week (even if it's not featured below, there's a good chance I commented on it internally), please feel free to reach out.

Well, I'm already breaking my own new rule, by publishing two blog posts on the same day... Can't resist it this morning... I.e., I don't want this one to get lost in the shuffle of next week's summary.

This morning's log entry:

4/27/2024

This from Grant Williams' podcast guest is, in essence, what I’ve been describing during client review meetings of late…

I.e., In terms of what he says about how policy will be implemented going forward, I couldn’t agree more!

I somehow failed to mention the market implications of next week's treasury quarterly refunding announcement... Before you click the play button, here’s from our internal notes:

4/23/2024

Next week’s QRA (the treasury’s quarterly refunding announcement) is likely to be big for markets.

If Yellen wants to concentrate go-forward issuance on the short end of the curve, that’s easy for the market to absorb and bullish for equities.

If, on the other hand, she signals that issuance will concentrate on the long-end (far more difficult for the market to absorb (i.e., yields higher), that’s bearish.

With regard to the TGA (treasury general account), if she sets a high target (i.e., much bond issuance proceeds get stuck in the TGA, as opposed to being spent in the economy), that’s bearish.

If she sets a relatively low target (i.e., more juice going into the economy), that’s bullish.

Her track record thus far – not to mention, incentives – leans heavily toward t-bill concentration and a lowish TGA target (i.e., she definitely wants to keep financial markets buoyant going forward)... Problem being, that would be economically-stimulative, which might problematically offset what would otherwise be hugely bullish (operative word their being “might”) for equities... I.e., a resilient economy means sticky inflation, and sticky inflation means no aggressive rate cutting over the next few months, which could be a real downer for equities going forward.

Nevertheless, if we're talking relatively light issuance (less than last quarter) focused on the short-end of the curve, and, again, a lowish TGA target, stocks are likely to, at least initially, rally on the news.

Once playing, click the icon in the lower right corner for full screen. Focus should occur after a few seconds; if not, click the wheel to the left of the YouTube icon to adjust:

Attention Non-Client subscribers: Nothing in this video should be construed as investment advice. The examples expressed relate to portfolio management we perform on behalf of our clients, and, again, under no circumstances are they to be considered recommendations to the viewer.

Here are the latest highlights of key global economic and market signals, trends, etc., from our internal log... Be sure and peruse all the way to the end, as we highlight a broad range of topics.

4/19/2024

Equity futures, bonds, currencies, commodities all reacted aggressively to the initial news of Israel’s attack on a military base in Iran… As the dust settled it became clear that the attack was limited in scope – i.e., tit for tat – and, therefore, for the moment, not a market event… As I type, 7:04am, the S&P is flat, the Nasdaq’s off 56 bps, yields are down a bit, gold’s up 25 bps, the dollar’s down 21 bps and oil’s flat.

4/19/2024

The latest Fed Beige Book release (a view from each of the 12 districts) points to an economy that continues to expand, albeit at a snail's pace at this point, and a consumer who is, on balance, becoming more cautious on spending… Inflation signals are mixed, but, on balance, somewhat problematic for businesses as their pricing power now seems to be fleeting.